Thursday, November 22, 2018

Economic Growth and Carbon Emissions

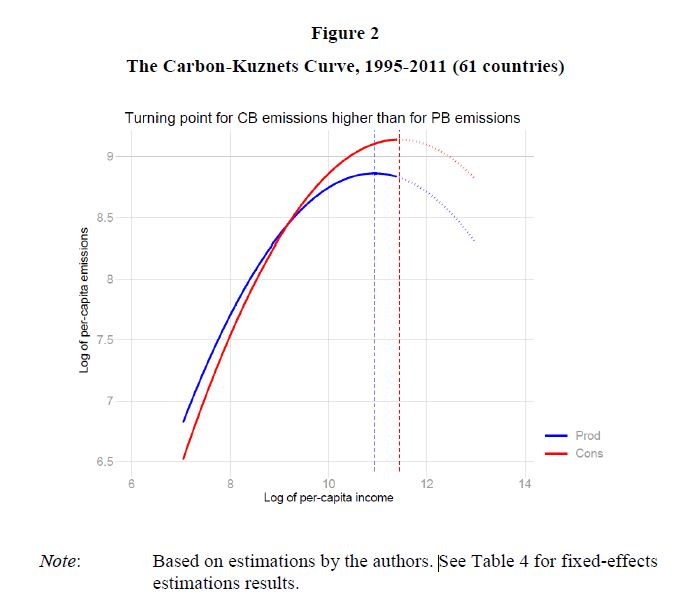

From a new paper by Enno Schröder and Servaas Storm:

“The unmistakably alarmist tone of the ‘Hothouse Earth’ article stands in contrast to more upbeat reports that there has been a delinking between economic growth and carbon emissions in recent times, at least in the world’s richest countries and possibly even more globally. The view that decoupling is not only possible, but already happening in real time, is a popular position in global and national policy discourses on COP21. To illustrate, in a widely read Science article titled ‘The irreversible momentum of clean energy’, erstwhile U.S. President Barack Obama (2017), argues that the U.S. economy could continue growing without increasing CO2 emissions thanks to the rollout of renewable energy technologies. Drawing on evidence from the report of his Council of Economic Advisers (2017), Obama claims that during the course of his presidency the American economy grew by more than 10% despite a 9.5% fall in CO2 emissions from the energy sector. “…this “decoupling” of energy sector emissions and economic growth,’ writes Obama with his usual eloquence, “should put to rest the argument that combating climate change requires accepting lower growth or a lower standard of living.

(…) And International Monetary Fund economists Cohen, Tovar Jalles, Loungani and Marto (2018), using trend/cycle decomposition techniques, find some evidence of decoupling for the period 1990-2014, particularly in European countries and especially when emissions measures are production-based. The essence of the decoupling thesis is captured well by the title of the OECD (2017) report ‘Investing in Climate, Investing in Growth’. The OECD report, prepared in the context of the German G20 Presidency, argues that the G20 countries can achieve ‘strong’ and ‘inclusive’ economic growth at the same time as reorienting their economies towards development pathways featuring substantially lower GHG emissions.”

From a new paper by Enno Schröder and Servaas Storm:

“The unmistakably alarmist tone of the ‘Hothouse Earth’ article stands in contrast to more upbeat reports that there has been a delinking between economic growth and carbon emissions in recent times, at least in the world’s richest countries and possibly even more globally. The view that decoupling is not only possible, but already happening in real time, is a popular position in global and national policy discourses on COP21.

Posted by at 8:14 AM

Labels: Energy & Climate Change

Wednesday, November 21, 2018

Developments in Spain’s Housing Market: Already a Cause of Concern?

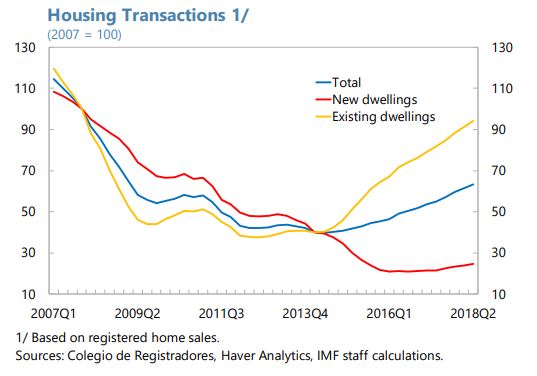

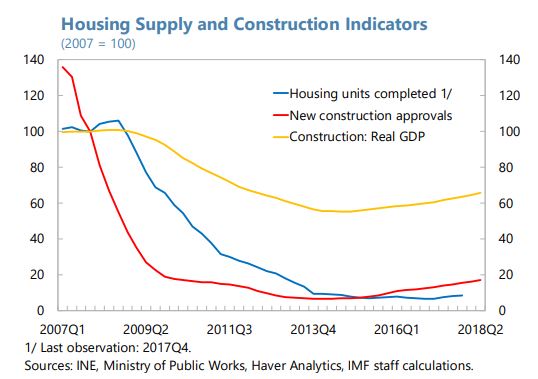

From the IMF’s latest report on Spain:

“House prices have increased in recent years, although from a low level and without signs of a construction boom. While there is no clear evidence of a significant price misalignment yet, the authorities need to be vigilant. The set of macroprudential tools should be expanded to deal with potential financial stability risks.

The ongoing price recovery is not associated with a construction boom. House prices have increased by around 15 percent between 2014–17, boosted by fast recoveries in cities like Madrid and Barcelona. Registered sales have disproportionately risen among existing dwellings, whereas new-dwelling transactions are still well below their pre-crisis peak. Despite early signs of mild supply-side recovery, such as an increase in new construction approvals from a low level, the housing stock has barely risen so far. In the overall economy, the contribution of value added from the construction sector is nearly half of what it was before the crisis. These trends have been accompanied by a small decline in home ownership (from 80 to 77 percent between 2008–17), while renting activity has strengthened. Against this background, new rent subsidy programs and social home loans were recently introduced. The authorities are also considering expanding the social housing stock.

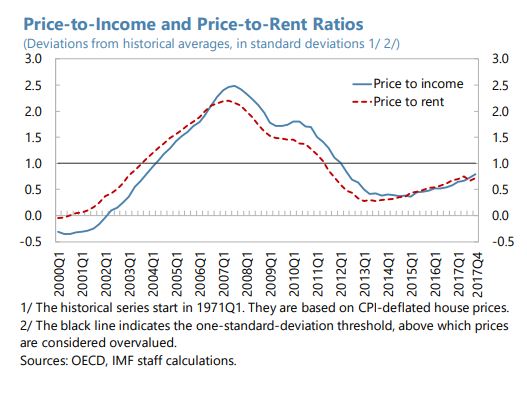

Although house prices are rising, there is no strong evidence of a clear overvaluation yet. Two approaches are used to assess house price misalignment. The first approach measures deviations from historical averages of the price-to-rent and the price-to income ratios. As of 2017:Q4, both ratios stand at roughly similar levels as in mid-2003 and less than one standard deviation above their historical averages, thus indicating no overvaluation. The second approach is a regression that includes the growth rates of income per capita, working-age population, interest rates, equity prices, and construction costs, as well as a long-term equilibrium relationship with the price-to-income ratio, which measures housing

affordability. This model suggests a slight overvaluation in 2017:Q4. However, this regression-based result should be treated with caution given that the model is particularly

limited in capturing supply-side dynamics.To prevent financial stability risks emerging, the macroprudential toolkit should be expanded and ready to be used. While housing valuation gaps are not significant so far and households’ balance sheets have gradually improved since 2012, persistent demand pressures in the housing market could increase risks to financial stability. As noted in the 2017 FSAP, banks are highly exposed to real estate sector developments, and therefore the macroprudential toolkit should be expanded to deal with risks associated with that exposure (see IMF Country Reports No. 17/321 and 17/336). Other actions would be welcome to: (i) further improve balance sheets in the construction and real estate sectors; (ii) encourage greater use of fixed-rate mortgages; (iii) ensure that eligibility criteria for social home loans and rent subsidies are prudently assessed; and (iv) improve housing development regulation to address supply constraints. Any new measures aimed at reducing rent pressures should avoid causing negative supply-side effects with adverse impact on low-income renters.”

From the IMF’s latest report on Spain:

“House prices have increased in recent years, although from a low level and without signs of a construction boom. While there is no clear evidence of a significant price misalignment yet, the authorities need to be vigilant. The set of macroprudential tools should be expanded to deal with potential financial stability risks.

The ongoing price recovery is not associated with a construction boom.

Posted by at 1:34 PM

Labels: Global Housing Watch

Tuesday, November 20, 2018

The Evolution of Zipf’s Law for U.S. Cities

From a new working paper by Angelina Hackmann and Torben Klarl:

“Exploiting the cascade structure of cities and based on a dataset for U.S. cities between 1840 and 2016, the aim of this short paper is to answer three important questions: First, do we

observe that the U.S. city size distribution exhibits a smooth transition to Zipf’s law from the beginning or are there periods showing a pronounced departure from Zipf’s law? Second, if we observe periods of departure, which alternative laws instead should be used to accurately describe the city size distribution? Third, employing information from the cascade structure of cities, do we always find evidence for primate cities for a specific period of time? Inter alia, we find that the exact Zipf’s law has evolved over time from the more general, so-called threeparameter Zipf’s law which can be traced back to Mandelbrot (1982).”

From a new working paper by Angelina Hackmann and Torben Klarl:

“Exploiting the cascade structure of cities and based on a dataset for U.S. cities between 1840 and 2016, the aim of this short paper is to answer three important questions: First, do we

observe that the U.S. city size distribution exhibits a smooth transition to Zipf’s law from the beginning or are there periods showing a pronounced departure from Zipf’s law?

Posted by at 9:30 AM

Labels: Global Housing Watch

Monday, November 19, 2018

Belize: Climate Change Policy Assessment

From the IMF’s latest report on Belize:

“Belize is exceptionally vulnerable to natural disasters and climate change. It already faces hurricanes, flooding, sea level rise, coastal erosion, coral bleaching, and droughts, with impacts likely to intensify given expected increases in weather volatility and sea temperature. Hence, planning for resilience-building, and engagement with development partners on environmental reforms, have been central to Belizean policy-making for many years, since well before Belize submitted its Nationally Determined Contribution (NDC) to the Paris Accord in 2015.

This Climate Change Policy Assessment (CCPA) takes stock of Belize’s plans to manage its climate response, from the perspective of their macroeconomic and fiscal implications. The CCPA is a joint initiative by the IMF and World Bank to assist small states to understand and manage the expected economic impact of climate change, while safeguarding long-run fiscal and external sustainability. It explores the possible impact of climate change and natural disasters on the macroeconomy and the cost of Belize’s planned response. It suggests macroeconomically relevant reforms that could strengthen the likelihood of success of the national strategy and identifies policy gaps and resource needs.

- General preparedness for climate change. Belize’s planned climate response is well articulated. Its NDC includes a clear strategy with relatively well-developed costing for its mitigation and adaptation activities. But while climate planning is advanced and consistent with the broader development strategy (GSDS), implementation capacity remains a challenge. Belize has strong physical emergency planning but receives comparatively little disaster aid and falls short on longer-term financial provisioning.

- Mitigation. Belize plans to meet its NDC mitigation goals by expanding its already relatively high share of renewable energy further (from 57 percent to 85 percent of electricity supply), reducing energy intensity and fossil fuel use in transport, and protecting forest reserves and improving sustainable forest management. Given its already-reduced dependence on fossil fuels, and its need to preserve competitiveness with Caribbean neighbors, it has limited scope to raise carbon taxes unilaterally; however, feebates could improve the mitigation incentives in the tax system.

Continue reading here.

From the IMF’s latest report on Belize:

“Belize is exceptionally vulnerable to natural disasters and climate change. It already faces hurricanes, flooding, sea level rise, coastal erosion, coral bleaching, and droughts, with impacts likely to intensify given expected increases in weather volatility and sea temperature. Hence, planning for resilience-building, and engagement with development partners on environmental reforms, have been central to Belizean policy-making for many years, since well before Belize submitted its Nationally Determined Contribution (NDC) to the Paris Accord in 2015.

Posted by at 9:21 AM

Labels: Energy & Climate Change

Monetary policy and climate change

From a speech by Benoît Cœuré, Member of the Executive Board of the European Central Bank:

“2018 has seen one of the hottest summers in Europe since weather records began.[1]Increasing weather extremes, rising sea levels and Arctic melting are now clearly visible consequences of human-induced warming.[2] Climate change is not a theory. It is a fact.

While only one dimension of the human cost, the consequences in macroeconomic terms look set to be large. Without further mitigation, cumulative emissions pose significant risks of economic disruption.[3]

While there is a wide recognition that environmental externalities should be primarily corrected by first-best policies, such as taxes[4], all authorities, including the ECB, need to reflect on, and consider, the appropriate response to climate change.

In recent years, central bankers, led by Bank of England Governor Mark Carney, have started discussing the financial stability implications of climate change.[5] The first tangible results are trickling in. The Financial Stability Board’s Task Force on Climate-related Financial Disclosures published its first status report just a few weeks ago. Only last week, ECB Banking Supervision communicated to banks that climate-related risks have been identified as being among the key risk drivers affecting the euro area banking system.

And, of course, the Central Banks and Supervisors Network for Greening the Financial System published its first progress report just a few weeks ago, reasserting that climate-related risks fall squarely within the supervisory and financial stability mandates of central banks and supervisors.

An area that has received less attention though, both in policy and in academia, is the impact of climate change on the conduct of monetary policy. Today I would like to contribute to this debate and offer a way of thinking about how climate change fits into our current monetary policy framework – the way we react to shocks and the way we think policy propagates through the economy – and how it may affect our monetary policy implementation.

I will argue that climate change can be expected to affect monetary policy one way or the other. That is, if left unchecked, it may further complicate the correct identification of shocks relevant for the medium-term inflation outlook, it may increase the likelihood of extreme events and hence erode central banks’ conventional policy space more often, and it may raise the number of occasions on which central banks face a trade-off forcing them to prioritise stable prices over output.

In the more desirable scenario in which humankind rises to the climate change challenge, the implications for monetary policy could be equally far-reaching, in particular if the associated shift in the energy mix changes relative prices to an extent that risks destabilising medium-term inflation expectations.

I will also argue that there is scope for central banks themselves to play a supporting role in mitigating the risks associated with climate change while staying within our mandate.”

Continue reading here.

From a speech by Benoît Cœuré, Member of the Executive Board of the European Central Bank:

“2018 has seen one of the hottest summers in Europe since weather records began.[1]Increasing weather extremes, rising sea levels and Arctic melting are now clearly visible consequences of human-induced warming.[2] Climate change is not a theory. It is a fact.

While only one dimension of the human cost,

Posted by at 9:13 AM

Labels: Energy & Climate Change

Subscribe to: Posts