Tuesday, December 11, 2018

Media Sentiment and International Asset Prices

From a new IMF working paper by Samuel P. Fraiberger, ; Do Lee, Damien Puy, and Romain Ranciere:

“We assess the impact of media sentiment on international equity prices using more than 4.5 million Reuters articles published across the globe between 1991 and 2015. News sentiment robustly predicts daily returns in both advanced and emerging markets, even after controlling for known determinants of stock prices. But not all news-sentiment is alike. A local (country-specific) increase in news optimism (pessimism) predicts a small and transitory increase (decrease) in local returns. By contrast, changes in global news sentiment have a larger impact on equity returns around the world, which does not reverse in the short run. We also find evidence that news sentiment affects mainly foreign – rather than local – investors: although local news optimism attracts international equity flows for a few days, global news optimism generates a permanent foreign equity inflow. Our results confirm the value of media content in capturing investor sentiment.”

From a new IMF working paper by Samuel P. Fraiberger, ; Do Lee, Damien Puy, and Romain Ranciere:

“We assess the impact of media sentiment on international equity prices using more than 4.5 million Reuters articles published across the globe between 1991 and 2015. News sentiment robustly predicts daily returns in both advanced and emerging markets, even after controlling for known determinants of stock prices. But not all news-sentiment is alike.

Posted by at 10:01 AM

Labels: Macro Demystified

Drivers of commodity price booms and busts in the long run

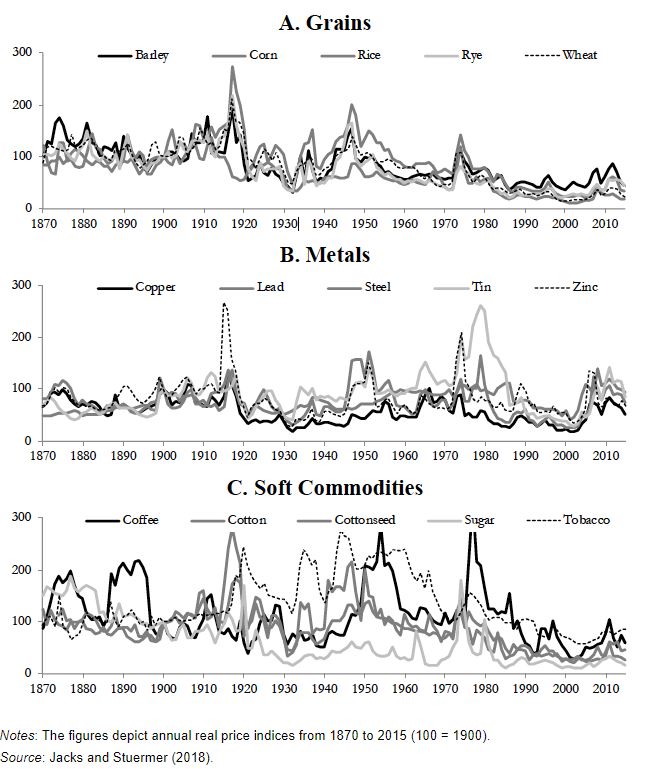

From a VoxEU post by David Jacks, and Martin Stuermer:

“There is a lack of consensus on the importance of various drivers of long-run commodity prices. This column analyses a new dataset of prices and production for 15 commodities, including metals, agricultural goods, and soft commodities, between 1870 and 2015. Demand shocks due to rapid industrialisation and urbanisation have driven a substantial amount of variation in commodity price booms. While demand shocks have gained importance over time, commodity supply shocks have become less relevant.

Understanding the drivers of commodity price booms and busts is of first-order importance for the global economy. A significant portion of real income and welfare in both commodity-consuming and commodity-producing nations hinges upon these prices (Bernanke 2006). They vitally affect the distribution of income within particular nations as the ownership of natural resources varies widely, potentially setting the stage for civil conflict (Dube and Vargas 2013). And the long-run drivers of commodity prices have serious implications for the formation and persistence of growth-detracting and growth-enhancing institutions (van der Ploeg 2011).

But for all this, outside spectators – whether they are academics, the general public, the investment community, or policymakers – remain divided in assigning the importance of various forces in the determination of commodity price booms and busts. Understanding which shocks drive these events and how long they persist is important for the conduct of macroeconomic policy, formulating environmental and resource policies, and, perhaps most importantly, investment decisions in the resource sectors of the global economy.

While the literature on modelling oil markets has examined a handful of booms and busts since the early 1970s (e.g. Kilian 2009, Kilian and Murphy 2014), our analysis of commodity markets is based on a new dataset of real prices and output for 15 grains, metals, and soft commodities from 1870 to 2015 (Jacks and Stuermer 2018). Unanticipated changes in world demand affect all commodity prices simultaneously. Throughout history, aggregate commodity demand shocks due to rapid industrialisation and urbanisation have driven commodity price booms. China’s recent effect on commodity markets is, thus, not a new phenomenon.

Commodities in the long run and identifying price shocks

A new dataset encompassing global output and real prices for 15 commodities – barley, coffee, copper, corn, cotton, cottonseed, lead, rice, rye, steel, sugar, tin, tobacco, wheat, and zinc – has been assembled covering the past 145 years (see Figure 1) and representing in excess of $2.5 trillion in annual gross value of production in 2015. The commodity markets selected exhibit characteristics that make such long-run analysis feasible: a high degree of product homogeneity, long-standing evidence of an integrated world market, and no indication of sudden changes in how the commodity is used. Thus, they have desirable characteristics that commodities such as crude oil or iron ore have only gained relatively recently.

Figure 1 Booms and busts are not new phenomena

Continue reading here.

From a VoxEU post by David Jacks, and Martin Stuermer:

“There is a lack of consensus on the importance of various drivers of long-run commodity prices. This column analyses a new dataset of prices and production for 15 commodities, including metals, agricultural goods, and soft commodities, between 1870 and 2015. Demand shocks due to rapid industrialisation and urbanisation have driven a substantial amount of variation in commodity price booms.

Posted by at 9:59 AM

Labels: Energy & Climate Change

Optimal Control of a Global Model of Climate Change with Adaptation and Mitigation

From a new IMF working paper by Manoj Atolia, Prakash Loungani, Helmut Maurer, and Willi Semmler:

“The Integrated Assessment Model (IAM) has extensively treated the adverse effects of climate change and the appropriate mitigation policy. We extend such a model to include optimal policies for mitigation, adaptation and infrastructure investment studying the dynamics of the transition to a low fossil-fuel economy. We focus on the adverse effects of increase in atmospheric CO2 concentration on households. Formally, the model gives rise to an optimal control problem of finite horizon consisting of a dynamic system with five-dimensional state vector consisting of stocks of private capital, green capital, public capital, stock of brown energy in the ground, and emissions. Given the numerous challenges to climate change policies the control vector is also five-dimensional. Our solutions are characterized by turnpike property and the optimal policy that accomplishes the objective of keeping the CO2 levels within bound is characterized by a significant proportion of investment in public capital going to mitigation in the initial periods. When initial levels of CO2 are high, adaptation efforts also start immediately, but during the initial period, they account for a smaller proportion of government’s public investment.”

From a new IMF working paper by Manoj Atolia, Prakash Loungani, Helmut Maurer, and Willi Semmler:

“The Integrated Assessment Model (IAM) has extensively treated the adverse effects of climate change and the appropriate mitigation policy. We extend such a model to include optimal policies for mitigation, adaptation and infrastructure investment studying the dynamics of the transition to a low fossil-fuel economy. We focus on the adverse effects of increase in atmospheric CO2 concentration on households.

Posted by at 9:55 AM

Labels: Energy & Climate Change

Friday, December 7, 2018

Overfitting in Judgment-based Economic Forecasts: The Case of IMF Growth Projections

From a new IMF working paper:

“I regress real GDP growth rates on the IMF’s growth forecasts and find that IMF forecasts behave similarly to those generated by overfitted models, placing too much weight on observable predictors and underestimating the forces of mean reversion. I identify several such variables that explain forecasts well but are not predictors of actual growth. I show that, at long horizons, IMF forecasts are little better than a forecasting rule that uses no information other than the historical global sample average growth rate (i.e., a constant). Given the large noise component in forecasts, particularly at longer horizons, the paper calls into question the usefulness of judgment-based medium and long-run forecasts for policy analysis, including for debt sustainability assessments, and points to statistical methods to improve forecast accuracy by taking into account the risk of overfitting.”

From a new IMF working paper:

“I regress real GDP growth rates on the IMF’s growth forecasts and find that IMF forecasts behave similarly to those generated by overfitted models, placing too much weight on observable predictors and underestimating the forces of mean reversion. I identify several such variables that explain forecasts well but are not predictors of actual growth. I show that, at long horizons, IMF forecasts are little better than a forecasting rule that uses no information other than the historical global sample average growth rate (i.e.,

Posted by at 5:48 PM

Labels: Forecasting Forum

You are needed but not your skills: Challenges to manufacturing workers in the wake of globalisation

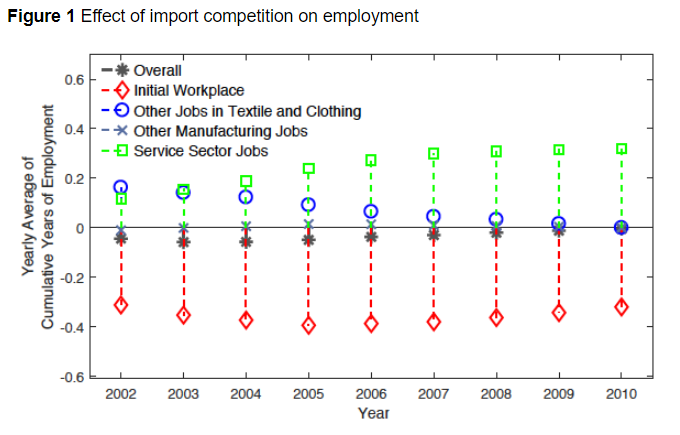

From a new VOX post:

“The impact of trade shocks on labour market shifts is usually studied in the context of re-training and social welfare frictions. Using evidence from Denmark, this column shows how workers can experience long-run reductions in earnings no matter how easy it is to change sector. A sudden and obligatory shift toward a new sector may, by its nature, generate some worker dissatisfaction.”

“Figure 1 shows the import competition-induced sectoral change. Each marker shows the causal effect of import competition in the corresponding year on employment at the respective job/sector indicated in the legend, as captured by the difference-in-difference specification with individual fixed effects.”

“The challenges faced by manufacturing workers, who once exemplified the middle class, have important implications for the whole society. My findings show that adjustment problems do not end once manufacturing workers find full-time jobs in the growing service sector. And the Danish labour market institutions, despite being successful in keeping the workers within the labour market and ensuring fast inter-sectoral movement as well as largely covering the earnings losses of workers with transfers, were not fully successful in relieving the pain of the people whose human capital is not relevant for service sector jobs. In the end one feels better when earning a living rather than getting a transfer, and when enjoying and taking pride in work rather than changing from one job to another due to skill mis-match. Thus, it may be unavoidable that a sudden and obligatory shift toward a new sector demanding new skills leads to dissatisfaction. Although, the social system in Denmark may be a factor in keeping the dissatisfaction within limits and preventing unwanted political consequences.”

From a new VOX post:

“The impact of trade shocks on labour market shifts is usually studied in the context of re-training and social welfare frictions. Using evidence from Denmark, this column shows how workers can experience long-run reductions in earnings no matter how easy it is to change sector. A sudden and obligatory shift toward a new sector may, by its nature, generate some worker dissatisfaction.”

“Figure 1 shows the import competition-induced sectoral change.

Posted by at 5:42 PM

Labels: Inclusive Growth

Subscribe to: Posts