Thursday, November 17, 2016

Housing Market in Sweden

The IMF’s latest Financial System Stability Assessment on Sweden notes the following:

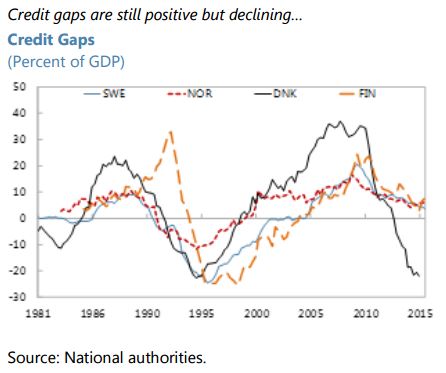

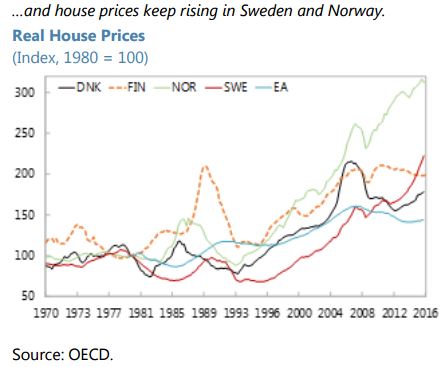

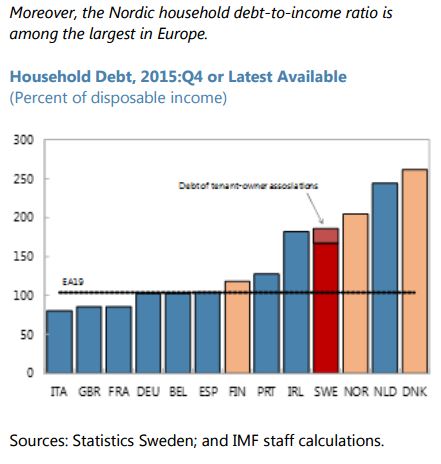

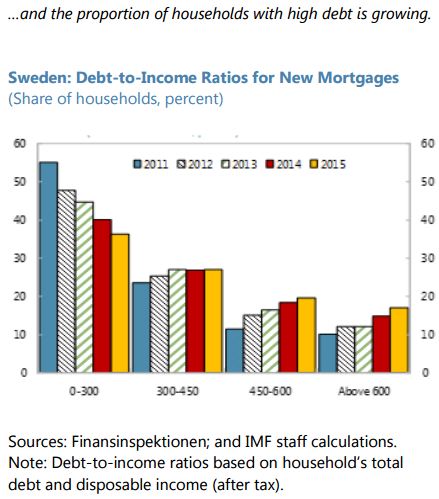

“Housing finance creates vulnerabilities for financial stability due to specific features of Swedish residential mortgages, high household debt, and rising asset prices (…). House prices have risen to high levels, slowing only recently. The price-to-income ratio is 40 percent above its 20-year average, among the highest in advanced economies, raising a red flag. Research suggests that house prices are 12 percent above long-run equilibrium (IMF Working Paper 15/276). House price gains provide incentives for households not to amortize loans and take out even larger loans relative to income, aided by longer loan maturities. Mortgage interest rate deductibility and the lack of a property tax further propel house demand. (…) The pace of housing completions represents less than 1 percent of the housing stock, lagging behind rising population, especially in urban areas. (…) FI’s view is that the rising house prices and high household debt do not entail high credit risk for banks, but they do add to macroeconomic vulnerabilities. (…) High asset valuations do not necessarily lead to asset price declines, but if a fall were to happen, the corrections could be much larger and damaging, especially given the high household debt. (…) Even though households appear resilient, it is challenging to be conclusive about how scenarios of falling asset prices and higher interest rates would play out. (…) The authorities have responded to increasing household debt with macroprudential measures focusing on credit supply (…). The recent amortization requirement and the government’s 22–point proposal for more housing are welcome, but more is needed to address distortions in the housing market.”

Posted by at 4:21 PM

Labels: Global Housing Watch

Subscribe to: Posts