Saturday, January 20, 2018

2018 AEA Annual Meeting’s Papers on Climate Change and Energy

On climate change

- Expect Above Average Temperatures: Identifying the Economic Impacts of Climate Change – Paper

- The Impact of Weather on Local Employment: Using Big Data on Small Places – AEA

- Winter is Coming: The Long-run Effects of Climate Change on Conflict, 1400-1900 – Paper

- Regulating Mismeasured Pollution: Implications of Firm Heterogeneity for Environmental Policy – Paper

- Climate Change and Civil Unrest: Evidence From the El Niño Southern Oscillation – Paper – AEA

- Military Planning in a Context of Complex Systems and Climate Change – AEA

- Who Joined the Pigou Club? A Postmortem Analysis of Washington State’s Carbon Tax Initiative I-732 – Paper

- Decoupling Agricultural and Malarial Channels of Climate-driven Infant Mortality in Sub-Saharan Africa – AEA

- How Large is the Potential Economic Benefit of Agricultural Adaptation to Climate Change? – Paper and Presentation

- Firm and Household Responses to Climate Change Risks – AEA

- ACE – Analytic Climate Economy (with Temperature and Uncertainty) – Paper

- Expect Above Average Temperatures: Identifying the Economic Impacts of Climate Change – Paper

- Same Storm, Different Disasters: Consumer Credit Access, Income Inequality, and Natural Disaster Recovery – Paper

- Heterogeneous firms under regional temperature shocks: exit and reallocation, with evidence from Indonesia – Paper

- The Costs of Inefficient Regulation: Evidence from the Bakken – Paper

- Clean Energy Investments for New York State: An Economic Framework for Promoting Climate Stabilization and Expanding Good Job Opportunities – AEA

- Spatial Effects of Nitrogen Pollution on Drinking Water Production – Paper

- Regulating Mismeasured Pollution: Implications of Firm Heterogeneity for Environmental Policy – Paper

- Assessing the External Net Benefits of Wind Energy: The Case of Iowa’s Wind Farms – Paper

- Do HOV Lanes Save Energy? Evidence from a General Equilibrium Model of the City – Paper

On oil market

- Informing SPR Drawdown Policy through Oil Futures and Inventory Dynamics – Paper

- Measuring Leakage Risk – AEA

- How Trade-sensitive are Energy-intensive Sectors? – AEA

- Gasoline Savings From Clean Vehicle Adoption – Paper

- Response of Consumer Debt to Income Shocks: The Case of Energy Booms and Busts – Paper and Presentations

- Granger Causality of Real Oil Prices After the Great Recession – Paper and Presentation

- Did the Renewable Fuel Standard Shift Market Expectations of the Price of Ethanol? – Paper

- Evaluating a Discretionary Safety Valve: The Economic and Environmental Impacts of Waiving Fuel Content Regulations in Response to Supply Shocks – Paper

On shale gas

- Local Economic Shocks and Entrepreneurship: New Business Formation During the Shale Oil and Gas Boom – Paper

- Collateral Damage: The Impact of Shale Gas on Mortgage Lending – Paper

- The Local Effects of the Texas Shale Boom on Schools, Students, and Teachers – Paper

- Analyzing the Risk of Transporting Crude Oil by Rail – Paper

- Local Labor Market Shocks and Wage Differentials: Evidence From Shale Oil and Gas Booms – Paper

On carbon market

- Lessons From China’s Seven Regional Carbon Market Pilots – AEA

- China’s Rate-Based Approach to Reducing CO2 Emissions: Strengths, Limitations, and Alternatives – Paper

- Design Issues in China’s National Carbon Market – Paper

- Who Joined the Pigou Club? A Postmortem Analysis of Washington State’s Carbon Tax Initiative I-732 – Paper

- Do Carbon Taxes Kill Jobs? New Heterogeneous Evidence from British Columbia – Paper

- Emissions Containment in Response to Carbon Market Prices – Paper and Presentation

- Pigou Creates Losers: On the Impossibility of Pareto Improvements From Pigouvian Taxes – AEA

On solar energy

- Pass-Through as a Test for Market Power: An Application to Solar Subsidies – Paper

- What Drives Social Contagion in the Adoption of Solar Photovoltaic Technology? – Paper

- What Drives Social Contagion in the Adoption of Solar Photovoltaic Technology? – Paper

- Siting Solar PV Capacity to Maximize Environmental Benefits – Paper

On electricity

- What’s killing nuclear power in U.S. electricity markets? Drivers of wholesale price declines at nuclear generators in the PJM Interconnection – Paper and Presentation

- Who Pays In Deregulated Electricity Markets? – Paper

- Determinants of the Cost of Electricity Supply in India – AEA

On vehicle market

- Self-Driving Cars and the City: Long-Run Effects on Land Use, Welfare, and the Environment – Paper

- Attribute Substitution in Household Vehicle Portfolios – Paper

- Mind the Gap! Tax Incentives and Incentives for Manipulating Fuel Efficiency in the Automobile Industry – AEA

- Does an Energy Efficiency Gap Exist in the Light-duty Vehicle Market? Evidence From Fuel-saving Technology Adoption – Paper

On climate change

- Expect Above Average Temperatures: Identifying the Economic Impacts of Climate Change – Paper

- The Impact of Weather on Local Employment: Using Big Data on Small Places – AEA

- Winter is Coming: The Long-run Effects of Climate Change on Conflict, 1400-1900 – Paper

- Regulating Mismeasured Pollution: Implications of Firm Heterogeneity for Environmental Policy – Paper

- Climate Change and Civil Unrest: Evidence From the El Niño Southern Oscillation – Paper – AEA

- Military Planning in a Context of Complex Systems and Climate Change – AEA

- Who Joined the Pigou Club?

Posted by at 7:19 PM

Labels: Energy & Climate Change

Friday, January 19, 2018

Housing View – January 19, 2018

On cross-country:

- Comparative Analysis of Newly-Built Housing Quality in Poland and Lithuania – De Gruyter

On the US:

- The Hazards of Concentrating Wealth in Homeownership – Federal Reserve Bank of St. Louis

- A Bad Start on Reforming Fannie and Freddie – Bloomberg

- The Corrupt Politics of Low-Income Housing – Reason

- Fannie Mae will ease financial standards for mortgage applicants next month – Washington Post

- How the latest affordable housing policy benefits homeowners and realtors, not first-time buyers – American Enterprise Institute

- The Great Urban Housing Solution That Has No Good Name – The Atlantic

- Remodeling Market to March Higher in 2018 – Harvard Joint Center for Housing Studies

On other countries:

- [China] Housing market sentiment and intervention effectiveness: Evidence from China – Emerging Markets Review

- [China] Is there a housing bubble in China? – Sun Yat-sen University, Guangzhou

- [China] China’s Hot Housing Market Begins to Cool – Wall Street Journal

- [Czech Republic] Who actually decides? Parental influence on the housing tenure choice of their children – The Czech Academy of Sciences

- [Iceland] Discrimination in the Housing Market as an Impediment to European Labour Force Integration: The Case of Iceland – Lund University

- [India] India’s property slowdown puts developers in crosshairs – Financial Times

- [Italy] Matching and Credit Conditions: Evidence from the Italian Housing Market Survey – Luiss Lab of European Economics

- [Singapore] Curb Your Enthusiasm for Singapore Property – Bloomberg

- [United Kingdom] Why Britain’s buy-to-let boom is over – Economist

- [United Kingdom] Housing in London: Addressing the Supply Crisis – London School of Economics

- [United Kingdom] What will happen to house prices in 2018? – Financial Times

- [United Kingdom] Divorce, Separation, and Housing Changes: A Multiprocess Analysis of Longitudinal Data from England and Wales – Demography

Photo by Aliis Sinisalu

On cross-country:

- Comparative Analysis of Newly-Built Housing Quality in Poland and Lithuania – De Gruyter

On the US:

- The Hazards of Concentrating Wealth in Homeownership – Federal Reserve Bank of St. Louis

- A Bad Start on Reforming Fannie and Freddie – Bloomberg

- The Corrupt Politics of Low-Income Housing – Reason

- Fannie Mae will ease financial standards for mortgage applicants next month – Washington Post

- How the latest affordable housing policy benefits homeowners and realtors,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, January 18, 2018

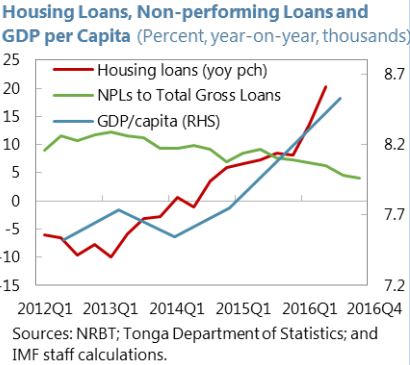

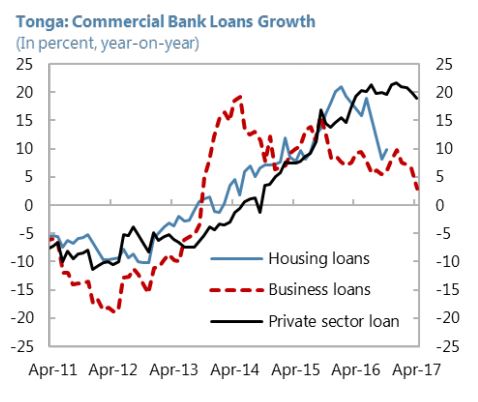

Tonga’s Housing Sector

From the IMF’s latest report on Tonga:

“Housing credit continues to rise supported by lower interest rates and economic growth. A housing bubble is unlikely to develop. Tonga has a rigid land tenure system with lengthy land registration. The secondary market for housing is very small and slow, with approximately 10 house sale transactions per each year. Most bank credit finances construction of owner-occupied dwellings and housing for personal use rather than for investment. The lending to households is collateralized, where land is the only asset that is qualified as collateral by banks. The limited time of land use depreciates its value as collateral over time.

Housing credit continues to rise supported by (i) low lending rates for housing loans; (ii) revision of the Land Act; and (iii) other initiatives. Higher payments for import of construction materials driven partially by removal of custom duty on construction materials also contributed to the increase of housing credit.

The household credit quality is not a clear concern. Although housing credit is growing rapidly, there are no signs of weakening ability of households to service the debt. All loans are salary-based, where loan payments are deducted directly from the salaries. The remittances continue to increase, and consumer confidence and demand are also on the rise. On the supply side, the ratio NPLs continue to decline. In FY2017, the value of collateral held against the delinquent loans reported by banks was at T$40.5 million compared to total NPLs of T$16.9 million, which indicates that banks hold sufficient collateral to cover any shortfall in loan-loss provisions.”

From the IMF’s latest report on Tonga:

“Housing credit continues to rise supported by lower interest rates and economic growth. A housing bubble is unlikely to develop. Tonga has a rigid land tenure system with lengthy land registration. The secondary market for housing is very small and slow, with approximately 10 house sale transactions per each year. Most bank credit finances construction of owner-occupied dwellings and housing for personal use rather than for investment.

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, January 15, 2018

Regulatory Cycles: Revisiting the Political Economy of Financial Crises

From a new IMF working paper by Jihad Dagher:

“This paper reviews some of the most infamous financial crisis in history and brings several patterns that are rarely discussed in the literature, at least not in a historical and cross- sectional approach. It shows that in most cases regulation has been pro-cyclical, effectively weakening during the boom and strengthening during the bust. Regulators do not operate in a vacuum, and this paper shows how, in most cases, political interventions have helped fuel the boom in similar ways across time and countries. The political repercussions of crises, partly due to changes in the public’s perception about the role of the government, are usually very significant. They help explain the reversal of policies and the regulatory backlash.

The interplay between politics and financial policy, described in this paper, has not received sufficient attention. The focus of the literature, which has been mostly cast in technical terms, is to find the optimal level of regulation that regulators should be enforc- ing. Will new regulations and their enforcement survive the test of time? History offers a relatively pessimistic answer to this question. It offers plenty of examples where regulatory failures can be attributed to political failures. Strengthened regulations and supervision are, in essence, tools given to regulators to use as long as the political climate allows them to. To what extent can regulators be insulated from changes in politicians’ (and voters’) philosophy toward regulation? What changes need to be made at the institutional level? This is an important question left for future research. Acknowledging the fact that politics can be the undoing of macro-prudential policy would be a step in the right direction.”

From a new IMF working paper by Jihad Dagher:

“This paper reviews some of the most infamous financial crisis in history and brings several patterns that are rarely discussed in the literature, at least not in a historical and cross- sectional approach. It shows that in most cases regulation has been pro-cyclical, effectively weakening during the boom and strengthening during the bust. Regulators do not operate in a vacuum, and this paper shows how,

Posted by at 2:35 PM

Labels: Macro Demystified

2018 AEA Annual Meeting’s Papers on Inequality

On income inequality

- Top Income Inequality in the 21st Century: Some Cautionary Notes – AEA

- Capitalists in the Twenty-first Century – Paper

- Long Run Developments of Income and Wealth Inequality: Do They Move Together? – AEA

- Has Middle Class Wealth Recovered? – Paper

- Income and Wealth Inequality in America, 1949-2013 – Paper

- Recent Trends in the Variability of Men’s Earnings: Evidence From Administrative and Survey Data – Paper

- Taxes, Regulations of Businesses and Evolution of Income Inequality in the United States – Paper

- Origins of Wealth Inequality – AEA

- An Empirical Institutionalist Analysis of the Determinants of Income and Wealth Inequality in USA Since the 1980s – Paper

- Road to Despair and the Geography of the America Left Behind – AEA

On gender inequality

- Top Income Inequality and the Gender Pay Gap – Paper and Presentation

- Choosing Between Career and Family – Gender Roles as a Coordination Device in a Specialization Game – AEA

- Gender Inequality in Post-capitalism: Theorizing Institutions for Democratic Workplaces – Paper

On racial inequality

- Examining the Black-White Earnings Differential with Administrative Records – Paper

- Occupational Licensing Reduces Racial and Gender Wage Gaps: Evidence From the Survey of Income and Program Participation – AEA

- Higher Education in Orthodox, Heterodox, and Stratification Economics Perspectives on Racial Economic Inequality – AEA

- Poverty and Inequality – AEA

- Inequality Between and Within Immigrant Groups in the United States – Paper

- Revising The Racial Wage Gap Among Men: The Role Of Non-employment And Incarceration – AEA

- Revisiting Bergmann’s Occupational Crowding Model – AEA

- Racial Differences in Labor Force Participation Since the Great Recession: What’s Happening? – Paper

- The Color of Wealth: Evidence Across United States Cities – AEA

- No End in Sight? The Widening Racial Wealth Gap Since The Great Recession – AEA

On populism and globalization

- Understanding the Rise of Populism: Financialisation, Household Balance Sheet Structures, and Inequality in the United States Since 1980s – Paper

- Trade and Inequality: Evidence From Worker-level Adjustment in France – AEA

- Trade, Jobs, and Inequality – AEA

- Globalization and Inequality in Innovation: A Perspective from U.S. R&D Tax Credit Policy – Paper

- Making Financial Globalization More Inclusive – Paper and Presentation

- Making Globalization More Inclusive: When Compensation Is Not Enough – Paper

On labor

- Earnings Inequality and Mobility Trends in the United States: Nationally Representative Estimates from Longitudinally Linked Employer-employee Data – Paper and Presentation

- Theories of Redistribution and Share of Labor Income – Paper

- Labor Unions and Wealth Inequality – AEA

- The Care Penalty and the Power Premium: Earnings Inequality in the United States – AEA

- Inequality, Good Governance and Endemic Corruption – Paper

- Inequality and the Disappearing Large Firm Pay Premium – Paper

- Earnings Inequality and the Minimum Wage: Evidence From Brazil – Paper

- Unequal Growth in Local Wages: Rail Versus Internet Infrastructure – Paper

- Determinants of the Wage Share: Evidence From Firm-level Data – Presentation

- Declining Labor and Capital Shares – Paper

- Labor Share and Technology Dynamics – Paper

- Theories of Redistribution and Share of Labor Income – Paper

- Earnings Inequality and the Role of the Firm – Paper and Presentation

- Inequality in Retirement Wealth – Paper and Presentation

- Delayed Retirement and the Growth in Economic Inequality by Work Ability – Paper

- Robots, Growth and Inequality: Should We Fear the Robot Revolution? – Paper and Presentation

- Endogenous Skill Choice as Source of Productivity Dispersion – Presentation

- The Fall of the Labor Share and the Rise of Superstar Firms – Paper

On Africa

- Inclusive Finance for SMEs in South Africa and Its Impact on Growth and Inequality – Paper

- Institutions, Structures and Policy Paradigms: Toward Understanding Inequality in Africa – AEA

On other issues

- Extreme Inequality: Evidence From Brazil, India, the Middle-East, and South Africa – Paper and Presentation

- When Inequality Matters for Macro and Macro Matters for Inequality – Paper

- Estimating Unequal Gains Across United States Consumers With Supplier Trade Data – Paper and Presentation

- Why Does Portfolio Choice Correlate Across Generations? – Paper

- Ten Years after the Crisis: A Lost Decade? – Paper

- Military Expenditures And Income Inequality, Evidence From A Panel Of Transition Countries (1990-2015) – AEA

- Tax Rates and Progressivity: Was the System More Progressive when the Top Rate was 91 Percent? – Paper and Presentation

- Rising Inequality, Household Debt, And The Slow Recovery After Great Recession – AEA

- Consumption Inequality and The Frequency of Purchases – Paper

- Mergers and Acquisitions, Technological Change and Inequality – Paper

- Same Storm, Different Disasters: Consumer Credit Access, Income Inequality, and Natural Disaster Recovery – Paper

- Rethinking Inequality in 21st Century – Financial Sector, Household Balance Sheet Structures and Distribution in the United States Since 1980s – Paper

- The Effects of Technical Change: Does Capital Aggregation Matter? – AEA

On income inequality

- Top Income Inequality in the 21st Century: Some Cautionary Notes – AEA

- Capitalists in the Twenty-first Century – Paper

- Long Run Developments of Income and Wealth Inequality: Do They Move Together? – AEA

- Has Middle Class Wealth Recovered? – Paper

- Income and Wealth Inequality in America, 1949-2013 – Paper

- Recent Trends in the Variability of Men’s Earnings: Evidence From Administrative and Survey Data – Paper

- Taxes,

Posted by at 1:33 PM

Labels: Inclusive Growth

Subscribe to: Posts