Friday, December 22, 2017

Housing View – December 22, 2017

On cross-country:

- Institutional settings and urban sprawl: evidence from Europe – Journal of Housing Economics

- Bubbles and crashes: A vicious cycle of self- fulfilling investor sentiment – London School of Economics

- Houses, up and down: An international comparison of house price movement – Federal Reserve Bank of St. Louis

- Integrating national policies to deliver compact, connected cities: an overview of transport and housing – Coalition for Urban Transitions

- Space matters: Understanding the real effects of macroeconomic variations in cross-country housing price movements – Economic Letters

- The Crisis in Affordable Housing Is a Problem for Cities Everywhere – World Resources Institute

On the US:

- The Long View of Housing Wealth Effects – Columbia University

- Why Housing Supply Matters – Oregon Office of Economic Analysis

- Reactions to the tax plan: Curbed, New York Times, Reuters, Seattle Times, Seeking Alpha

- Owned Now Rented Later? Housing Stock Transitions and Market Dynamics – Syracuse University

- BuildZoom Research: A Year in Review – BuildZoom

- Measuring population estimates of housing insecurity in the United States: A comprehensive approach – Equitable Growth

- What “affordable housing” really means – Vox

- What Would it Take to Make Neighborhoods More Equitable and Integrated? – Harvard Joint Center for Housing Studies

- The Libertarian: How Housing Got So Expensive – Hoover Institution

- A Decline in Multifamily Housing Permits Offsets a Gain in Single-Family Permits – American Institute for Economic Research

- The Best Housing Market in a Decade, Now What? – Freddie Mac

On other countries:

- [Australia] Does Population Growth Cause Rising Dwelling Prices? – LF Economics

- [Canada] Non-residents focus on new condos in Vancouver, Toronto – Reuters

- [China] Smaller cities drive China’s new home prices in Nov, defying curbs – Reuters

- [Czech Republic] Czech central bank acts to cool buoyant property market – Financial Times

- [Germany] Germany a hot destination for overseas buyers – Global Property Guide

- [Peru] Rapid Rural-to-Urban Migration to Lima: A Need for a Sustainable Housing Reform – Lehigh University

- [Spain] A Decade After Bubble, Spanish Real Estate a Hot Buy Again – Bloomberg

- [United Arab Emirates] Mortgages: Catch me if you can – Reidin

- [United Arab Emirates] Dubai / Abu Dhabi Residential Property Price Indices: November 2017 Results – Reidin

- [United Kingdom] Is owning a house cheaper than renting it? – Medium

Photo by Aliis Sinisalu

On cross-country:

- Institutional settings and urban sprawl: evidence from Europe – Journal of Housing Economics

- Bubbles and crashes: A vicious cycle of self- fulfilling investor sentiment – London School of Economics

- Houses, up and down: An international comparison of house price movement – Federal Reserve Bank of St. Louis

- Integrating national policies to deliver compact, connected cities: an overview of transport and housing – Coalition for Urban Transitions

- Space matters: Understanding the real effects of macroeconomic variations in cross-country housing price movements – Economic Letters

- The Crisis in Affordable Housing Is a Problem for Cities Everywhere – World Resources Institute

Posted by at 5:00 AM

Labels: Global Housing Watch

Sunday, December 17, 2017

House Prices in Cyprus

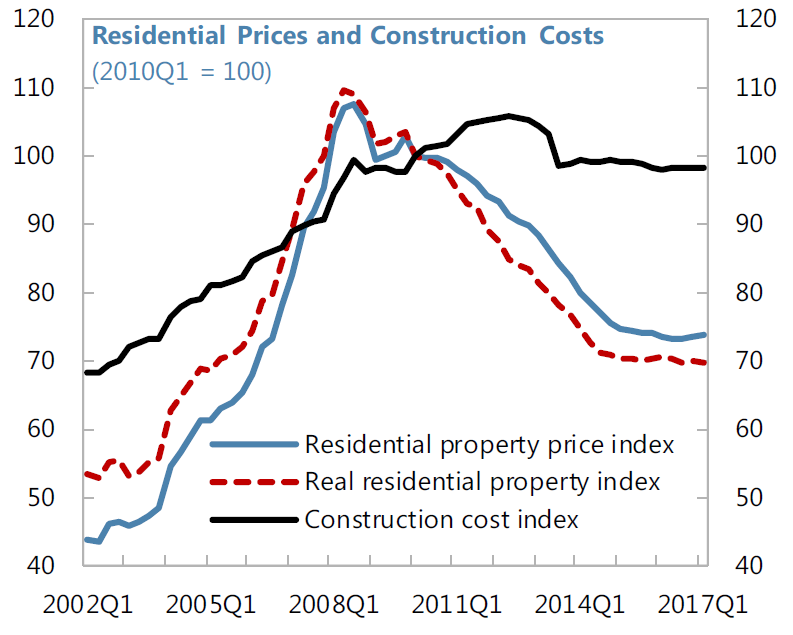

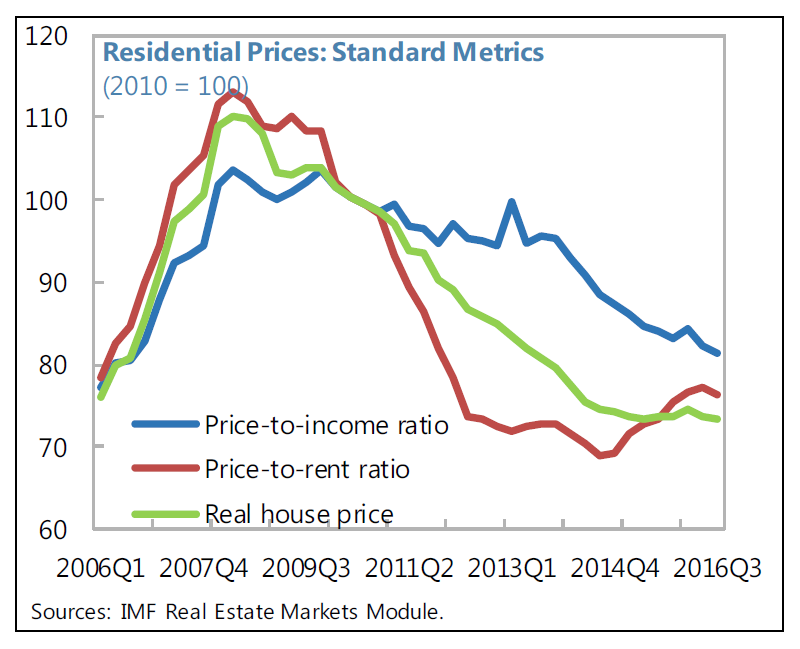

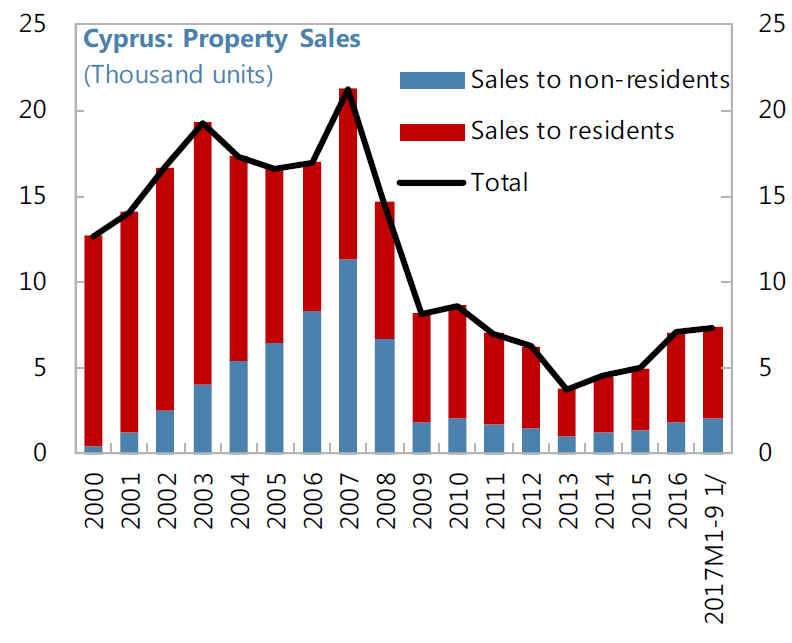

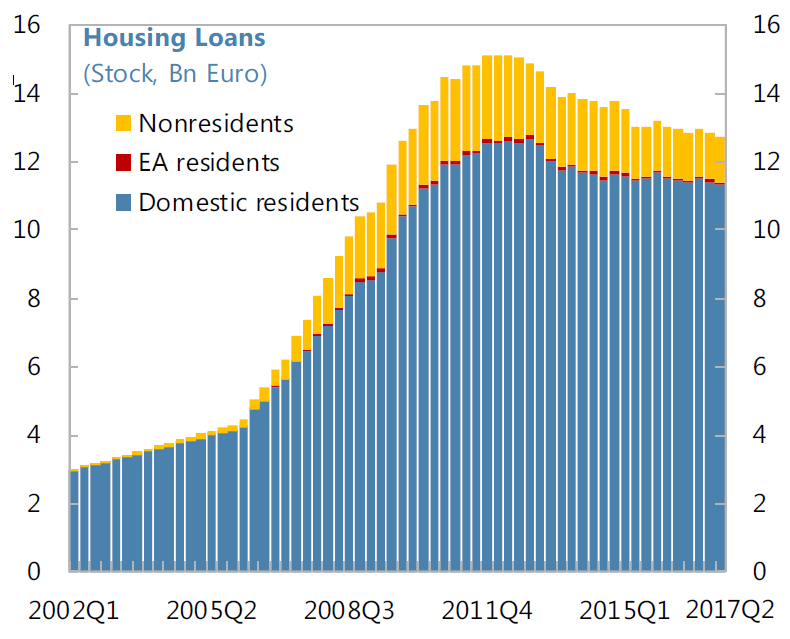

The IMF’s latest report on Cyprus says that:

“After falling sharply, property prices are now rising marginally while transactions are recovering, especially in the luxury segment. Prices declined 30 percent (residential) and 50 percent (retail) relative to the 2008–09 peak, stabilized in 2015, and rose moderately since mid-2016. Price-to-rent and price-to-income ratios have returned to historical levels.6 With at least two thirds of loans collateralized with real estate, moderate price growth will increase banks’ NPL cover and borrowers’ net worth. However, prices have also benefited from the limited number of foreclosures, while turnover is more active in the luxury market owing in part to the CbI scheme.

Increased construction activity has supported the recovery, and associated risks appear manageable. Tax and other incentives targeting the property sector helped to stabilize prices and bring jobs and economic growth. The fact that large luxury construction projects are mainly foreign financed or financed through pre-selling helps to limit financial stability risks. The CbI scheme is a general investment scheme, although real estate is the major beneficiary. Regulatory improvements to the CbI—with stricter controls on intermediaries (including real estate agents and lawyers)—are being considered, but there are no plans to amend the eligibility criteria. Some construction projects will generate future revenue streams (e.g., the casino and marinas) that will underpin their value. However, resale prices of residential units could be affected if too many are built, which could spread to prices of other properties. While developers have not relied on domestic bank financing so far, caution is needed to prevent a recurrence of such bank exposure, and tightening of lending standards is warranted for developers and in the event foreign demand spills over to the housing market for the general population. To comply with EU requirements, VAT will be imposed on transactions of buildable land, thereby partly offsetting—from a tax-incidence perspective—the previous elimination of the IPT and reduction in property transfer fees.”

The IMF’s latest report on Cyprus says that:

“After falling sharply, property prices are now rising marginally while transactions are recovering, especially in the luxury segment. Prices declined 30 percent (residential) and 50 percent (retail) relative to the 2008–09 peak, stabilized in 2015, and rose moderately since mid-2016. Price-to-rent and price-to-income ratios have returned to historical levels.6 With at least two thirds of loans collateralized with real estate, moderate price growth will increase banks’ NPL cover and borrowers’ net worth.

Posted by at 5:01 PM

Labels: Global Housing Watch

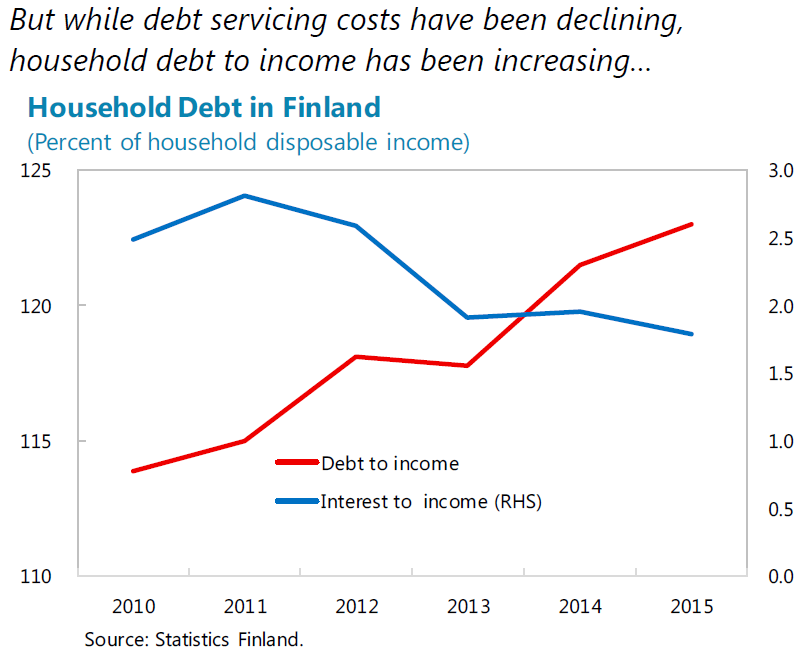

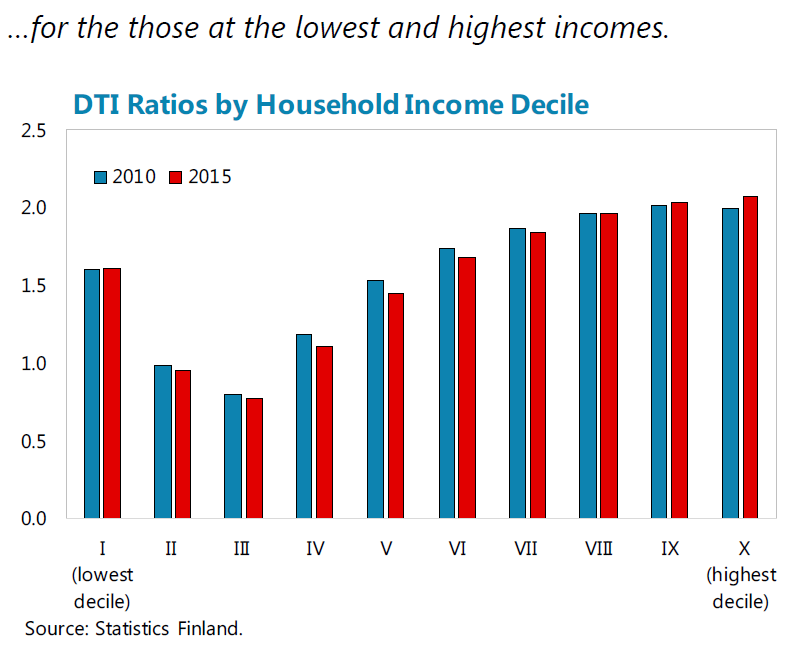

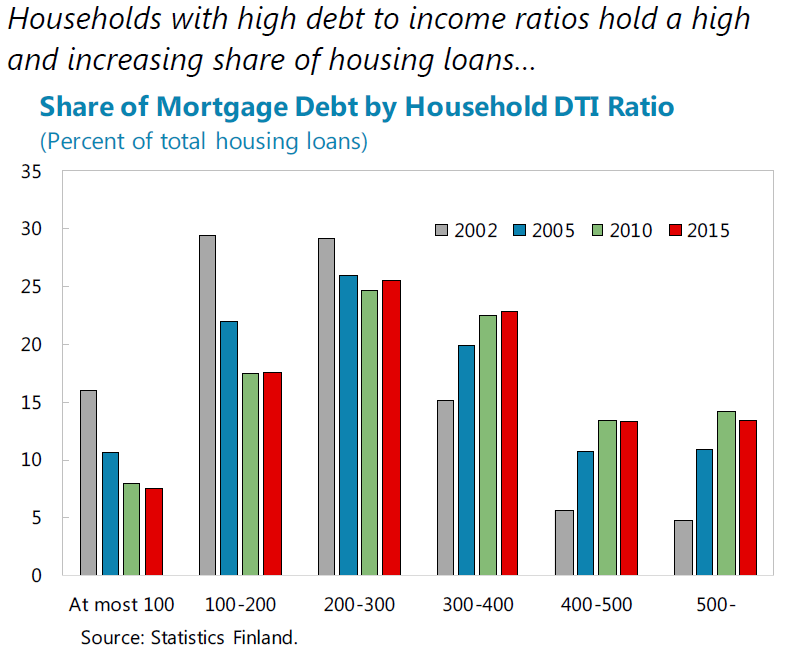

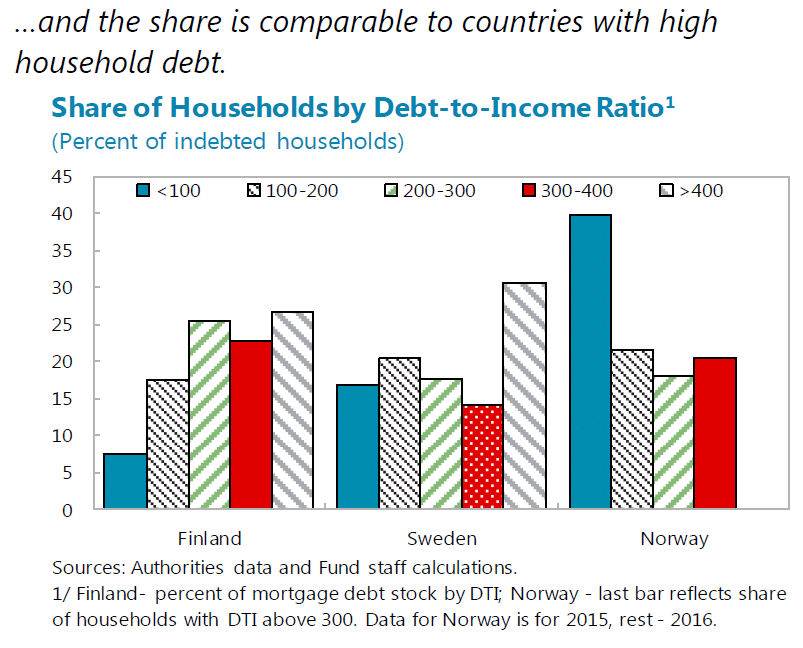

Housing Market in Finland

The IMF’s latest report on Finland says that:

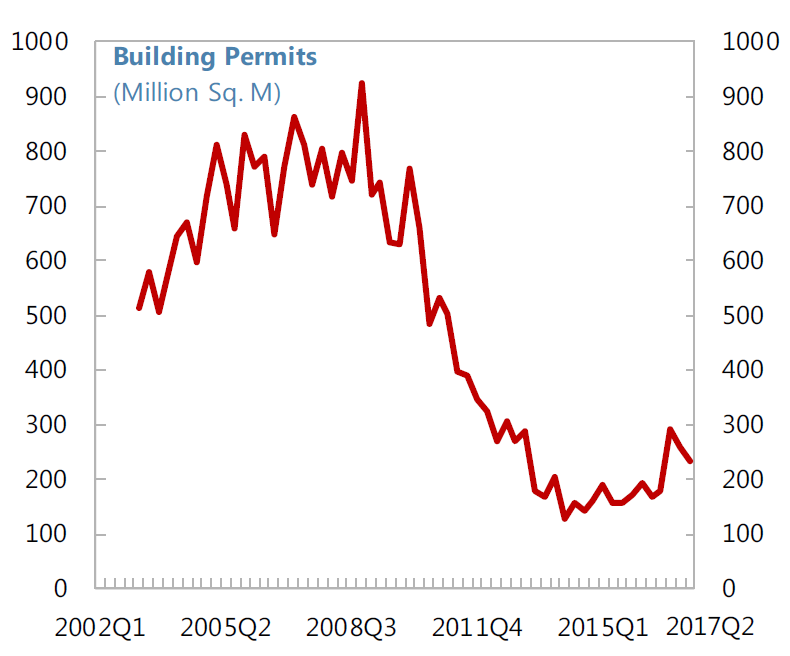

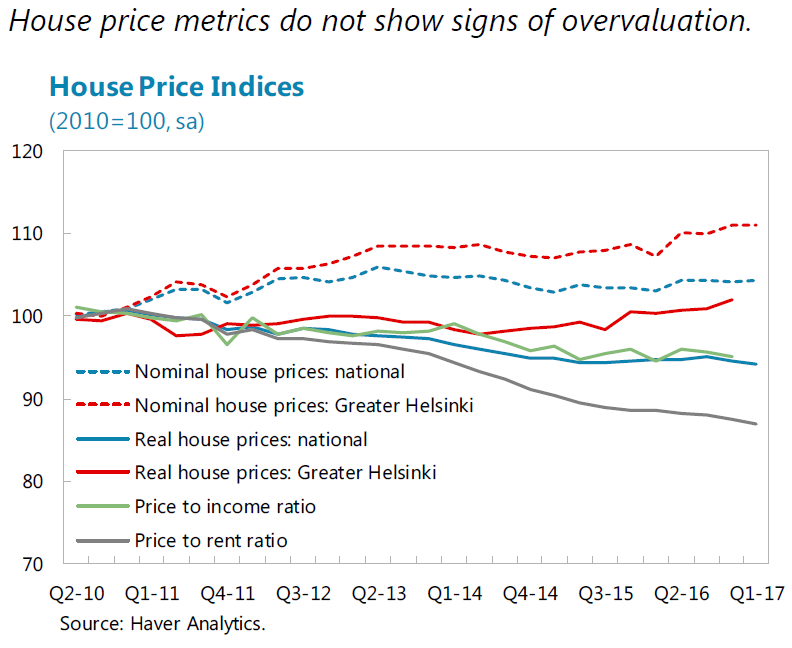

“House prices do not show signs of overvaluation. House prices relative to rent and incomes are close to their long run averages. Real house prices in the Helsinki metropolitan area have increased gradually since 2012, reflecting greater demand, whereas they have declined for the rest of Finland.

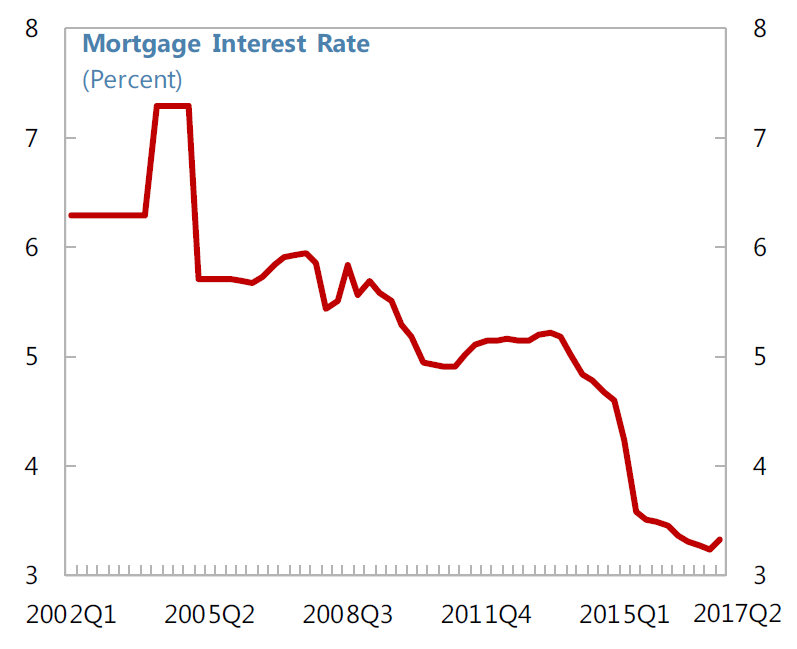

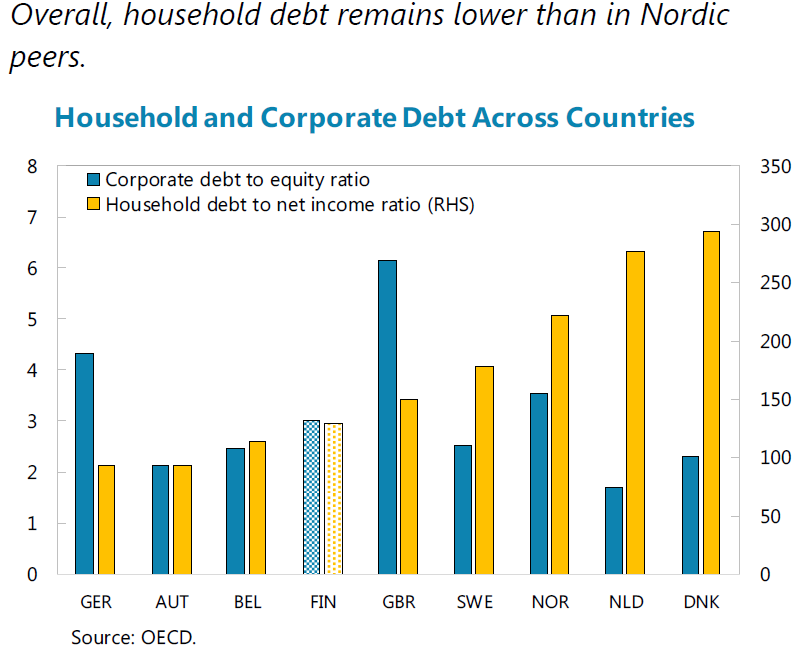

Some households are vulnerable (…). Household saving rates are negative, unsecured consumer credit is growing strongly, and a large share of mortgage loans is held by highly indebted borrowers: over a quarter of mortgage debt is to mortgagees with debt to income ratios higher than 400 percent. Some households would therefore be vulnerable to interest rate increases, as most mortgages are variable rate loans (although about 40 percent of mortgages have contracts that lengthening loan maturity instead of increasing payments).

Increasing imbalances in the household sector make it important to give the FIN-FSA additional tools:

Additional macroprudential measures for borrowers should be introduced to allow the macroprudential authority to better target household vulnerabilities that are not well covered by existing Loan-To-Collateral limits. These could include caps on loans in relation to values of houses and personal incomes, and debt servicing to income. The Bank of Finland and FIN-FSA are currently working together to analyze appropriateness of different tools, and plans to propose legislation for additional measures once the SRB is introduced.

A comprehensive credit registry would be particularly helpful to monitor and assess household credit. The Ministry of Justice has ordered a study on its implementation in Finland.”

The IMF’s latest report on Finland says that:

“House prices do not show signs of overvaluation. House prices relative to rent and incomes are close to their long run averages. Real house prices in the Helsinki metropolitan area have increased gradually since 2012, reflecting greater demand, whereas they have declined for the rest of Finland.

Some households are vulnerable (…). Household saving rates are negative, unsecured consumer credit is growing strongly,

Posted by at 4:33 PM

Labels: Global Housing Watch

Friday, December 15, 2017

The Impact of Fiscal Consolidations on Growth in Sub-Saharan Africa

From the latest IMF working paper:

“This paper examines the output effects of changes in public expenditure and revenue in sub-Saharan African countries during 1990–2016. Fiscal multipliers in sub-Saharan Africa are somewhat smaller than those in advanced and emerging economies. The effect of changes in fiscal policy on output depends on the composition: cutting public investment has a larger effect on output than cutting public consumption or raising revenue. Episodes of fiscal consolidation have short- and medium-term output effects, but here, too, composition matters: fiscal consolidations based on reducing public investment have the largest effect on output, while fiscal consolidations based on revenue mobilization are less harmful than those based on public investment cuts. These findings suggest that the negative impact on growth can be mitigated through the design of fiscal adjustment and the accompanying policy environment.”

From the latest IMF working paper:

“This paper examines the output effects of changes in public expenditure and revenue in sub-Saharan African countries during 1990–2016. Fiscal multipliers in sub-Saharan Africa are somewhat smaller than those in advanced and emerging economies. The effect of changes in fiscal policy on output depends on the composition: cutting public investment has a larger effect on output than cutting public consumption or raising revenue. Episodes of fiscal consolidation have short- and medium-term output effects,

Posted by at 10:29 PM

Labels: Inclusive Growth

Housing View – December 15, 2017

On cross-country:

- Conference on Urban Development and Economics in Developing World – Asian Development Bank

- Data needs and Statistics compilation for macroprudential analysis – Bank for International Settlements

- The Future of Global Real Estate – Savills

On the US:

- The Inflow of New Bay Area Residents Has Grown More Financially Selective, While the Outflow Has Spread to Higher Income Levels – BuildZoom

- Reactions to the tax plan – Bloomberg, Curbed, NPR, NYU Furman Center, Politico, Reason, Washington Post

- Snapshots of the US Housing Market: Ten Years Later – Conversable Economist

- Mortgage-Default Research and the Recent Foreclosure Crisis – Federal Reserve Bank of Boston

- Cities turn to ‘missing middle’ housing to keep older millennials from leaving – Washington Post

- How Affordable Urban Housing Stays Affordable – Bloomberg

- House hunting: State-by-state differences in house price appreciation – Federal Reserve Bank of St. Louis

- How Will a Turbulent 2017 Affect Housing in 2018? – Trulia

- Housing Wealth Fluctuations Affect Seniors’ Health Care Choices – NBER

- New Report: Surge in the Supply of Higher-Cost Rental Housing is Slowing Amidst Persistent Affordability Challenges for Working-Class Households – Harvard Joint Center for Housing Studies

- House prices in Chicago suburbs fall as crime rate rises – Financial Times

On other countries:

- [Australia] Housing Accessibility for First Home Buyers – Reserve Bank of Australia

- [Australia] Chinese capital controls send tremor through Australian property – Reuters

- [Australia] Australian housing markets hurt by Chinese capital outflow restrictions – Global Property Guide

- [Australia] ‘Share of foreign ownership in Australian housing market not significant enough to raise concerns’ – Global Property Guide

- [Australia] Construction boom poses risk to housing markets in Australia – Global Property Guide

- [Canada] Three Things Keeping Me Awake at Night – Bank of Canada

- [Canada] Shadow Lending Growing as Canadians Chase Housing Dream – Bloomberg

- [Canada] Jennifer Keesmaat: It’s time to rethink Canada’s housing system – Maclean’s

- [Canada] Is Canada One Step Closer to Declaring Housing a Human Right? – Citylab

- [China] Beijing housing demolitions spark rare street protests – Financial Times

- [Germany] Unemployment Benefit Recipients: Causes, Reactions and Consequences of Housing Relocations – SpringerLink

- [Germany] The Americans are coming to Germany – Global Property Guide

- [Greece] Why real estate prices in Greece are set to rise? – Global Property Guide

- [Ireland] Housing Supply Coordination Task Force for Dublin – Department of Housing, Planning and Local Government

- [Netherlands] Brexit Refugees Heading to Amsterdam Raise Local Housing Concern – Bloomberg

- [New Zealand] New Zealand looks to ban foreigners from buying houses – Financial Times

- [Singapore] Singapore land supply for private housing in H1 2018 almost steady – Reuters

- [Sweden] Amortization Requirements Benefit Well-Off and Hurt Liquidity-Constrained Housing Buyers – Lars E.O. Svensson

- [United Kingdom] Britain’s buy-to-let boom is coming to an end – Economist

- [United Arab Emirates] Abu Dhabi, Property Market Outlook, Winter 2017 – Cluttons

Photo by Aliis Sinisalu

On cross-country:

- Conference on Urban Development and Economics in Developing World – Asian Development Bank

- Data needs and Statistics compilation for macroprudential analysis – Bank for International Settlements

- The Future of Global Real Estate – Savills

On the US:

Posted by at 9:06 AM

Labels: Global Housing Watch

Subscribe to: Posts