Thursday, May 24, 2018

Housing Market in Estonia

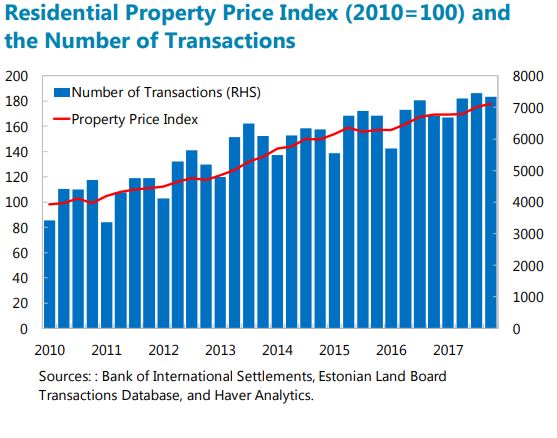

The IMF’s latest report on Estonia says:

“Residential real estate market activity has increased, but prices remain well anchored to income and nominal GDP growth (figures below). The number of transactions in 2017 rose by

8 percent compared to the level in 2016 and the real estate price index increased by 5 percent, driven partly by the growing share of new apartments. Going forward, the number of permit applications suggest construction activity should be sufficient to just maintain the current housing stock.”

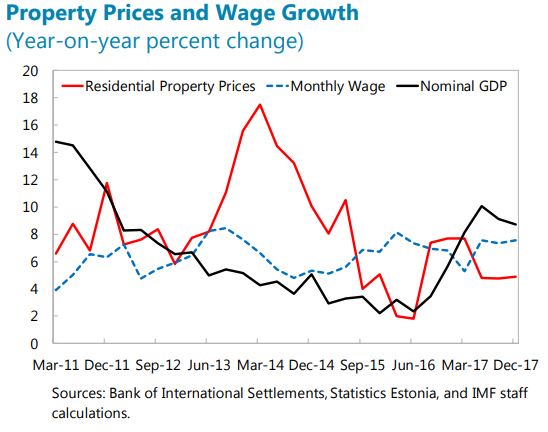

The report also says that: “Housing market trends, both domestic and abroad, are important drivers of banking sector developments in Estonia. While household indebtedness is moderate, banks’ extension of housing loans accelerated in 2017. Higher interest rates following an eventual monetary policy normalization could pose a risk for household finances and potentially affect future financial developments and economic growth. In addition, developments in cross-border banking linkages indicate that potential spillovers from vulnerabilities in Nordic parent banks, notably the Swedish real estate sector, require further safeguards for financial stability, notably in cross-border banking supervision through the Nordic-Baltic cooperation platform.”

The IMF’s latest report on Estonia says:

“Residential real estate market activity has increased, but prices remain well anchored to income and nominal GDP growth (figures below). The number of transactions in 2017 rose by

8 percent compared to the level in 2016 and the real estate price index increased by 5 percent, driven partly by the growing share of new apartments. Going forward, the number of permit applications suggest construction activity should be sufficient to just maintain the current housing stock.”

Posted by at 5:31 PM

Labels: Global Housing Watch

Tuesday, May 22, 2018

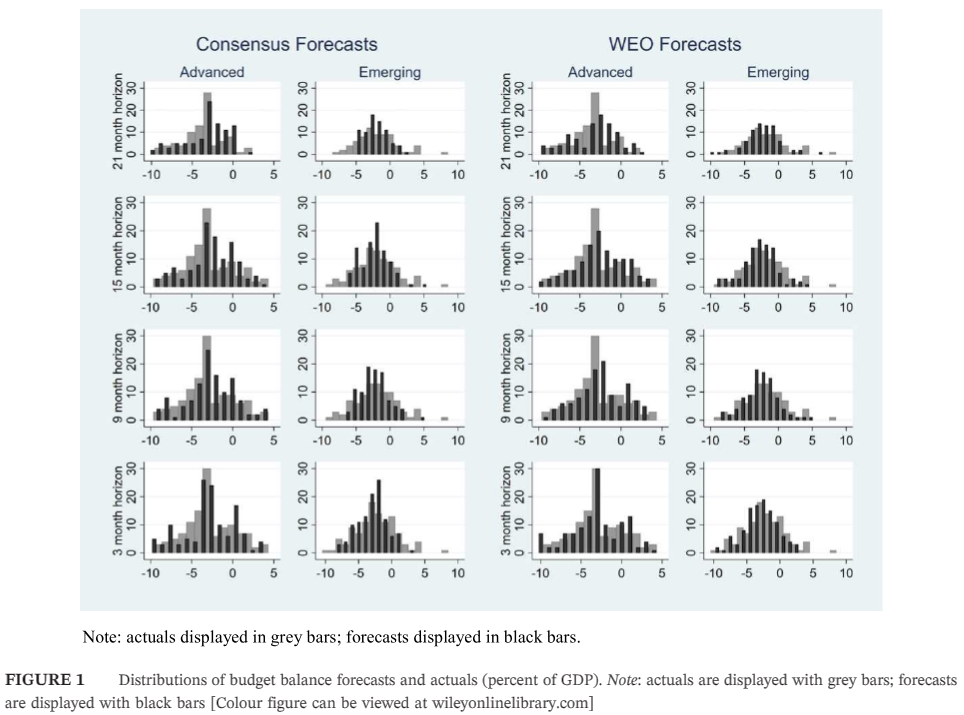

Do IMF fiscal forecasts add value?

My new paper with Zidong An, Joao Jalles, and Ricardo M. Sousa was just published in Journal of Forecasting:

“We used a panel of 29 advanced and emerging market countries to investigate whether the IMF’s World Economic Outlook (WEO) fiscal forecasts add value in terms of forecast accuracy and information content, relative to private sector forecasts (from Consensus Economics). We find that: (i) WEO forecasts are not significantly less accurate than Consensus forecasts; (ii) WEO and Consensus forecasts tend to mutually encompass one another; and (iii) each source of forecasts appears to contain some information that is not embedded in the other source.”

My new paper with Zidong An, Joao Jalles, and Ricardo M. Sousa was just published in Journal of Forecasting:

“We used a panel of 29 advanced and emerging market countries to investigate whether the IMF’s World Economic Outlook (WEO) fiscal forecasts add value in terms of forecast accuracy and information content, relative to private sector forecasts (from Consensus Economics). We find that: (i) WEO forecasts are not significantly less accurate than Consensus forecasts;

Posted by at 11:27 AM

Labels: Forecasting Forum

The FOMC versus the Staff, Revisited: When do Policymakers Add Value?

A new paper finds that “policymakers’ value-added is greater when economic conditions are unfavorable or uncertain.” “[…] in certain circumstances, the value of the FOMC’s informational advantage and judgement-based adjustments to the staff forecasts is greater. The use of explicit formal models for quantitative macroeconomic forecasting proliferated in the 1960s, but forecasters typically adjust the model-based forecasts using their own judgment (Wallis, 1989). There is mixed evidence on the value of “judgmental adjustments,” which can introduce psychological biases but can also compensate for model limitations, and

may be especially valuable when economic events lack close historical precedents (McNees, 1990).”

A new paper finds that “policymakers’ value-added is greater when economic conditions are unfavorable or uncertain.” “[…] in certain circumstances, the value of the FOMC’s informational advantage and judgement-based adjustments to the staff forecasts is greater. The use of explicit formal models for quantitative macroeconomic forecasting proliferated in the 1960s, but forecasters typically adjust the model-based forecasts using their own judgment (Wallis, 1989). There is mixed evidence on the value of “judgmental adjustments,”

Posted by at 11:11 AM

Labels: Forecasting Forum

Yes, we should fear the robot revolution

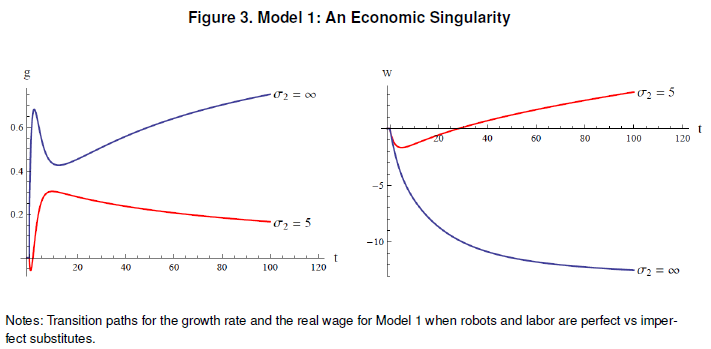

From a new IMF working paper by Andrew Berg, Edward Buffie, and Luis-Felipe Zanna:

“Advances in artificial intelligence and robotics may be leading to a new industrial revolution. This paper presents a model with the minimum necessary features to analyze the implications for inequality and output. Two assumptions are key: “robot” capital is distinct from traditional capital in its degree of substitutability with human labor; and only capitalists and skilled workers save. We analyze a range of variants that reflect widely different views of how automation may transform the labor market. Our main results are surprisingly robust: automation is good for growth and bad for equality; in the benchmark model real wages fall in the short run and eventually rise, but “eventually” can easily take generations.”

“Figure 3 plots the transition paths [when robots and labor are perfect vs. imperfect substitutes, when all other parameters take their base case bales.] Perfect substitution of robot for human labor delivers perpetual growth. But the rich become richer and the poor poorer with every passing year. In the long run, the real wage decreases 13.4% while capitalists’ income rises without limit.”

From a new IMF working paper by Andrew Berg, Edward Buffie, and Luis-Felipe Zanna:

“Advances in artificial intelligence and robotics may be leading to a new industrial revolution. This paper presents a model with the minimum necessary features to analyze the implications for inequality and output. Two assumptions are key: “robot” capital is distinct from traditional capital in its degree of substitutability with human labor; and only capitalists and skilled workers save.

Posted by at 10:59 AM

Labels: Inclusive Growth

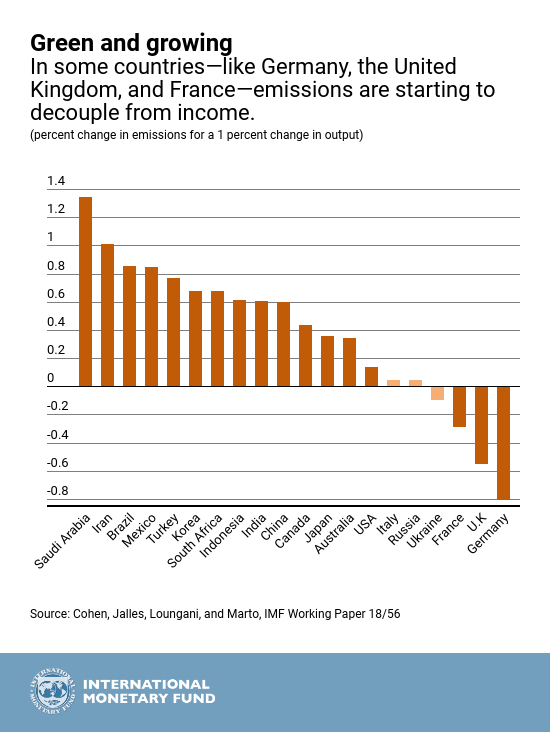

Chart of the Week: Greenery and Prosperity

Economic growth has traditionally moved in tandem with pollution. But can countries break this link and manage to grow while lowering pollution?

Our research, based on joint work with Gail Cohen and Ricardo Marto, shows that yes, progress is being made. Our evidence is clear: advanced economies are starting to show signs of decoupling—increasing growth while reducing pollution—but emerging market economies not yet.

The chart summarizes our evidence on the link between the trend (long-run relationship) in greenhouse gas (GHG) emissions and the trend in incomes. Our analysis covers the world’s top twenty largest GHG emitters from 1990 to the present. Over this time, incomes have grown—the trend is positive—despite dips due to occasional recessions and financial crises. But what has happened to trend emissions?

The bars in the chart show the percent increase in trend emissions for every 1 percent increase in trend incomes—economists refer to such estimates as elasticities. Look first at the three cases on the far right of the chart—Germany, the United Kingdom, and France. For this group the elasticity estimates are negative: emissions have fallen despite the increase in incomes. These countries have achieved decoupling of emissions and output. Our results show that this is due both to active policies by these countries aimed at decarbonizing their economies as well as the structural transformation of their economies towards a greater role for services.

Continue reading here.

Economic growth has traditionally moved in tandem with pollution. But can countries break this link and manage to grow while lowering pollution?

Our research, based on joint work with Gail Cohen and Ricardo Marto, shows that yes, progress is being made. Our evidence is clear: advanced economies are starting to show signs of decoupling—increasing growth while reducing pollution—but emerging market economies not yet.

The chart summarizes our evidence on the link between the trend (long-run relationship) in greenhouse gas (GHG) emissions and the trend in incomes.

Posted by at 10:51 AM

Labels: Energy & Climate Change

Subscribe to: Posts