Friday, November 9, 2018

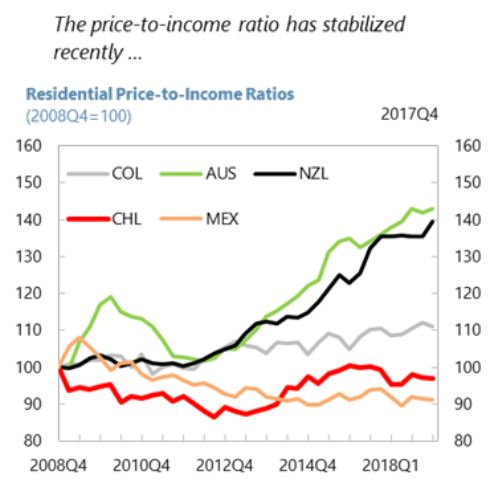

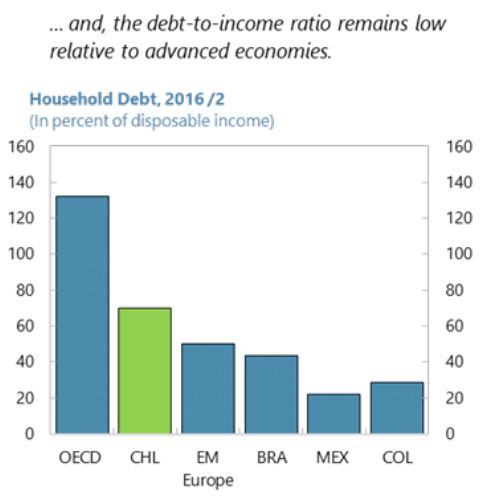

Chile: Housing Market Developments

Posted by at 4:20 PM

Labels: Global Housing Watch

Housing View – November 9, 2018

On cross-country:

- 2018 Housing Finance in Africa Yearbook – Centre for Affordable Housing Finance in Africa

- Pockets of risk in European Housing Markets: then and now – Central Bank of Ireland

- UN Special Rapporteur Leilani Farha on homelessness, human rights and why the lack of adequate housing is on the rise – Al Jazeera

- ULI/ PwC’s Emerging Trends in Real Estate Europe 2019 – Urban Land Institute

On the US:

- Birth Rates and Home Values: A Closer Look – Zillow

- Affordability, Disruption & Rising Interest Rates Lead Top Ten Issues Facing Real Estate – National Association of Realtors

- US Housing: As good as it gets? – ING

- When Millennials Battle Boomers Over Housing – Citylab

- Ballots for Buildings: Voters Weigh Affordable Housing Measures – The Pew Charitable Trusts

- Are median incomes actually stagnating? How we calculate housing costs affects the answer – Urban Institute

- Amazon’s real estate team did its homework – Brookings

- How Minimum Zoning Mandates Can Improve Housing Markets and Expand Opportunity – The Aspen Institute

- Resilience and housing markets: Who is it really for? – Land Use Policy

On other countries:

- [Australia] Australia’s Property Slump Casts Doubt on Household Spending – Bloomberg

- [Australia] Significant drop in auction rates set alarm bells ringing for major Australian housing markets – Global Property Guide

- [Canada] Vancouver’s complicated relationship with Chinese money – CBC

- [China] Three New Signs China’s Housing Market Slowdown Is Taking Hold – Bloomberg

- [Denmark] Party is over for apartment owners – but the Danish housing market is picking up – Danske Bank

- [Hungary] Measuring Heterogeneity of House Price Developments in Hungary, 1990–2016 – Central Bank of Hungary

Photo by Aliis Sinisalu

On cross-country:

- 2018 Housing Finance in Africa Yearbook – Centre for Affordable Housing Finance in Africa

- Pockets of risk in European Housing Markets: then and now – Central Bank of Ireland

- UN Special Rapporteur Leilani Farha on homelessness, human rights and why the lack of adequate housing is on the rise – Al Jazeera

- ULI/ PwC’s Emerging Trends in Real Estate Europe 2019 – Urban Land Institute

On the US:

- Birth Rates and Home Values: A Closer Look – Zillow

- Affordability,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, November 8, 2018

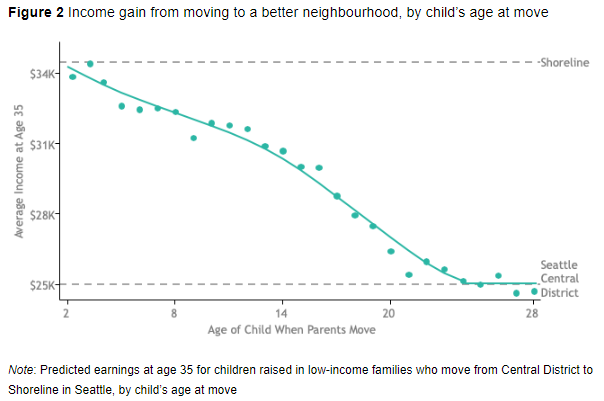

The Opportunity Atlas: Mapping the childhood roots of social mobility

From a new VOX post:

“Economic mobility varies dramatically across the US. This column introduces a new interactive mapping tool that traces the roots of outcomes such as poverty and incarceration back to the neighbourhoods in which children grew up. Among the insights the data reveal are that children who grow up a few miles apart in families with comparable incomes have very different life outcomes, and that moving in early childhood to a neighbourhood with better outcomes can increase a child’s income by several thousands of dollars later in life.”

“Children who move to high-upward-mobility neighbourhoods earlier in their childhood earn more as adults, as illustrated in Figure 2. This chart shows the average income (at age 35) of children raised in low- income families who move from the Central District of Seattle, a low-upward mobility area, to Shoreline, a high upward-mobility area that is ten miles north. Children who make this move at birth earn $9,000 more per year than those who move in their 20s.”

From a new VOX post:

“Economic mobility varies dramatically across the US. This column introduces a new interactive mapping tool that traces the roots of outcomes such as poverty and incarceration back to the neighbourhoods in which children grew up. Among the insights the data reveal are that children who grow up a few miles apart in families with comparable incomes have very different life outcomes, and that moving in early childhood to a neighbourhood with better outcomes can increase a child’s income by several thousands of dollars later in life.”

Posted by at 3:01 PM

Labels: Inclusive Growth

Monday, November 5, 2018

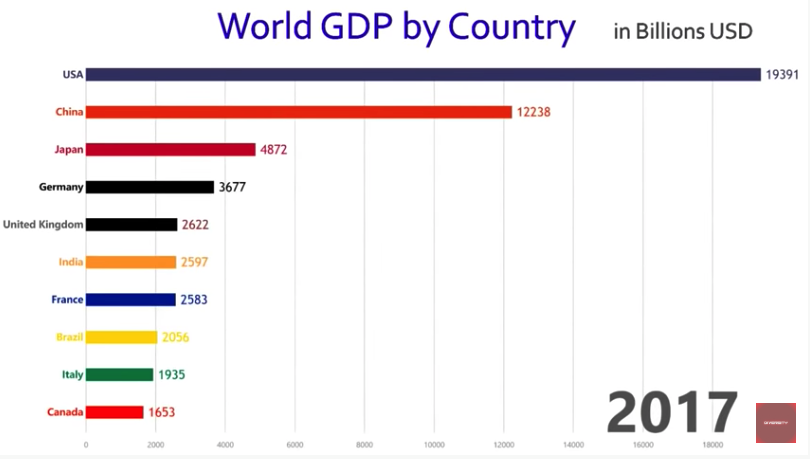

Dynamic chart: World’s ten largest economies, 1961 to 2017

From a new AEI post:

“Watch the top ten largest economies in the world based on GDP, year-by-year from 1961 to 2017. A few interesting observations:

1. The global slowdown in the early 1980s.

2. China’s ranking in the world’s ten largest economies has sure bounced around a lot. It was the world’s fifth largest economy in 1962 and remained in the top ten economies until it dropped out in 1978 and 1979, before returning in 1980, dropping out again for a few years and returning to the top ten in 1982. In 1987, China fell out for a year, came back in 1988, dropped out again in 1989 before returning to the top ten for good in 1992. By 2000, China rose to the No. 6 position by passing Italy, then to No. 5 in 2005 when it surpassed France, to No. 4 in 2006 when it surpassed the UK, No. 3 in 2007 surpassing Germany, and finally rising to No. 2 in 2010 by surpassing Japan.

3. As of 2017, the US economy at $19.4 trillion was 58.4% larger than China’s GDP of $12.2 trillion.”

Watch the dynamic chart here.

From a new AEI post:

“Watch the top ten largest economies in the world based on GDP, year-by-year from 1961 to 2017. A few interesting observations:

1. The global slowdown in the early 1980s.

2. China’s ranking in the world’s ten largest economies has sure bounced around a lot. It was the world’s fifth largest economy in 1962 and remained in the top ten economies until it dropped out in 1978 and 1979,

Posted by at 9:42 PM

Labels: Macro Demystified

Balancing Financial Stability and Housing Affordability: The Case of Canada

From the IMF’s latest report on Canada:

“Housing market imbalances are a key source of systemic risk and can adversely affect housing affordability. This paper utilizes a stylized model of the Canadian economy that includes policymakers with differing objectives—macroeconomic stability, financial stability, and housing affordability. Not surprisingly, when faced with multiple objectives, deploying more policy instruments can lead to better outcomes. The results show that macroprudential policy can be more effective than policies based on adjusting propertytransfer taxes because property-tax policy entails excessive volatility in tax rates. They also show that if property-transfer taxes are used as a policy instrument, taxes targeted at a broader-set of homebuyers can be more effective than measures targeted at a smaller subset of homebuyers, such as nonresident homebuyers.”

From the IMF’s latest report on Canada:

“Housing market imbalances are a key source of systemic risk and can adversely affect housing affordability. This paper utilizes a stylized model of the Canadian economy that includes policymakers with differing objectives—macroeconomic stability, financial stability, and housing affordability. Not surprisingly, when faced with multiple objectives, deploying more policy instruments can lead to better outcomes. The results show that macroprudential policy can be more effective than policies based on adjusting propertytransfer taxes because property-tax policy entails excessive volatility in tax rates.

Posted by at 9:49 AM

Labels: Global Housing Watch

Subscribe to: Posts