Thursday, May 3, 2018

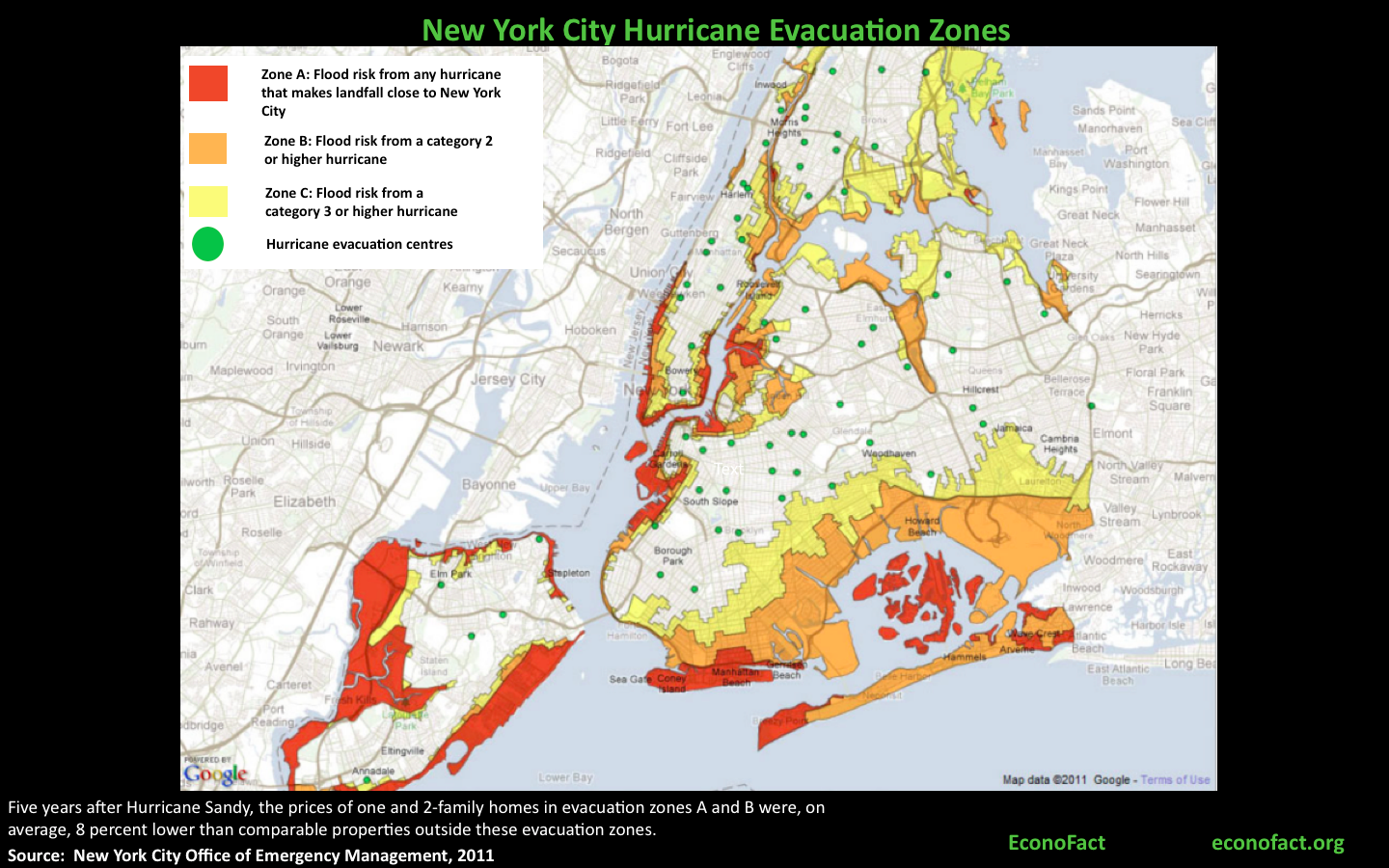

Learning from Hurricane Sandy? Rising Seas and Housing Values in New York

From ECONOFACT:

The Issue:

“The chance of large-scale coastal flooding episodes is increasing. In the last few decades, sea levels have been rising steadily at about 3 centimeters per decade and many estimates expect that this rate will accelerate going forward. At the same time, the population living in coastal counties in the United States grew by 40 percent between 1970 and 2010 and is projected to continue rising. Are people considering the increased risk of flooding associated with sea level rise in their housing decisions? Looking at what happened to property values in New York City after Hurricane Sandy gives us a first look at how those on the front lines may be responding.”

The Facts:

- “Past research has found the response of homebuyers towards flooding risks and the threat of other climate-related hazards to be short-lived. While a region’s exposure to hurricanes or flooding does not vary greatly from one year to the next, many studies have found that homebuyers tend to take these risks much more into account immediately following hurricanes and other catastrophic events. However, these effects tend to be short-lived —very often vanishing completely within five years (see here and here). Flood insurance take-up rates, for instance, have tended to spike the year after a flooding event and then gradually decline to the levels that prevailed before the flood. This response happened not only in the flooded zones but – to a lesser extent — also in non-flooded areas in the same television media markets according to one study. While the risk of flooding remains objectively the same, people may be more aware of it following a flood and then tend to forget about it with the passage of time. It is also possible that, as time goes by, new people who have had less direct exposure to the risk move into the area. These facts suggest a gap between objective probabilities of flood risk and households’ perceptions of this risk. In addition to the psychological biases mentioned, coordination problems, misguided policies, and the expectation of financial assistance by the government in case of disaster might contribute to a mismatch between home prices and damage risk.”

- “Hurricane Sandy was a climatic event of unprecedented proportions that impacted the Greater New York region. The storm hit New York on October 29, 2012. At the time, Sandy was the largest Atlantic hurricane on record and the second costliest in U.S. history (behind Hurricane Katrina), with damages amounting to over $19 billion. Hurricane Sandy flooded 17 percent of New York City (or nearly 90,000 buildings).”

Continue reading here.

From ECONOFACT:

The Issue:

“The chance of large-scale coastal flooding episodes is increasing. In the last few decades, sea levels have been rising steadily at about 3 centimeters per decade and many estimates expect that this rate will accelerate going forward. At the same time, the population living in coastal counties in the United States grew by 40 percent between 1970 and 2010 and is projected to continue rising.

Posted by at 3:31 PM

Labels: Global Housing Watch

Retail Apocalypse Postponed Not Cancelled

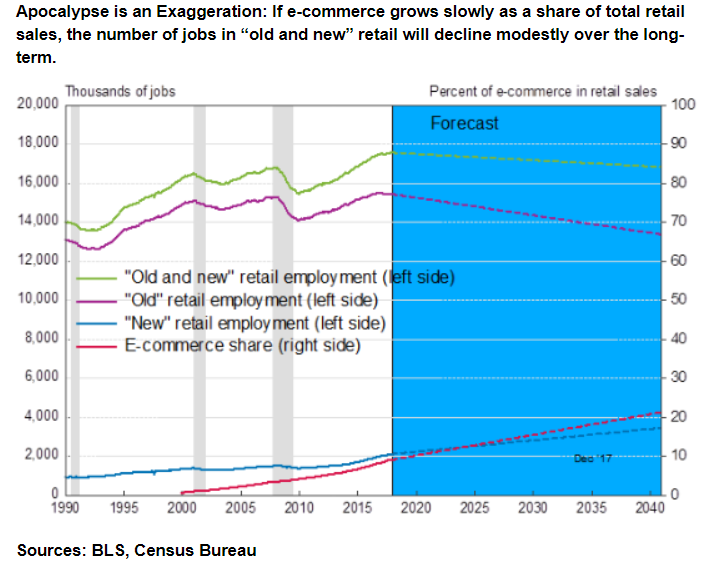

A new post by Brian Schaitkin says that “Economist Michael Mandel of the Progressive Policy Institute tells a reassuring story about what will happen to retail employment. Jobs behind retail counters and stocking store aisles will simply be replaced by jobs at warehouses, e-commerce facilities, and as delivery drivers.” How quickly will this happen? He provides forecasts under the “Apocalypse is an Exaggeration” and “Apocalypse is Ongoing” scenarios:

“[…] Under an “Apocalypse is an Exaggeration” scenario, e-commerce will grow at a modest pace as a share of total retail sales because many of the lowest hanging e-commerce fruit have already been plucked. Therefore, the transformation from in-store retail to e-commerce would take quite a long time. The logistical challenge of shipping books to individual customers is orders of magnitude less complicated than delivering groceries. The “in-store” experience also provides special value to some consumers, especially when the ability to touch and feel merchandise and consult with experts is part of the value proposition stores and their workers provide. Firms will learn how to adapt to the challenge of e-commerce in less easily adapted industries, but because of these challenges, growth in the e-commerce share may increase by only 6.8 percent every 13 years, as happened between 2005 and 2017. Under this scenario, the share of e-commerce in retail sales would be 21 percent by the end of 2040, and the “old and new” retail sector will employ 16.8 million workers, compared to 17.6 million today. A disappointing job trajectory to be sure, but hardly apocalyptic.”

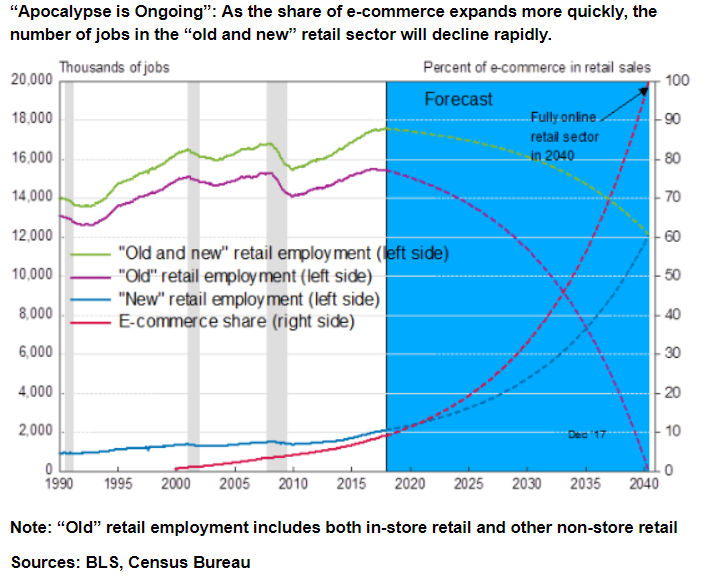

“The 2005 to 2017 period though lights the way to a bolder, yet in my view more likely “Apocalypse is Ongoing” scenario. This scenario assumes that exponential growth of the e-commerce share will continue as it did from 2005 to 2017 meaning that the e-commerce share of retail will double every 6.5 years. Incentives for firms to adapt new sectors to e-commerce will be tremendous due to the convenience and efficiency commerce without stores can provide. Companies can apply the lessons from developing one form of e-commerce to new product areas with knowledge of the pitfalls they are likely to encounter. Under this scenario, e-commerce would represent 18 percent of retail sales by the middle of 2024, 36 percent by the end of 2030, and 100 percent by the middle of 2040. Initially, job losses resulting from the shift to e-commerce would be small in “old and new” retail with 738,000 jobs disappearing between now and the end of 2025. By 2040, however, only 12.1 million workers, all employed by “new” retail sectors, would be able to manage all retail sales activities, a loss of 5.5 million jobs.”

Continue reading here.

A new post by Brian Schaitkin says that “Economist Michael Mandel of the Progressive Policy Institute tells a reassuring story about what will happen to retail employment. Jobs behind retail counters and stocking store aisles will simply be replaced by jobs at warehouses, e-commerce facilities, and as delivery drivers.” How quickly will this happen? He provides forecasts under the “Apocalypse is an Exaggeration” and “Apocalypse is Ongoing” scenarios:

“[…] Under an “Apocalypse is an Exaggeration” scenario,

Posted by at 10:13 AM

Labels: Forecasting Forum, Inclusive Growth

Wednesday, May 2, 2018

Housing Market in Israel

From the IMF’s latest report on Israel:

- On house price developments: “Housing price increases have slowed significantly but supply may also be weakening. After more than doubling since 2008, house price rises slowed to under two percent y/y in 2017, below household income growth. Transactions also declined, with investor activity likely affected by the proposed tax on owners of more than two apartments, and first-time buyers waiting to see the “Buyer’s Price” program impact.5 But residential investment began to decline in mid-2017, and a 16 percent y/y fall in starts in H2’2017 suggests further falls to come.”

- On financial sector and housing policies:

- “Israel’s banking system is healthy. Capitalization, loan quality, and profitability continued to improve in 2017. The leverage ratio rose to 7.5 percent, exceeding that in most advanced economies. All five of the largest banks met the capital requirement, enabling them to resume or raise dividend payouts in 2017.”

- “Household debt remains relatively low, with well-contained risks, and business debt has stabilized after declining significantly. The household debt ratio has been rising for a decade, but remains low at just over 40 percent of GDP. The BoI has maintained strong macroprudential measures in the housing area (…). As a result, new mortgages with LTVs over 75 percent have been almost eliminated, and the share of lower LTV loans has risen. However, consumer credit, which usually has a variable interest rate, is almost two-fifths of total household debt, calling for close monitoring. Business sector debt has declined to below 70 percent of GDP, with the stock of corporate bonds falling to 19 percent of GDP by 2017, 9 percent of GDP less than their former ratio. Limited supply and the global search for yield may be contributing to low spreads on these bonds.”

- “Slowing housing construction despite still high housing prices calls for reforms to make supply more responsive to needs and to improve housing affordability. The authorities estimate that 45–50 thousand new housing units are needed annually during 2015–2020, rising to 60 thousand annually by 2026–35. Completions appear sufficient in 2016–2017, but shortfalls could return given recent falls in housing starts. Hence, continued reform efforts are needed:

- “Land supply, competition, and regulation. Increased land auctions are needed to avoid supply constraints and to help make construction more responsive to variations in demand. Construction costs and time to build should be reduced by streamlining building regulations and expanding foreign construction company access.”

- “Municipal incentives. To encourage timely municipal approval of residential development, residential property taxes should be raised—while avoiding work disincentives—coupled with predictable central government support to municipalities for the up-front costs of additional infrastructure and public services.”

- “Expand commutable areas and increase urban density. Well-developed public transportation can expand commutable areas and relieve demand in major centers, hence plans to establish metropolitan authorities are welcome. Urban renewal should be increased as density in Tel Aviv is relatively low, including through the proposed fast-track approvals of mixed use development.”

From the IMF’s latest report on Israel:

- On house price developments: “Housing price increases have slowed significantly but supply may also be weakening. After more than doubling since 2008, house price rises slowed to under two percent y/y in 2017, below household income growth. Transactions also declined, with investor activity likely affected by the proposed tax on owners of more than two apartments, and first-time buyers waiting to see the “Buyer’s Price” program impact.5 But residential investment began to decline in mid-2017,

Posted by at 10:13 AM

Labels: Global Housing Watch

Tuesday, May 1, 2018

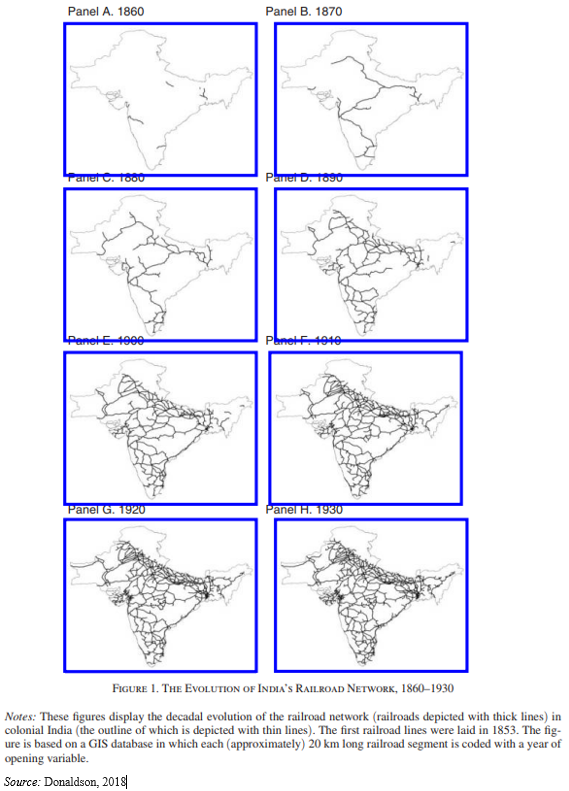

How much does infrastructure boost an economy?

A new post by Peter Dizikes summarizing David Donaldson’s new paper on how railroads helped India trade and grow: “railroads fostered commerce that raised real agricultural income by 16 percent.”

“Donaldson’s paper on the subject, “Railroads of the Raj: Estimating the Impact of Transportation Infrastructure,” just published in the American Economic Review, may also speak to the importance of infrastructure more broadly. After all, as he notes in the paper, about 20 percent of World Bank lending in the developing world goes to infrastructure projects. And in the United States, debate rolls on about the value of building and refurbishing America’s roads, bridges, railroads, ports, and airports.”

“And while every country is different, and circumstances change over time, Donaldson’s research suggests that the growth India experienced as its railroads grew was specifically the result of increased trade, a general finding that could be applied to other countries and other eras.”

A new post by Peter Dizikes summarizing David Donaldson’s new paper on how railroads helped India trade and grow: “railroads fostered commerce that raised real agricultural income by 16 percent.”

“Donaldson’s paper on the subject, “Railroads of the Raj: Estimating the Impact of Transportation Infrastructure,” just published in the American Economic Review, may also speak to the importance of infrastructure more broadly. After all, as he notes in the paper,

Posted by at 11:39 AM

Labels: Inclusive Growth, Macro Demystified

El-Erian on What’s Wrong with Economics

From a new post by Mohamed A. El-Erian:

“[…] the reputation of mainstream economists has taken a beating in the last 10 years. The bulk of them failed to predict the 2008 crisis that almost tipped the global economy into a multiyear depression. They also didn’t foresee the aftermath.

Most made the mistake of treating the crisis as a cyclical shock and forecast a V-type growth snapback. They were prisoners of an excessive mean-reversion mindset: They acknowledged that growth was taking a huge hit due to severe financial dislocations, but they forecast that economic activity would bounce back strongly and inclusively.

Instead, the experience of advanced economies more closely resembled an “L,” in which they got stuck in a “new normal” characterized by a prolonged period of low and insufficiently inclusive growth.

The damage goes well beyond lost output, diminished consumer welfare, widespread economic insecurity and a worsening of the inequality of income, wealth and opportunity. The shortfalls fueled the politics of anger, along with a heightened mistrust of the establishment, institutions and expert opinion.

This, in turn, has diminished the credibility of economics. Meanwhile, many students have complained to me that the mainstream economics they are taught is divorced from real-world relevance. It is only a matter of time before the funding for economic research risks becoming a casualty.

Yet this huge failure has not been the result of ignorance about the limitations of the discipline, nor is it the consequence of a lack of new, disruptive ideas.

Here are some reasons for the erosion of the insights and predictive powers of mainstream economics:

- The proliferation of oversimplifying assumptions, including those that sideline many elements of real-world behaviors and interactions, in an effort to make models seem more “scientific.” This leads to overreliance on excessively abstract estimation techniques and approaches.

- Insufficient consideration of financial linkages and little allowance, if any, for the possibility that financial dislocations can disrupt the economy.

- Poor and grudging adoption of important insights from behavioral science, along with excessive hesitation to develop multidisciplinary approaches.

- An oversimplification of uncertainty and the ways it influences economic interactions.

- Overemphasis of equilibrium conditions and mean reversion, a trend that reduces the understanding of transitions, structural changes and tipping points.”

From a new post by Mohamed A. El-Erian:

“[…] the reputation of mainstream economists has taken a beating in the last 10 years. The bulk of them failed to predict the 2008 crisis that almost tipped the global economy into a multiyear depression. They also didn’t foresee the aftermath.

Most made the mistake of treating the crisis as a cyclical shock and forecast a V-type growth snapback. They were prisoners of an excessive mean-reversion mindset: They acknowledged that growth was taking a huge hit due to severe financial dislocations,

Posted by at 11:38 AM

Labels: Inclusive Growth, Macro Demystified

Subscribe to: Posts