Saturday, November 24, 2018

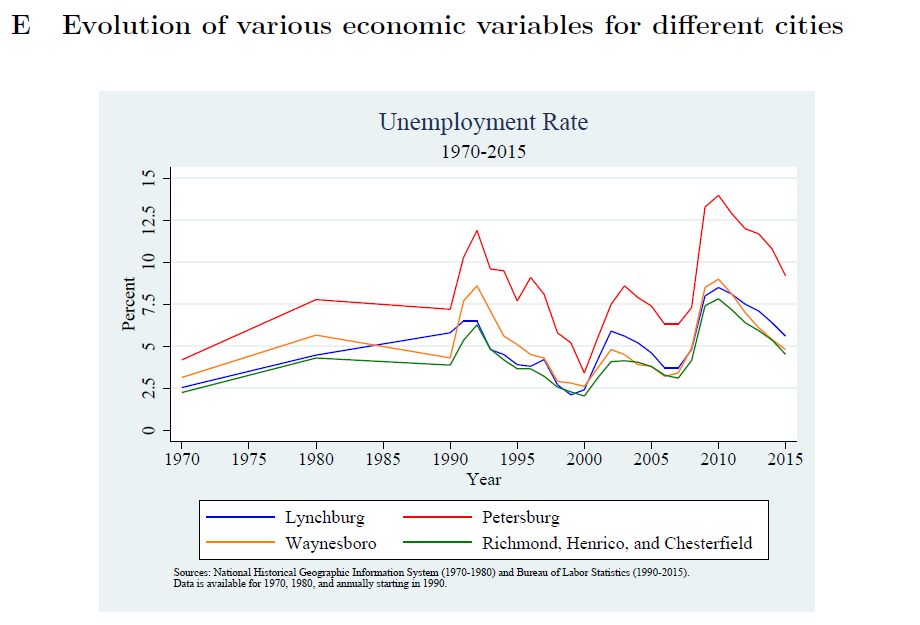

Distance and Decline: The Case of Petersburg, Virginia

From a new FRB Richmond Working Paper:

“Following two centuries of general economic prosperity, Petersburg has experienced a prolonged period of decline. A fixed-boundary city combined with a shrinking population may have left the city vulnerable to negative economic shocks as city officials faced “fixed” municipal costs in a context of declining tax revenues. When large layoffs occurred beginning in the 1980s, the city appears to have lost residents, especially higher-skilled residents, to the Richmond suburbs north of the city. Additionally, a new regional shopping center in neighboring Colonial Heights drained the city of retail tax revenues. These development led to a prolonged period of decline in the city.

But other Virginia cities also experienced substantial layoffs around the same time as Petersburg, yet they did not decline to the same degree. The question is why? We model two scenarios. The first incorporates two cities, one relatively economically vibrant and the other less so. We show that a negative productivity shock to the less vibrant city will lead to an outflow of high-skill workers to the more vibrant neighboring city along with higher-value homes. As tax revenues fall, the city experiences fiscal decline, which amplifies and reinforces its decline.

We also model an isolated city in which a negative shock does not result in as large of an outflow of high-skilled workers. In this setting, the city experiences a loss in aggregate utility for residents but is in a better position to weather the shock and eventually return to a path of economic growth.

Evidence from several Virginia cities is consistent with the implications of the models. In Petersburg, the period after the shocks saw high-income residents and higher home price areas decrease in the city and increase in areas closer to Richmond. As higher-skilled workers left, the population of Petersburg got older and less well-educated. In contrast, isolated cities that experienced somewhat similar shocks showed less pronounced effects. We conclude that Petersburg was a victim of being “too close” to Richmond, and as residents and the tax base left the city, an inability to scale down city municipal costs led to the severe fiscal difficulties seen today.”

From a new FRB Richmond Working Paper:

“Following two centuries of general economic prosperity, Petersburg has experienced a prolonged period of decline. A fixed-boundary city combined with a shrinking population may have left the city vulnerable to negative economic shocks as city officials faced “fixed” municipal costs in a context of declining tax revenues. When large layoffs occurred beginning in the 1980s, the city appears to have lost residents, especially higher-skilled residents,

Posted by at 7:14 PM

Labels: Inclusive Growth

Friday, November 23, 2018

Housing View – November 23, 2018

On cross-country:

- Housing in Europe: a different continent – a continent of differences – Journal of Housing Economics

- Can Monetary Policy lean against Housing Bubbles? – University of Pretoria

On the US:

- Why the Housing Market Is Slumping Despite a Booming Economy – New York Times

- The Renovation Rebalance: How Financial Intermediaries Affect Renter Housing Costs – Harvard University

- Mortgage Leverage and House Prices – Northwestern University

- Measuring Housing Insecurity in the American Housing Survey – HUD

- What explains the homeownership gap between black and white young adults? – Urban Institute

- Rental Housing Affordability in the Southeast: Data from the Sixth District – Federal Reserve Bank of Atlanta

- 81 Percent of Homes in the San Francisco Metro Area Are Worth More Than $1 Million. That’s Not Normal. – Reason

- LendingTree Reveals the Cities with the Most Foreign-born Homeowners – LendingTree

- Housing Perspectives: How Many Homeowners May Have Missed the Window to Refinance? – Harvard Joint Center for Housing Studies

- California Fires Only Add to Acute Housing Crisis – New York Times

- Real Estate Technology: Try, Try Again – New York Times

- The U.S. Housing Market: Despite a Demographic Push, Proceed With Caution – Pacific Union International

- Housing can’t both be a good investment and be affordable – City Observatory

- Redefault Risk in the Aftermath of the Mortgage Crisis: Why Did Modifications Improve More Than Self-Cures? – Federal Reserve Bank of Philadelphia

- The Homeless Crisis Is Getting Worse in America’s Richest Cities – Bloomberg

- S. Housing Starts Rise as Apartment Groundbreaking Gains – Bloomberg

On other countries:

- [Canada] Housing affordability worsens again in Q3 2018 – National Bank of Canada

- [Canada] Goodbye Vancouver. Canada’s Great Housing Boom Is Shifting North – Bloomberg

- [China] Qué son las “ciudades fantasma” de China y por qué son una pesadilla para la segunda economía mundial – BBC

- [United Kingdom] Mortgage payments to swell for first-time buyers – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Housing in Europe: a different continent – a continent of differences – Journal of Housing Economics

- Can Monetary Policy lean against Housing Bubbles? – University of Pretoria

On the US:

- Why the Housing Market Is Slumping Despite a Booming Economy – New York Times

- The Renovation Rebalance: How Financial Intermediaries Affect Renter Housing Costs – Harvard University

- Mortgage Leverage and House Prices – Northwestern University

- Measuring Housing Insecurity in the American Housing Survey – HUD

- What explains the homeownership gap between black and white young adults?

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, November 22, 2018

Economic Growth and Carbon Emissions

From a new paper by Enno Schröder and Servaas Storm:

“The unmistakably alarmist tone of the ‘Hothouse Earth’ article stands in contrast to more upbeat reports that there has been a delinking between economic growth and carbon emissions in recent times, at least in the world’s richest countries and possibly even more globally. The view that decoupling is not only possible, but already happening in real time, is a popular position in global and national policy discourses on COP21. To illustrate, in a widely read Science article titled ‘The irreversible momentum of clean energy’, erstwhile U.S. President Barack Obama (2017), argues that the U.S. economy could continue growing without increasing CO2 emissions thanks to the rollout of renewable energy technologies. Drawing on evidence from the report of his Council of Economic Advisers (2017), Obama claims that during the course of his presidency the American economy grew by more than 10% despite a 9.5% fall in CO2 emissions from the energy sector. “…this “decoupling” of energy sector emissions and economic growth,’ writes Obama with his usual eloquence, “should put to rest the argument that combating climate change requires accepting lower growth or a lower standard of living.

(…) And International Monetary Fund economists Cohen, Tovar Jalles, Loungani and Marto (2018), using trend/cycle decomposition techniques, find some evidence of decoupling for the period 1990-2014, particularly in European countries and especially when emissions measures are production-based. The essence of the decoupling thesis is captured well by the title of the OECD (2017) report ‘Investing in Climate, Investing in Growth’. The OECD report, prepared in the context of the German G20 Presidency, argues that the G20 countries can achieve ‘strong’ and ‘inclusive’ economic growth at the same time as reorienting their economies towards development pathways featuring substantially lower GHG emissions.”

From a new paper by Enno Schröder and Servaas Storm:

“The unmistakably alarmist tone of the ‘Hothouse Earth’ article stands in contrast to more upbeat reports that there has been a delinking between economic growth and carbon emissions in recent times, at least in the world’s richest countries and possibly even more globally. The view that decoupling is not only possible, but already happening in real time, is a popular position in global and national policy discourses on COP21.

Posted by at 8:14 AM

Labels: Energy & Climate Change

Wednesday, November 21, 2018

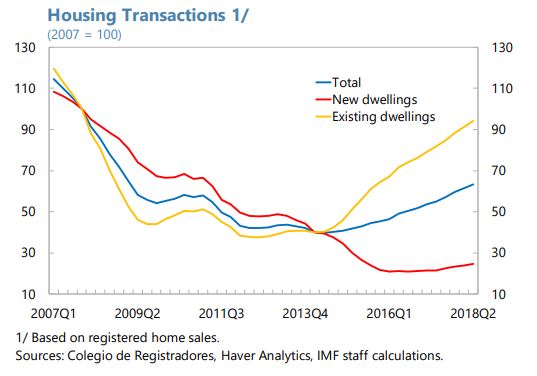

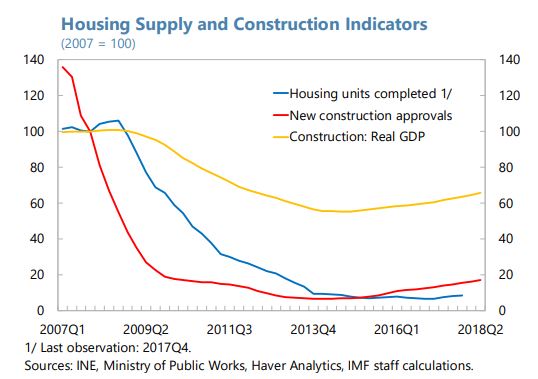

Developments in Spain’s Housing Market: Already a Cause of Concern?

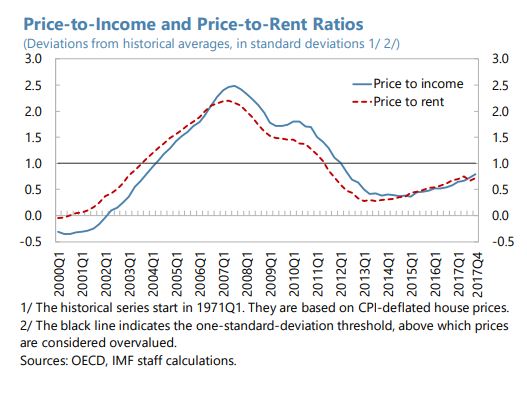

From the IMF’s latest report on Spain:

“House prices have increased in recent years, although from a low level and without signs of a construction boom. While there is no clear evidence of a significant price misalignment yet, the authorities need to be vigilant. The set of macroprudential tools should be expanded to deal with potential financial stability risks.

The ongoing price recovery is not associated with a construction boom. House prices have increased by around 15 percent between 2014–17, boosted by fast recoveries in cities like Madrid and Barcelona. Registered sales have disproportionately risen among existing dwellings, whereas new-dwelling transactions are still well below their pre-crisis peak. Despite early signs of mild supply-side recovery, such as an increase in new construction approvals from a low level, the housing stock has barely risen so far. In the overall economy, the contribution of value added from the construction sector is nearly half of what it was before the crisis. These trends have been accompanied by a small decline in home ownership (from 80 to 77 percent between 2008–17), while renting activity has strengthened. Against this background, new rent subsidy programs and social home loans were recently introduced. The authorities are also considering expanding the social housing stock.

Although house prices are rising, there is no strong evidence of a clear overvaluation yet. Two approaches are used to assess house price misalignment. The first approach measures deviations from historical averages of the price-to-rent and the price-to income ratios. As of 2017:Q4, both ratios stand at roughly similar levels as in mid-2003 and less than one standard deviation above their historical averages, thus indicating no overvaluation. The second approach is a regression that includes the growth rates of income per capita, working-age population, interest rates, equity prices, and construction costs, as well as a long-term equilibrium relationship with the price-to-income ratio, which measures housing

affordability. This model suggests a slight overvaluation in 2017:Q4. However, this regression-based result should be treated with caution given that the model is particularly

limited in capturing supply-side dynamics.To prevent financial stability risks emerging, the macroprudential toolkit should be expanded and ready to be used. While housing valuation gaps are not significant so far and households’ balance sheets have gradually improved since 2012, persistent demand pressures in the housing market could increase risks to financial stability. As noted in the 2017 FSAP, banks are highly exposed to real estate sector developments, and therefore the macroprudential toolkit should be expanded to deal with risks associated with that exposure (see IMF Country Reports No. 17/321 and 17/336). Other actions would be welcome to: (i) further improve balance sheets in the construction and real estate sectors; (ii) encourage greater use of fixed-rate mortgages; (iii) ensure that eligibility criteria for social home loans and rent subsidies are prudently assessed; and (iv) improve housing development regulation to address supply constraints. Any new measures aimed at reducing rent pressures should avoid causing negative supply-side effects with adverse impact on low-income renters.”

From the IMF’s latest report on Spain:

“House prices have increased in recent years, although from a low level and without signs of a construction boom. While there is no clear evidence of a significant price misalignment yet, the authorities need to be vigilant. The set of macroprudential tools should be expanded to deal with potential financial stability risks.

The ongoing price recovery is not associated with a construction boom.

Posted by at 1:34 PM

Labels: Global Housing Watch

Tuesday, November 20, 2018

The Evolution of Zipf’s Law for U.S. Cities

From a new working paper by Angelina Hackmann and Torben Klarl:

“Exploiting the cascade structure of cities and based on a dataset for U.S. cities between 1840 and 2016, the aim of this short paper is to answer three important questions: First, do we

observe that the U.S. city size distribution exhibits a smooth transition to Zipf’s law from the beginning or are there periods showing a pronounced departure from Zipf’s law? Second, if we observe periods of departure, which alternative laws instead should be used to accurately describe the city size distribution? Third, employing information from the cascade structure of cities, do we always find evidence for primate cities for a specific period of time? Inter alia, we find that the exact Zipf’s law has evolved over time from the more general, so-called threeparameter Zipf’s law which can be traced back to Mandelbrot (1982).”

From a new working paper by Angelina Hackmann and Torben Klarl:

“Exploiting the cascade structure of cities and based on a dataset for U.S. cities between 1840 and 2016, the aim of this short paper is to answer three important questions: First, do we

observe that the U.S. city size distribution exhibits a smooth transition to Zipf’s law from the beginning or are there periods showing a pronounced departure from Zipf’s law?

Posted by at 9:30 AM

Labels: Global Housing Watch

Subscribe to: Posts