Thursday, June 1, 2017

Colombia’s Housing Market

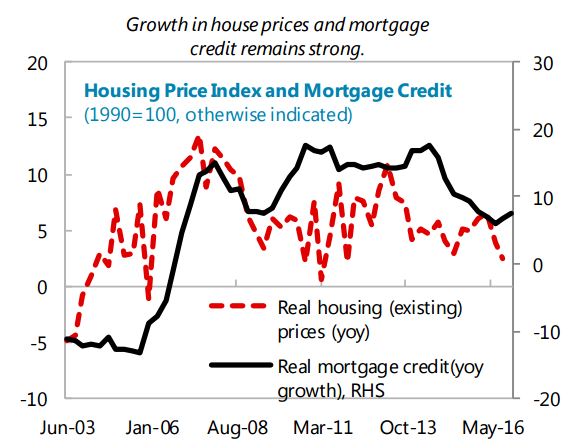

The IMF latest report on Colombia says that “(…) overall credit growth decelerated significantly in 2016. However, the mortgage credit segment has remained resilient with a real growth of 6.8 percent. This is partly due to the various government subsidy programs: around 30 percent of the mortgages originated in 2016 were subsidized. These developments, together with the significant expansion of house prices since 2002, generate questions about the macro-financial risks associated with potential reversals in the housing and mortgage markets. Staff estimated that house prices are slightly misaligned with respect to economic fundamentals, with an estimated price gap of 13.5 percent (…). However, after the 1999 financial crisis the authorities have adopted macroprudential measures such as the use of LTV limits, and other housing financing characteristics (e.g., full recourse, no prepayment penalties, fixed-rate mortgages) that limit the vulnerabilities stemming from the housing market.”

A separate paper “(…) estimates the extent of misalignments in house prices relative to fundamentals and evaluates the overall risk to the economy from the housing sector. The results suggest a moderate house price misalignment relative to fundamentals which is, however, mitigated by housing finance characteristics. ”

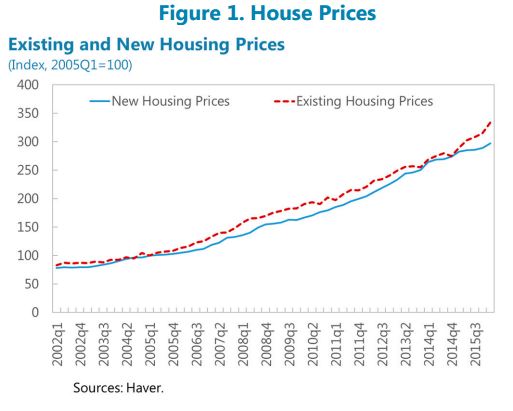

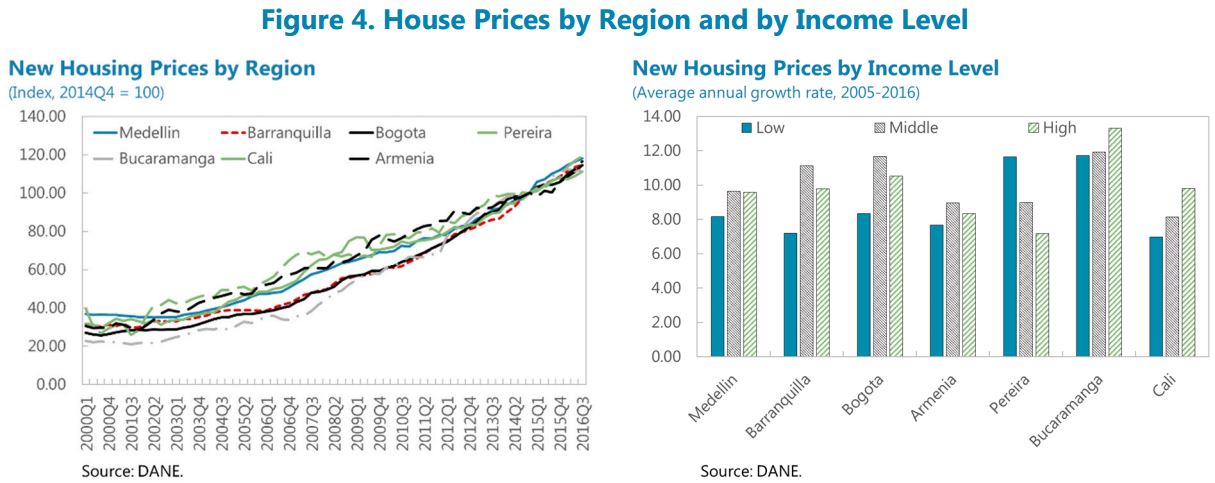

This paper also points out that “The increase in house prices has been widespread across the country. Figure 1 shows that prices for both new and existing houses have increased in the main three cities of Colombia. Figure 4 shows the evolution of prices for new houses in additional cities. Interestingly, house prices grew at high and similar rates in the seven cities considered: the average home-price index grew by an annual real rate of 5.18 percent between 2005 and 2016, with Bucaramanga having the highest average annual real growth rate (8 percent) and Armenia the lowest (3.4 percent). Notwithstanding, in all the cities house prices tended to show stronger growth for middle and upper income levels (Figure 4).”

The IMF latest report on Colombia says that “(…) overall credit growth decelerated significantly in 2016. However, the mortgage credit segment has remained resilient with a real growth of 6.8 percent. This is partly due to the various government subsidy programs: around 30 percent of the mortgages originated in 2016 were subsidized. These developments, together with the significant expansion of house prices since 2002, generate questions about the macro-financial risks associated with potential reversals in the housing and mortgage markets.

Posted by at 5:05 PM

Labels: Global Housing Watch

Is the United States Becoming Less of an Optimal Currency Area?

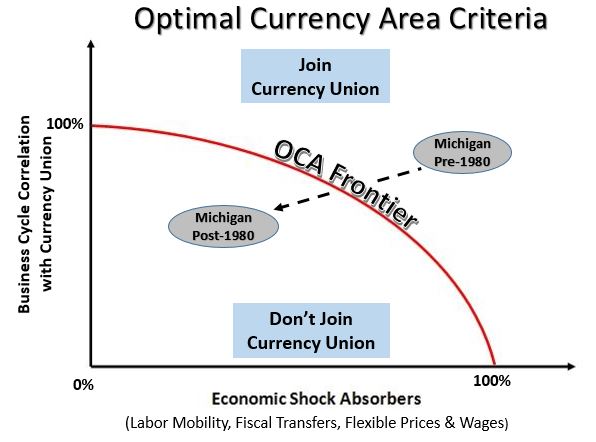

From a new Macro Musings Blog by David Beckworth:

“It took the United States roughly 150 years to become an optimal currency area (OCA), according to economic historian Hugh Rockoff. This long journey meant that it was not until the late 1930s that a one-size-fits-all monetary policy made sense for the U.S. economy. Since then the U.S. economy has often been held up as the best example of a currency union that meets the OCA criteria. This especially was the case when comparisons have been made to the Eurozone, like in this classic Blanchard and Katz (1992) paper. But all is not well in this land of the OCA.

(…)

The policy implications seem clear. Policy makers at the local, state, and federal level need to push policies that increase labor market mobility. There is a lot of work to do on this front, but it is important to do so to keep the United States an OCA. The Schleichner paper provides some suggestions and is good starting point for discussion.”

Continue reading here.

From a new Macro Musings Blog by David Beckworth:

“It took the United States roughly 150 years to become an optimal currency area (OCA), according to economic historian Hugh Rockoff. This long journey meant that it was not until the late 1930s that a one-size-fits-all monetary policy made sense for the U.S. economy. Since then the U.S. economy has often been held up as the best example of a currency union that meets the OCA criteria.

Posted by at 9:18 AM

Labels: Inclusive Growth

Colombia’s Peace Agreement Can Give Fillip to Inclusive Growth

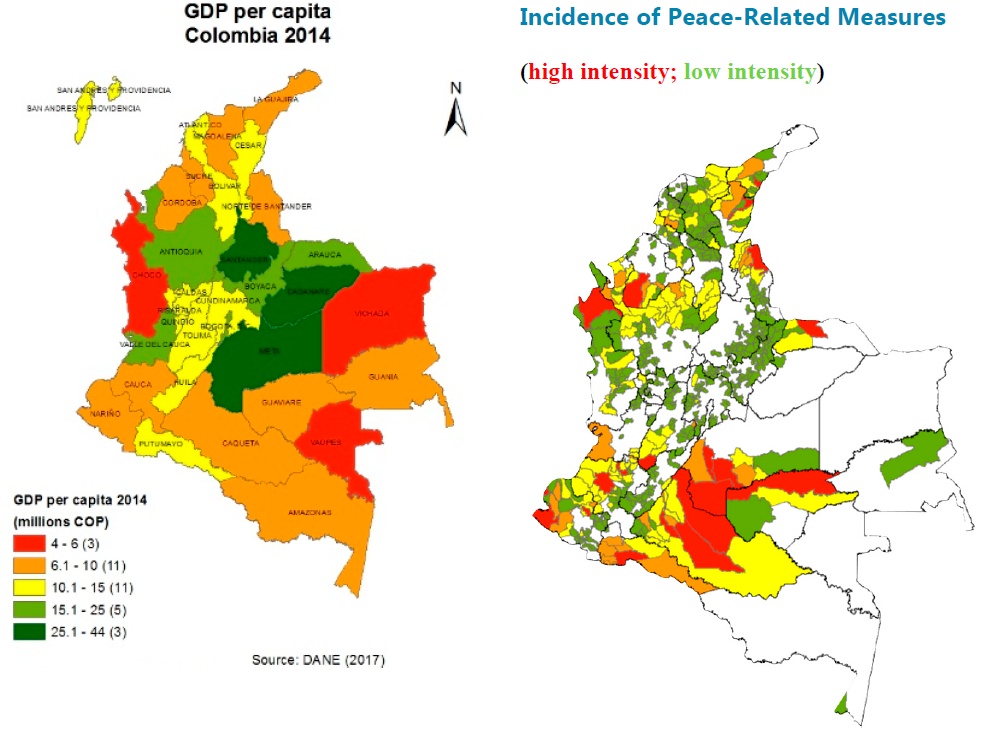

A new IMF annual assessment of the Colombian economy says that “The peace agreement will cement security gains achieved over the last decade and continue to bring more investment to the country. The implementation of the peace agreement will also focus on the regions where income per capita is relatively lower. The delivery of basic public goods and services to remote, poor, and conflict-ridden regions of the country—in addition to Colombia’s improved security conditions—will certainly make growth more inclusive over time.”

Continue reading here.

A new IMF annual assessment of the Colombian economy says that “The peace agreement will cement security gains achieved over the last decade and continue to bring more investment to the country. The implementation of the peace agreement will also focus on the regions where income per capita is relatively lower. The delivery of basic public goods and services to remote, poor, and conflict-ridden regions of the country—in addition to Colombia’s improved security conditions—will certainly make growth more inclusive over time.”

Posted by at 9:08 AM

Labels: Inclusive Growth

Subscribe to: Posts