Monday, November 21, 2016

International Jobs Report: Global Unemployment Inching Up Again

The latest update of the International Jobs Report shows that:

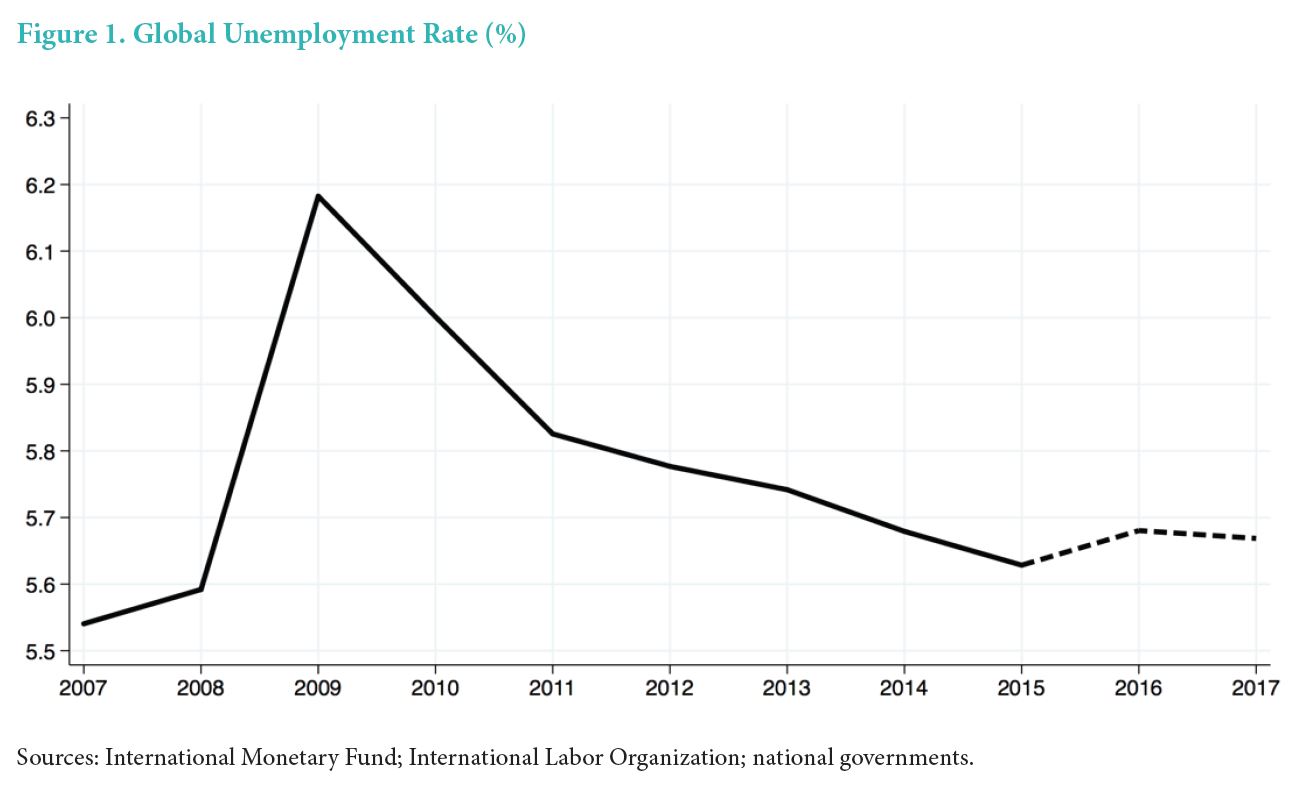

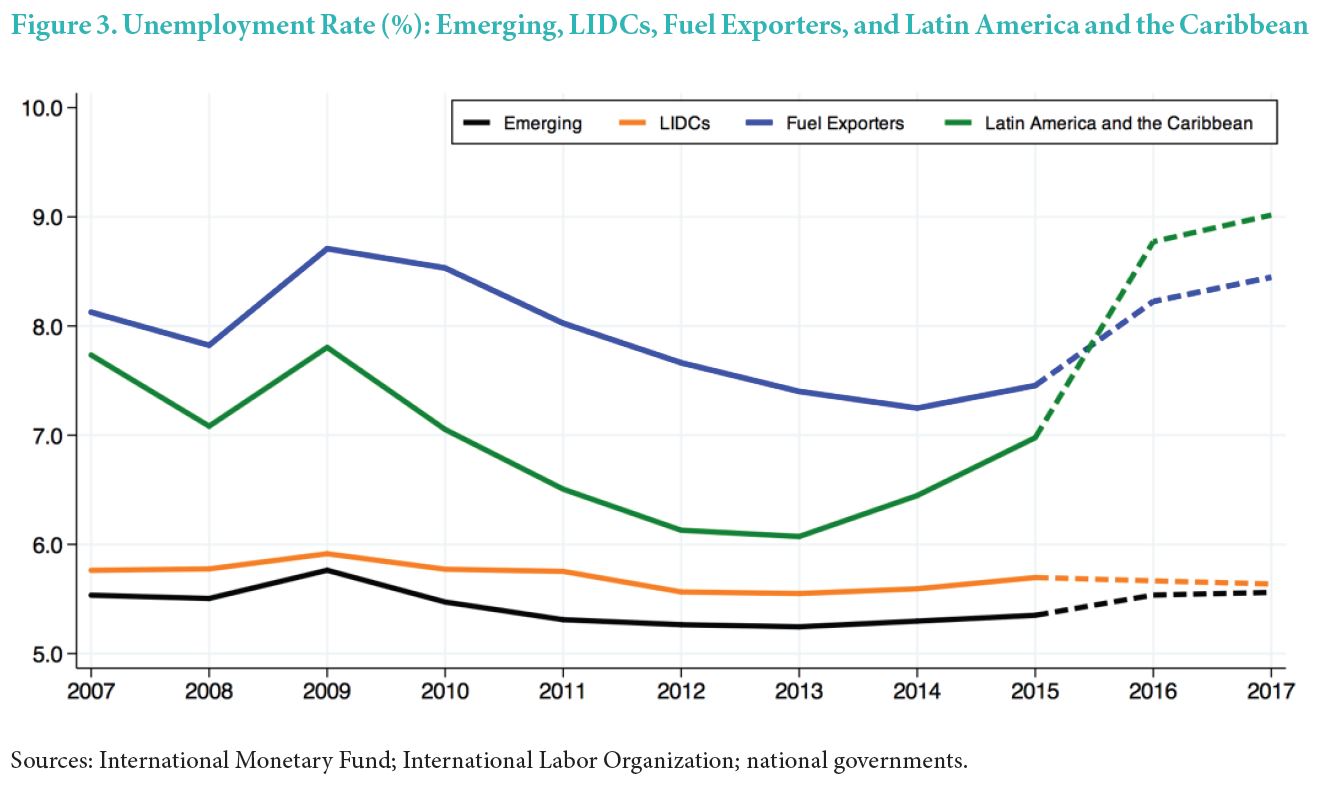

- The global unemployment rate inched up to 5.7 percent this year after several years of decline. This reflects sharp increases in unemployment in the Latin America and Caribbean region and among fuel-exporting countries. Hence, while the total number of people unemployed around the globe will remain somewhat stable at about 175 million, several million people will be added to the ranks of the unemployed in these two groups of countries.

- For fuel exporters, the unemployment rate is expected to shoot up to 8 ½ percent next year. This is a percentage point above the level in 2015 and implies that an additional 4 million more people will join the ranks of the unemployed. For the Latin America and the Caribbean region, the unemployment rate is forecast to reach 9 percent in 2017, which is 2 percentage points above the 2015 level and will add nearly 6 million people to the ranks of the unemployed.

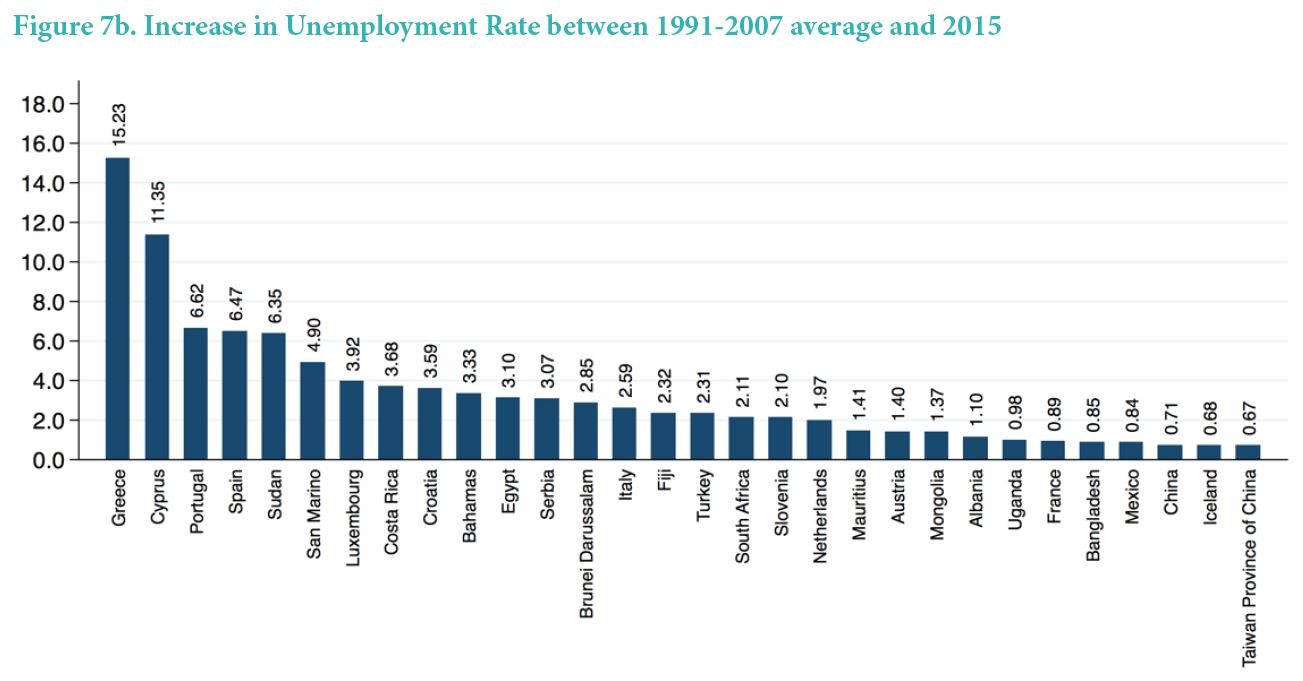

- Unemployment rates are expected to decline in most advanced economies, but remain well above historical averages in a few countries such as Greece, Cyprus, Portugal and Spain.

Read the full report.

The latest update of the International Jobs Report shows that:

- The global unemployment rate inched up to 5.7 percent this year after several years of decline. This reflects sharp increases in unemployment in the Latin America and Caribbean region and among fuel-exporting countries. Hence, while the total number of people unemployed around the globe will remain somewhat stable at about 175 million, several million people will be added to the ranks of the unemployed in these two groups of countries.

Posted by at 2:47 PM

Labels: Inclusive Growth

Thursday, November 17, 2016

Housing Market in Sweden

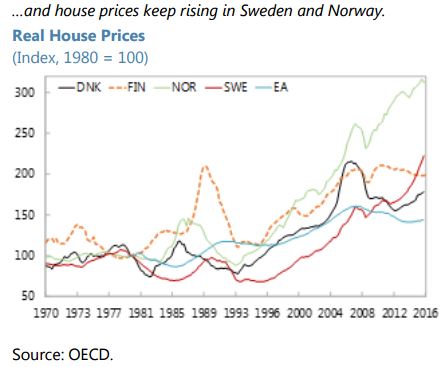

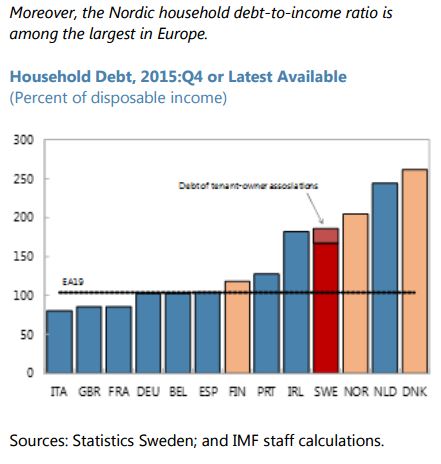

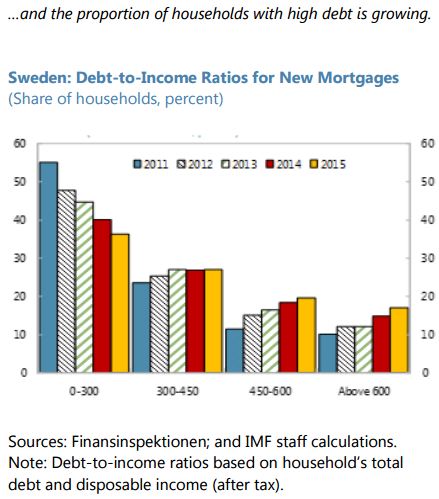

The IMF’s latest Financial System Stability Assessment on Sweden notes the following:

“Housing finance creates vulnerabilities for financial stability due to specific features of Swedish residential mortgages, high household debt, and rising asset prices (…). House prices have risen to high levels, slowing only recently. The price-to-income ratio is 40 percent above its 20-year average, among the highest in advanced economies, raising a red flag. Research suggests that house prices are 12 percent above long-run equilibrium (IMF Working Paper 15/276). House price gains provide incentives for households not to amortize loans and take out even larger loans relative to income, aided by longer loan maturities. Mortgage interest rate deductibility and the lack of a property tax further propel house demand. (…) The pace of housing completions represents less than 1 percent of the housing stock, lagging behind rising population, especially in urban areas. (…) FI’s view is that the rising house prices and high household debt do not entail high credit risk for banks, but they do add to macroeconomic vulnerabilities. (…) High asset valuations do not necessarily lead to asset price declines, but if a fall were to happen, the corrections could be much larger and damaging, especially given the high household debt. (…) Even though households appear resilient, it is challenging to be conclusive about how scenarios of falling asset prices and higher interest rates would play out. (…) The authorities have responded to increasing household debt with macroprudential measures focusing on credit supply (…). The recent amortization requirement and the government’s 22–point proposal for more housing are welcome, but more is needed to address distortions in the housing market.”

The IMF’s latest Financial System Stability Assessment on Sweden notes the following:

“Housing finance creates vulnerabilities for financial stability due to specific features of Swedish residential mortgages, high household debt, and rising asset prices (…). House prices have risen to high levels, slowing only recently. The price-to-income ratio is 40 percent above its 20-year average, among the highest in advanced economies, raising a red flag. Research suggests that house prices are 12 percent above long-run equilibrium (IMF Working Paper 15/276).

Posted by at 4:21 PM

Labels: Global Housing Watch

Thursday, November 10, 2016

Can Property Taxes Reduce House Price Volatility? Evidence from U.S. Regions

A new IMF Working Paper by Tigran Poghosyan “(…) use a novel dataset on effective property tax rates in U.S. states and metropolitan statistical areas (MSAs) over the 2005–2014 period to analyze the relationship between property tax rates and house price volatility. (…) [Poghosyan] find that property tax rates have a negative impact on house price volatility. The impact is causal, with increases in property tax rates leading to a reduction in house price volatility. The results are robust to different measures of house price volatility, estimation methodologies, and additional controls for housing demand and supply. The outcomes of the analysis have important policy implications and suggest that property taxation could be used as an important tool to dampen house price volatility.”

Please note that IMF Working Papers do not represent the official views of the IMF.

A new IMF Working Paper by Tigran Poghosyan “(…) use a novel dataset on effective property tax rates in U.S. states and metropolitan statistical areas (MSAs) over the 2005–2014 period to analyze the relationship between property tax rates and house price volatility. (…) [Poghosyan] find that property tax rates have a negative impact on house price volatility. The impact is causal, with increases in property tax rates leading to a reduction in house price volatility.

Posted by at 4:17 PM

Labels: Global Housing Watch

Sunday, November 6, 2016

Was Krugman Right? Unemployment during the Great Recession

Paul Krugman wrote in 2011 that unemployment was high “because growth is weak — period, full stop, end of story.” Six years later, has he been proven right? Read my post for Econbrowser to get the answer.

Paul Krugman wrote in 2011 that unemployment was high “because growth is weak — period, full stop, end of story.” Six years later, has he been proven right? Read my post for Econbrowser to get the answer.

Posted by at 7:55 AM

Labels: Inclusive Growth

Thursday, October 27, 2016

A “New Normal” for the Oil Market

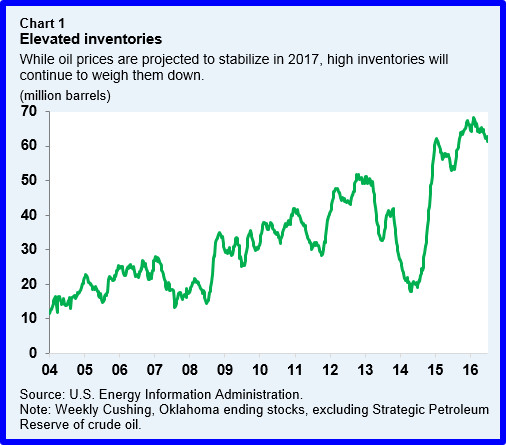

From iMFdirect:

While oil prices have stabilized somewhat in recent months, there are good reasons to believe they won’t return to the high levels that preceded their historic collapse two years ago. For one thing, shale oil production has permanently added to supply at lower prices. For another, demand will be curtailed by slower growth in emerging markets and global efforts to cut down on carbon emissions. It all adds up to a “new normal” for oil.

The “new” oil supply

Shale has been a game changer. Unexpectedly strong shale-oil production of 5 million barrels per day contributed to the global supply glut. That, along with the surprising decision by the Organization of the Petroleum Exporting Countries (OPEC) to keep production unchanged, contributed to the oil price collapse that started in June 2014.

Although the price collapse led to a massive cut in oil investment, production was slow to respond, keeping supply in excess. What’s more, the resilience of shale production to lower prices again surprised market participants, leading to even lower prices in 2015. Shale drillers significantly cut costs by improving efficiency, allowing major players to avoid bankruptcy. While reduced investment is expected to result in lower production by non-OPEC countries in 2016, production still exceeds consumption. Many experts expect oil markets to balance in 2017, albeit with high level of inventory (Chart 1). That said, there is uncertainty regarding supply, especially regarding the cost associated with extraction as well as production from so-called shale “fracklog”—drilled but uncompleted wells. The latter can add to production flows in a matter of weeks and hence considerably change the dynamics of production compared to conventional oil—that features long lead times between investment and production.

Against that backdrop, OPEC countries and Russia have been increasing output, and Iran’s return to markets has added even more supply. (While OPEC members have recently agreed to cut production, that agreement is yet to be finalized.) There are other factors at play. Recent data suggest that shale-oil production may be once again more resilient than expected. And the anticipation of an OPEC production cut in cooperation with other exporters has boosted prices to the level that will further stimulate output by many shale producers.

Continue reading here.

From iMFdirect:

While oil prices have stabilized somewhat in recent months, there are good reasons to believe they won’t return to the high levels that preceded their historic collapse two years ago. For one thing, shale oil production has permanently added to supply at lower prices. For another, demand will be curtailed by slower growth in emerging markets and global efforts to cut down on carbon emissions. It all adds up to a “new normal” for oil.

Posted by at 11:47 AM

Labels: Energy & Climate Change

Subscribe to: Posts