Tuesday, December 13, 2016

When China Sneezes Does ASEAN Catch a Cold?

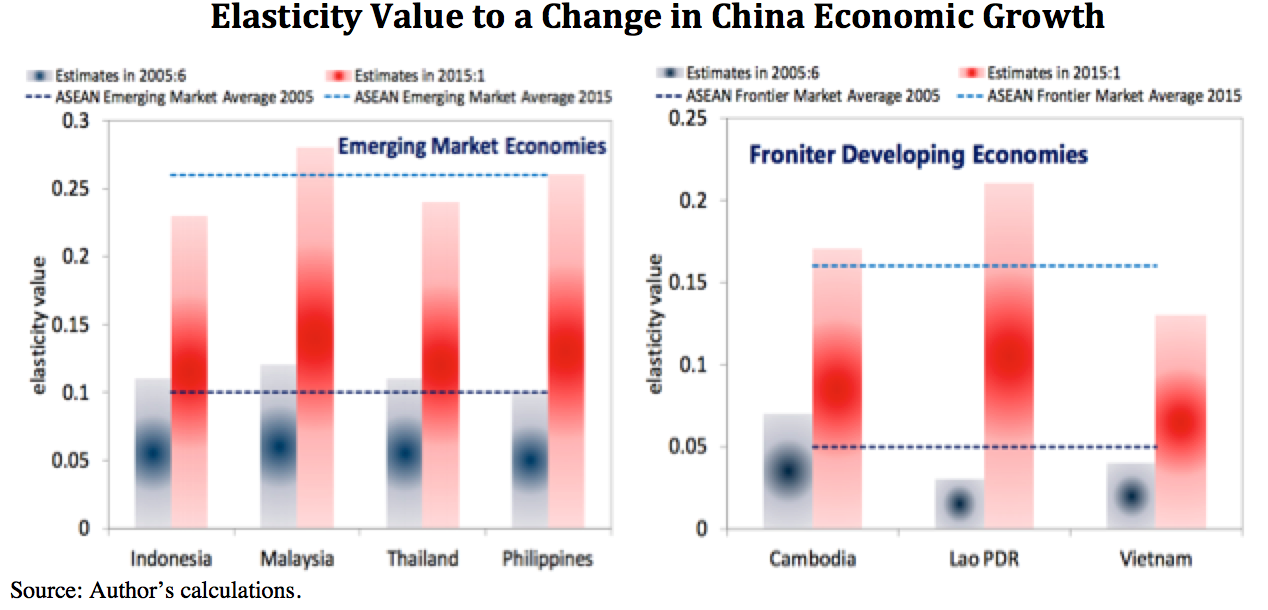

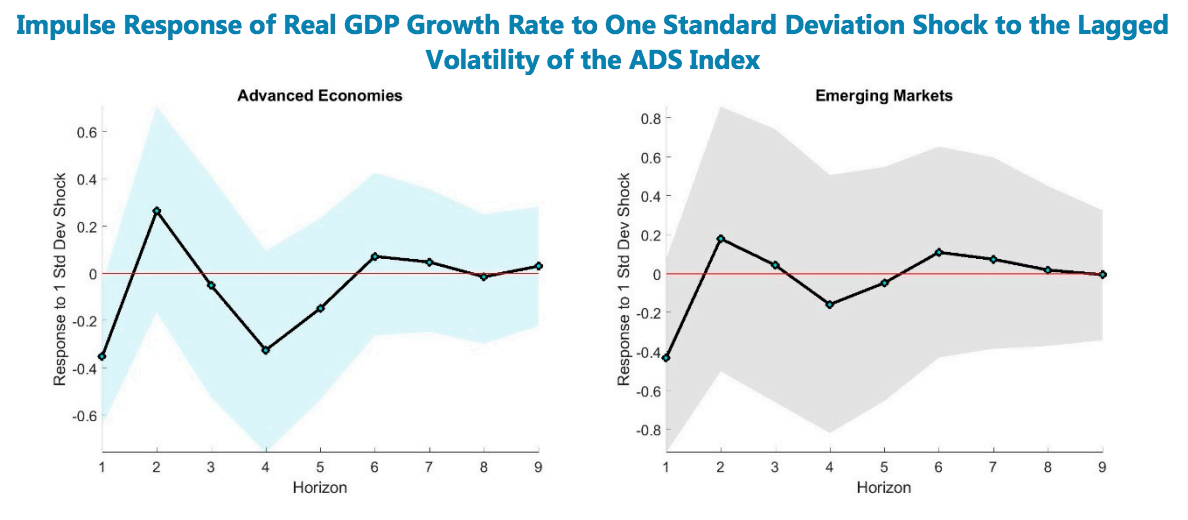

This paper looks at the effects of a China slowdown on Emerging Market Economies (Indonesia, Malaysia, and Thailand) and Frontier Developing Economies (Cambodia, Lao P.D.R., and Vietnam) in ASEAN. The main finding is that the impact of China growth shocks on ASEAN has risen since the global financial crisis. A one percent decline in China’s growth implies a 0.3 percent reduction in growth for ASEAN EMEs and 0.2 for FDEs. An important component of inflation is also shared between ASEAN and China. These magnitudes are double what they were two decades ago due to stronger trade and financial linkages. Finally, a slowdown in China, while having real effects, also has a financial impact via slower credit growth and lower equity prices. This is in line with the existence of both portfolio balance and signaling channels, in which ASEAN market participants absorb news on China economic activity as an indicator over domestic growth prospects.

For details, see the new IMF Working Paper.

This paper looks at the effects of a China slowdown on Emerging Market Economies (Indonesia, Malaysia, and Thailand) and Frontier Developing Economies (Cambodia, Lao P.D.R., and Vietnam) in ASEAN. The main finding is that the impact of China growth shocks on ASEAN has risen since the global financial crisis. A one percent decline in China’s growth implies a 0.3 percent reduction in growth for ASEAN EMEs and 0.2 for FDEs. An important component of inflation is also shared between ASEAN and China.

Posted by at 2:53 PM

Labels: Forecasting Forum

Forecast Errors and Uncertainty Shocks

Macroeconomic forecasts are persistently too optimistic. This paper finds that common factors related to general uncertainty about U.S. macrofinancial prospects and global demand drive this overoptimism. These common factors matter most for advanced economies and G- 20 countries. The results suggest that an increase in uncertainty-driven overoptimism has dampening effects on next-year real GDP growth rates. This implies that incorporating the common structure governing forecast errors across countries can help improve subsequent forecasts.

For details, see the new IMF Working Paper.

Macroeconomic forecasts are persistently too optimistic. This paper finds that common factors related to general uncertainty about U.S. macrofinancial prospects and global demand drive this overoptimism. These common factors matter most for advanced economies and G- 20 countries. The results suggest that an increase in uncertainty-driven overoptimism has dampening effects on next-year real GDP growth rates. This implies that incorporating the common structure governing forecast errors across countries can help improve subsequent forecasts.

For details,

Posted by at 2:37 PM

Labels: Forecasting Forum

Monday, December 12, 2016

The IMF is Not Asking Greece for More Austerity

Greece is once again in the headlines as discussions for the second review of its European Stability Mechanism (ESM) program are gaining pace. Unfortunately, the discussions have also spurred some misinformation about the role and the views of the IMF. Above all, the IMF is being criticized for demanding more fiscal austerity, in particular for making this a condition for urgently needed debt relief. This is not true, and clarifications are in order.

The IMF is not demanding more austerity. On the contrary, when the Greek Government agreed with its European partners in the context of the ESM program to push the Greek economy to a primary fiscal surplus of 3.5 percent by 2018, we warned that this would generate a degree of austerity that could prevent the nascent recovery from taking hold. We projected that the measures in the ESM program will deliver a surplus of only 1.5 percent of GDP, and said this would be enough for us to support a program. We did not call for additional measures to achieve a higher surplus. But contrary to our advice, the Greek Government agreed with the European institutions to temporarily compress spending further if needed to ensure that the surplus would reach 3.5 percent of GDP.

We have not changed our view that Greece does not need more austerity at this time. Claiming that it is the IMF who is calling for this turns the truth upside down.

Continue reading here.

Greece is once again in the headlines as discussions for the second review of its European Stability Mechanism (ESM) program are gaining pace. Unfortunately, the discussions have also spurred some misinformation about the role and the views of the IMF. Above all, the IMF is being criticized for demanding more fiscal austerity, in particular for making this a condition for urgently needed debt relief. This is not true,

Posted by at 5:07 PM

Labels: Inclusive Growth

Friday, December 9, 2016

Housing Market in Chile

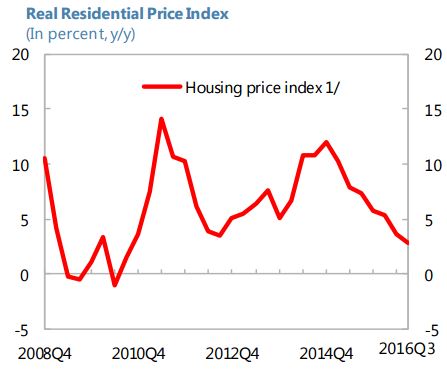

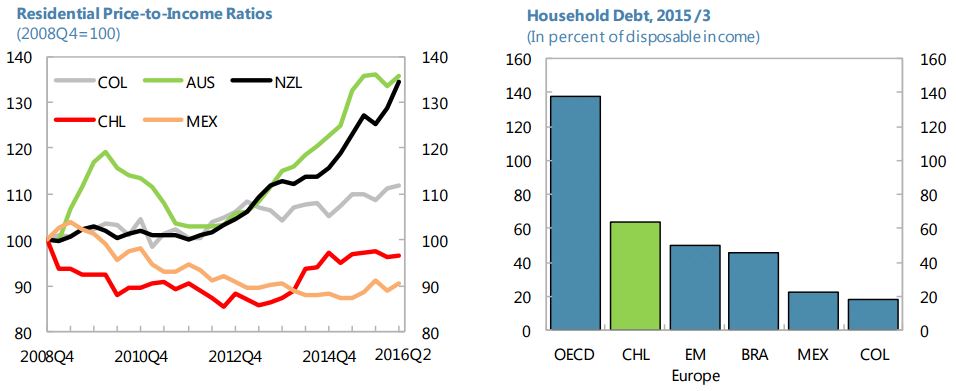

“Housing prices have grown at a relatively fast pace in Chile, prior to an impending VAT increase in 2016. Residential property sales have fallen sharply since early 2016. Housing prices are cooling down rapidly. Household debt has increased, driven by mortgage loans. Still, the price-to-income ratio has stabilized recently (…) and, the debt-to-income ratio in Chile remains low relative to advanced economies”, according to IMF’s latest report on Chile.

“Housing prices have grown at a relatively fast pace in Chile, prior to an impending VAT increase in 2016. Residential property sales have fallen sharply since early 2016. Housing prices are cooling down rapidly. Household debt has increased, driven by mortgage loans. Still, the price-to-income ratio has stabilized recently (…) and, the debt-to-income ratio in Chile remains low relative to advanced economies”, according to IMF’s latest report on Chile.

Posted by at 3:27 PM

Labels: Global Housing Watch

Thursday, December 8, 2016

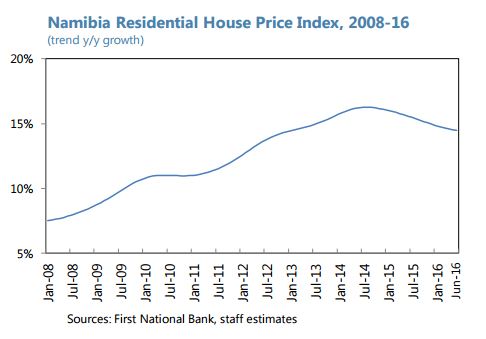

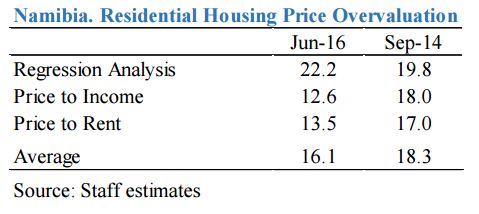

Housing Market in Namibia

“While decelerating, residential real estate prices continue their fast growing trend. (…) On average, house prices remain overvalued, raising risks of possible price corrections. Using common housing ratios and regression analysis from a cross country sample of house price reversal as in the 2015 Article IV staff report, staff estimates that in June 2016 the house price overvaluation at national level was on average around 16 percent, slightly lower than estimated in the 2015 Article IV. The reduction is attributable both to the recent slowdown in price growth and to revisions to the historical values of the housing index. (…) Despite their large exposure to mortgage loans, banks remain resilient to large house price corrections with pressures arising only under tail risk scenarios”, says IMF’s report on Namibia.

“While decelerating, residential real estate prices continue their fast growing trend. (…) On average, house prices remain overvalued, raising risks of possible price corrections. Using common housing ratios and regression analysis from a cross country sample of house price reversal as in the 2015 Article IV staff report, staff estimates that in June 2016 the house price overvaluation at national level was on average around 16 percent,

Posted by at 3:11 PM

Labels: Global Housing Watch

Subscribe to: Posts