Saturday, November 24, 2018

Is Inflation Domestic or Global? Evidence from Emerging Markets

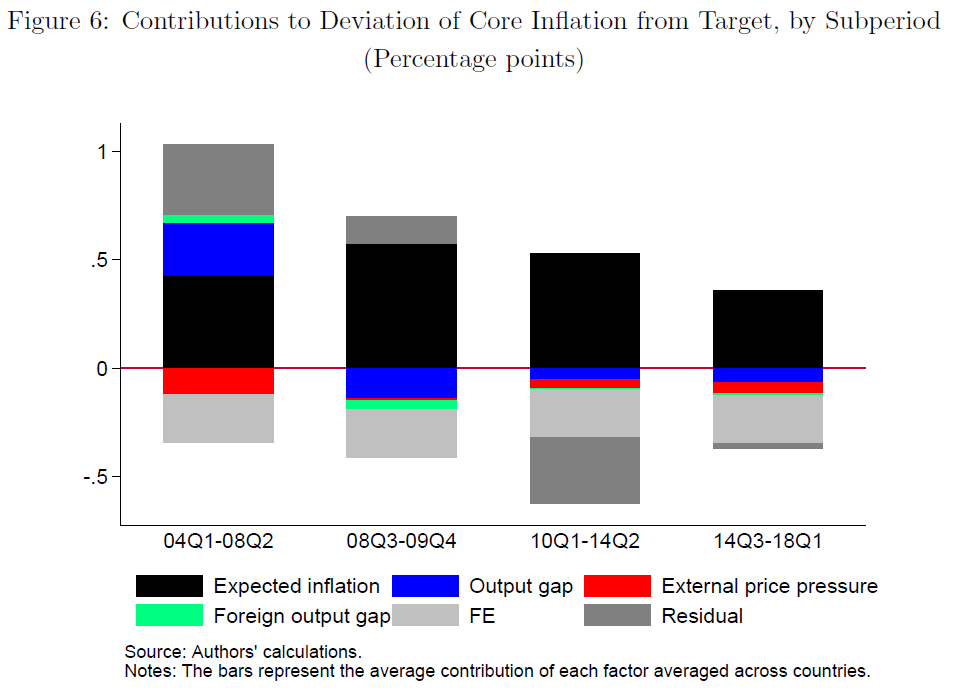

From a new IMF working paper:

“Following a period of disinflation during the 1990s and early 2000s, inflation in emerging markets has remained remarkably low. The volatility and persistence of inflation also fell considerably and remained low despite large swings in commodity prices, the global financial crisis, and periods of strong and sustained US dollar appreciation. A key question is whether this improved inflation performance is sustainable or rather reflects global disinflationary forces that could prove temporary. In this paper, we use a New-Keynesian Phillips curve framework and data for 19 large emerging market economies over 2004-18 to assess the contribution of domestic and global factors to domestic inflation dynamics. Our results suggest that longer-term inflation expectations, linked to domestic factors, were the main determinant of inflation. External factors played a considerably smaller role. The results underscore that although emerging markets are increasingly integrated into the global economy, policymakers remain largely in control of domestic inflation developments.”

From a new IMF working paper:

“Following a period of disinflation during the 1990s and early 2000s, inflation in emerging markets has remained remarkably low. The volatility and persistence of inflation also fell considerably and remained low despite large swings in commodity prices, the global financial crisis, and periods of strong and sustained US dollar appreciation. A key question is whether this improved inflation performance is sustainable or rather reflects global disinflationary forces that could prove temporary.

Posted by at 7:44 PM

Labels: Inclusive Growth

Populism and Civil Society

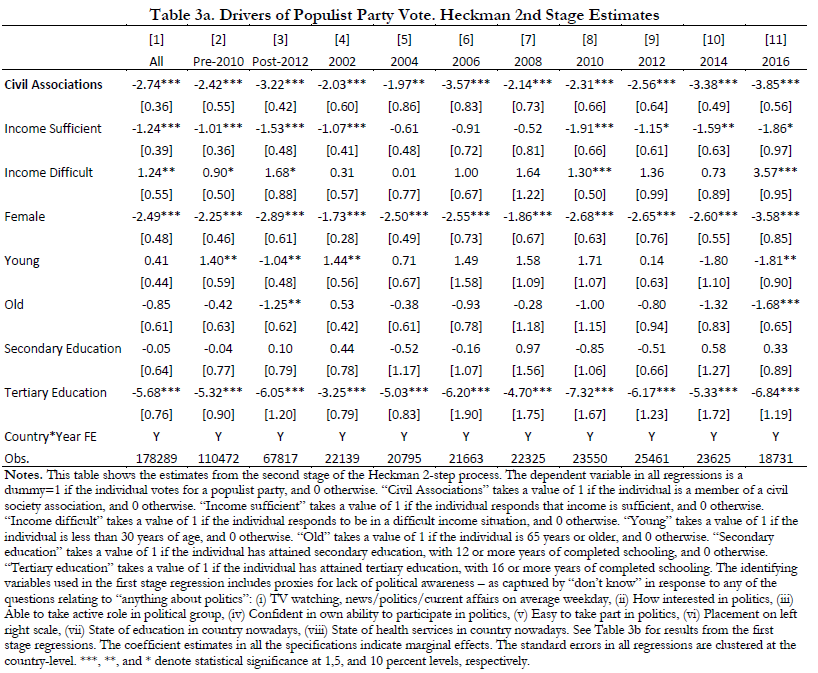

From a new IMF working paper:

“Populists claim to be the only legitimate representative of the people. Does it mean that there is no space for civil society? The issue is important because since Tocqueville (1835), associations and civil society have been recognized as a key factor in a healthy liberal democracy. We ask two questions: 1) do individuals who are members of civil associations vote less for populist parties? 2) does membership in associations decrease when populist parties are in power? We answer these questions looking at the experiences of Europe, which has a rich civil society tradition, as well as of Latin America, which already has a long history of populists in power. The main findings are that individuals belonging to associations are less likely by 2.4 to 4.2 percent to vote for populist parties, which is large considering that the average vote share for populist parties is from 10 to 15 percent. The effect is strong particularly after the global financial crisis, with the important caveat that membership in trade unions has unclear effects.”

From a new IMF working paper:

“Populists claim to be the only legitimate representative of the people. Does it mean that there is no space for civil society? The issue is important because since Tocqueville (1835), associations and civil society have been recognized as a key factor in a healthy liberal democracy. We ask two questions: 1) do individuals who are members of civil associations vote less for populist parties?

Posted by at 7:34 PM

Labels: Inclusive Growth

Solow on Friedman’s 1968 Presidential Address and the Medium Run

From a new post by Timothy Taylor:

“Robert Solow is a notable player in these disputes: in particular, in his 1960 paper with Paul Samuelson, “Analytical Aspects of Anti-Inflation Policy” (American Economic Review, 50:2, pp. 177-194). In an essay in the Winter 2000 issue of the Journal of Economic Perspectives, “Toward a Macroeconomics of the Medium Run,” Solow addressed this question of thinking about macroeconomic policy in the short- and the long-run. He wrote:

I can easily imagine that there is a “true” macrodynamics, valid at every time scale. But it is fearfully complicated, and nobody has a very good grip on it. At short time scales, I think, something sort of “Keynesian” is a good approximation, and surely better than anything straight “neoclassical.” At very long time scales, the interesting questions are best studied in a neoclassical framework, and attention to the Keynesian side of things would be a minor distraction. At the five-to-ten-year time scale, we have to piece things together as best we can, and look for a hybrid model that will do the job.

In this most recent essay, “A Theory is a Sometime Thing,” Solow pushes this idea of medium-run thinking harder. He acknowledges that if a central bank can only cause the interest rate and unemployment rate to shift for a year or two, in the short-run before a rebound to what is determined in the long run, then when problems of lags in timing are included, macroeconomic policy might be dysfunctional. But if a central bank can affect the interest rate and the unemployment rate for a medium-run period of, say 5-7 years, then even with some uncertainty and lags, macroeocnomic policy may be quite relevant and possible. At one point, Solow writes: “The medium run is where we live.””

From a new post by Timothy Taylor:

“Robert Solow is a notable player in these disputes: in particular, in his 1960 paper with Paul Samuelson, “Analytical Aspects of Anti-Inflation Policy” (American Economic Review, 50:2, pp. 177-194). In an essay in the Winter 2000 issue of the Journal of Economic Perspectives, “Toward a Macroeconomics of the Medium Run,” Solow addressed this question of thinking about macroeconomic policy in the short- and the long-run.

Posted by at 7:30 PM

Labels: Macro Demystified

Distance and Decline: The Case of Petersburg, Virginia

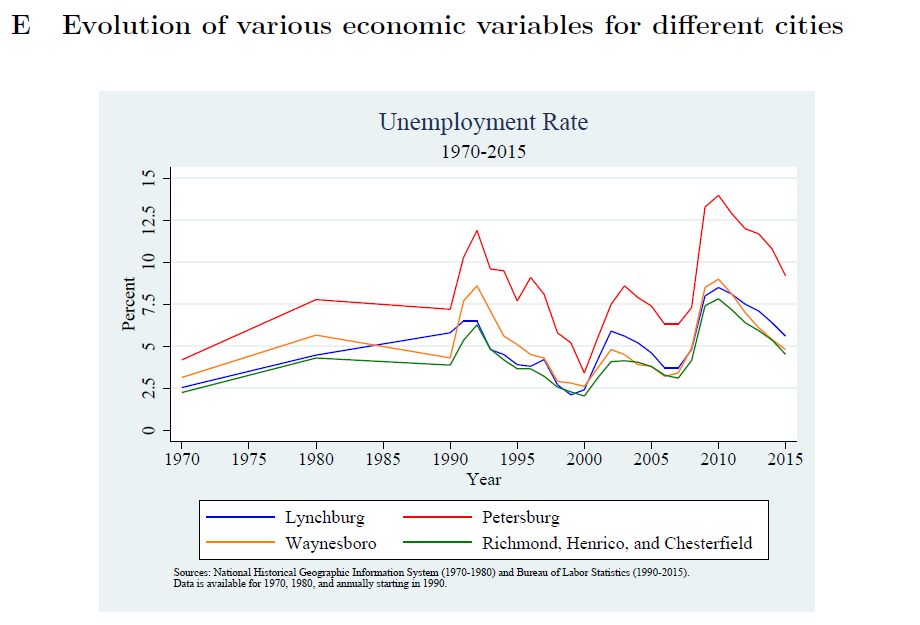

From a new FRB Richmond Working Paper:

“Following two centuries of general economic prosperity, Petersburg has experienced a prolonged period of decline. A fixed-boundary city combined with a shrinking population may have left the city vulnerable to negative economic shocks as city officials faced “fixed” municipal costs in a context of declining tax revenues. When large layoffs occurred beginning in the 1980s, the city appears to have lost residents, especially higher-skilled residents, to the Richmond suburbs north of the city. Additionally, a new regional shopping center in neighboring Colonial Heights drained the city of retail tax revenues. These development led to a prolonged period of decline in the city.

But other Virginia cities also experienced substantial layoffs around the same time as Petersburg, yet they did not decline to the same degree. The question is why? We model two scenarios. The first incorporates two cities, one relatively economically vibrant and the other less so. We show that a negative productivity shock to the less vibrant city will lead to an outflow of high-skill workers to the more vibrant neighboring city along with higher-value homes. As tax revenues fall, the city experiences fiscal decline, which amplifies and reinforces its decline.

We also model an isolated city in which a negative shock does not result in as large of an outflow of high-skilled workers. In this setting, the city experiences a loss in aggregate utility for residents but is in a better position to weather the shock and eventually return to a path of economic growth.

Evidence from several Virginia cities is consistent with the implications of the models. In Petersburg, the period after the shocks saw high-income residents and higher home price areas decrease in the city and increase in areas closer to Richmond. As higher-skilled workers left, the population of Petersburg got older and less well-educated. In contrast, isolated cities that experienced somewhat similar shocks showed less pronounced effects. We conclude that Petersburg was a victim of being “too close” to Richmond, and as residents and the tax base left the city, an inability to scale down city municipal costs led to the severe fiscal difficulties seen today.”

From a new FRB Richmond Working Paper:

“Following two centuries of general economic prosperity, Petersburg has experienced a prolonged period of decline. A fixed-boundary city combined with a shrinking population may have left the city vulnerable to negative economic shocks as city officials faced “fixed” municipal costs in a context of declining tax revenues. When large layoffs occurred beginning in the 1980s, the city appears to have lost residents, especially higher-skilled residents,

Posted by at 7:14 PM

Labels: Inclusive Growth

Friday, November 23, 2018

Housing View – November 23, 2018

On cross-country:

- Housing in Europe: a different continent – a continent of differences – Journal of Housing Economics

- Can Monetary Policy lean against Housing Bubbles? – University of Pretoria

On the US:

- Why the Housing Market Is Slumping Despite a Booming Economy – New York Times

- The Renovation Rebalance: How Financial Intermediaries Affect Renter Housing Costs – Harvard University

- Mortgage Leverage and House Prices – Northwestern University

- Measuring Housing Insecurity in the American Housing Survey – HUD

- What explains the homeownership gap between black and white young adults? – Urban Institute

- Rental Housing Affordability in the Southeast: Data from the Sixth District – Federal Reserve Bank of Atlanta

- 81 Percent of Homes in the San Francisco Metro Area Are Worth More Than $1 Million. That’s Not Normal. – Reason

- LendingTree Reveals the Cities with the Most Foreign-born Homeowners – LendingTree

- Housing Perspectives: How Many Homeowners May Have Missed the Window to Refinance? – Harvard Joint Center for Housing Studies

- California Fires Only Add to Acute Housing Crisis – New York Times

- Real Estate Technology: Try, Try Again – New York Times

- The U.S. Housing Market: Despite a Demographic Push, Proceed With Caution – Pacific Union International

- Housing can’t both be a good investment and be affordable – City Observatory

- Redefault Risk in the Aftermath of the Mortgage Crisis: Why Did Modifications Improve More Than Self-Cures? – Federal Reserve Bank of Philadelphia

- The Homeless Crisis Is Getting Worse in America’s Richest Cities – Bloomberg

- S. Housing Starts Rise as Apartment Groundbreaking Gains – Bloomberg

On other countries:

- [Canada] Housing affordability worsens again in Q3 2018 – National Bank of Canada

- [Canada] Goodbye Vancouver. Canada’s Great Housing Boom Is Shifting North – Bloomberg

- [China] Qué son las “ciudades fantasma” de China y por qué son una pesadilla para la segunda economía mundial – BBC

- [United Kingdom] Mortgage payments to swell for first-time buyers – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Housing in Europe: a different continent – a continent of differences – Journal of Housing Economics

- Can Monetary Policy lean against Housing Bubbles? – University of Pretoria

On the US:

- Why the Housing Market Is Slumping Despite a Booming Economy – New York Times

- The Renovation Rebalance: How Financial Intermediaries Affect Renter Housing Costs – Harvard University

- Mortgage Leverage and House Prices – Northwestern University

- Measuring Housing Insecurity in the American Housing Survey – HUD

- What explains the homeownership gap between black and white young adults?

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts