Saturday, March 28, 2015

House prices in Ireland

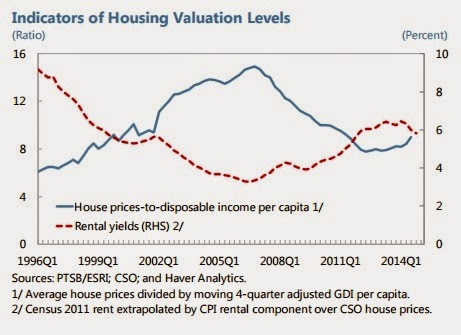

The latest IMF report for Ireland says: “Property markets are bouncing back rapidly. Commercial real estate values are up 30.7 percent y/y in 2014, though they still remain about 30 percent below pre-boom levels. Values were bolstered by record transaction volumes with over one-third reflecting foreign investment inflows. At the same time, house prices rose 16.3 percent y/y, as fast as the increases during the boom period, though they are still 38 percent below peak.”

Posted by at 1:04 AM

Labels: Global Housing Watch

Saturday, March 21, 2015

Housing Wealth and Inequality

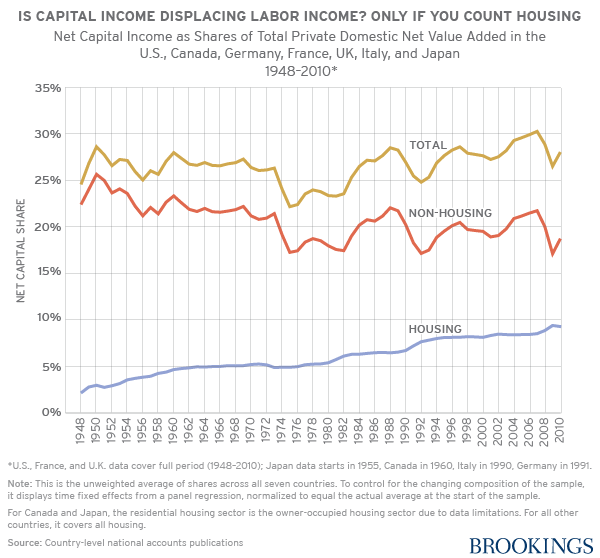

Beyond housing, the results in this paper suggest that concern about inequality should be shifted away from the split between capital and labor, and toward other aspects of distribution, such as the within-labor distribution of income. Although the net capital share has at times seen dramatic shifts both up and down, away from housing its long-term movement has been quite small, and there is not strong reason to suspect that this pattern will change going forward.”

Matt Rognlie concludes: “Housing has a pivotal role in the modern story of income distribution. Since housing has relatively broad ownership, it does not conform to the traditional story of labor versus capital, nor can its growth be easily explained with many of the stories commonly proposed for the income split elsewhere in the economy—the bargaining power of labor, the growing role of technology, and so on.

Beyond housing, the results in this paper suggest that concern about inequality should be shifted away from the split between capital and labor,

Posted by at 7:55 PM

Labels: Global Housing Watch

Thursday, March 19, 2015

House Prices in Indonesia

“Higher borrowing costs and macro prudential measures have helped moderate growth in property prices,” notes the IMF’s latest annual economic report on Indonesia.

Posted by at 2:11 PM

Labels: Global Housing Watch

Friday, March 13, 2015

House Prices in Iceland

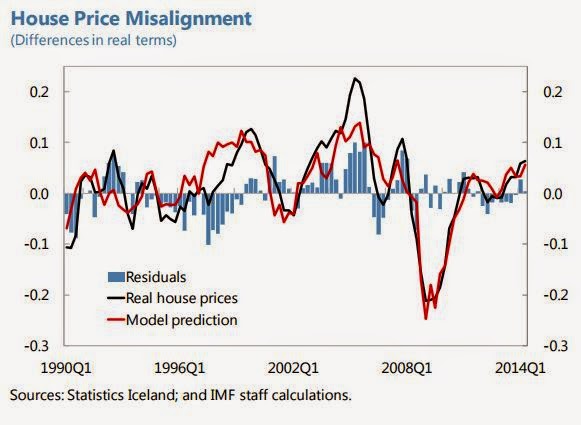

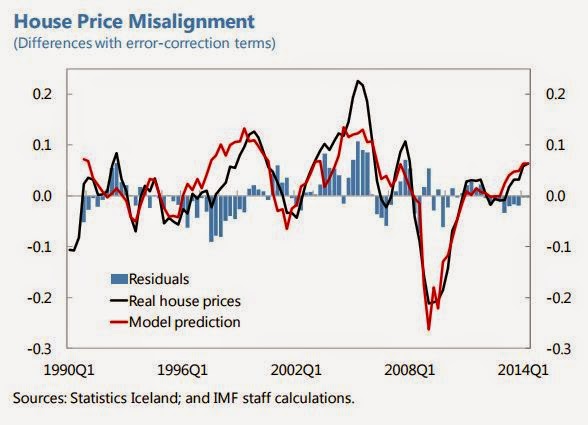

bubbles. House prices in Iceland have been rising rapidly in the recent period, prompting

concerns about possible overvaluation. Based on a cross-country comparison, time-series

analysis, and correlation analysis, house prices in Iceland do not stand out as particularly

misaligned. To formally test whether the housing market is overvalued, we employ the

Igan and Loungani (2012) model based on housing affordability, per capita income,

population, stock prices, credit, and interest rates. We find that there are currently no

misalignments between house prices and the fundamentals, which is consistent with the

recent analysis conducted by the CBI. However, housing supply-side constraints remain

significant, with new starts well below the historic norm. These, together with the ongoing

recovery in mortgage lending, the wealth and income effects of household debt relief and

Pillar III withdrawals to fund debt relief (and, until discontinued in 2015 budget, for

general consumption), increasing demand for vacation properties, and potentially large

wage hikes in the near-term, may lead to an overshooting of house prices. Policies that

could be explored (while keeping an eye on broader macroeconomic considerations) to

help minimize the risks of asset price bubbles in the housing sector include steps to: (i)

support measured increases in housing supply; (ii) maintain non-inflationary growth in

wages; (iii) prevent excessive leveraging; and (iv) increase household savings.”

A new IMF paper on asset price bubbles says that “One of the potential costs of prolonged capital controls is the formation of asset price

bubbles. House prices in Iceland have been rising rapidly in the recent period, prompting

concerns about possible overvaluation. Based on a cross-country comparison, time-series

analysis, and correlation analysis, house prices in Iceland do not stand out as particularly

misaligned. To formally test whether the housing market is overvalued, Read the full article…

Posted by at 5:29 PM

Labels: Global Housing Watch

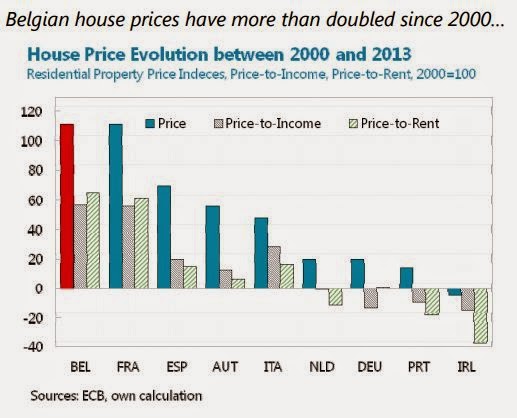

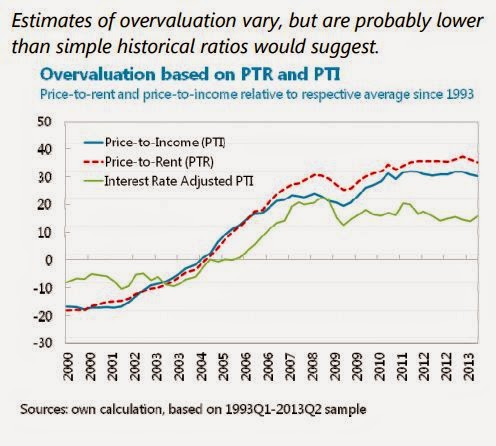

House Prices in Belgium

Moreover, the paper says that “there is a continued need for vigilance and policy coordination. Recent changes in macro-prudential and fiscal policy seem appropriate to make the housing market safer and reduce untargeted fiscal expenditures. To assure that the price adjustment remains orderly and does not lead to overshooting, future policy changes should be gradual and coordinated among different institutions. A well communicated housing strategy could help to avoid price mis-alignments in the future.”

A new IMF paper “(…) argues that current house prices are closer to their equilibrium than simple historical ratios would suggest and that given the moderate overvaluation, a gradual and limited adjustment seems a plausible scenario. Strong household balance sheets, a seemingly well-managed mortgage market and various institutional characteristics reduce the risk of an abrupt correction. Given that historical house price changes have had moderate macro-economic effects – with the exception of residential investment – the repercussions of a gradual decline seem manageable.” Read the full article…

Posted by at 2:32 PM

Labels: Global Housing Watch

Subscribe to: Posts