Wednesday, July 15, 2015

House Prices in Germany

“The moderate upward trend in housing prices continues and the appropriate response at this stage is close monitoring and readying the macroprudential toolkit. After years of stagnation, nominal housing prices at the aggregate level have grown at an annual pace of 3–4 percent for the past five years—only marginally faster than the growth in disposable income. In spite of falling lending rates, mortgage loan growth remains modest and lending standards appear stable. Thus, there are no signs of overheating yet. Read the full article…

Posted by at 6:52 PM

Labels: Global Housing Watch

Tuesday, July 14, 2015

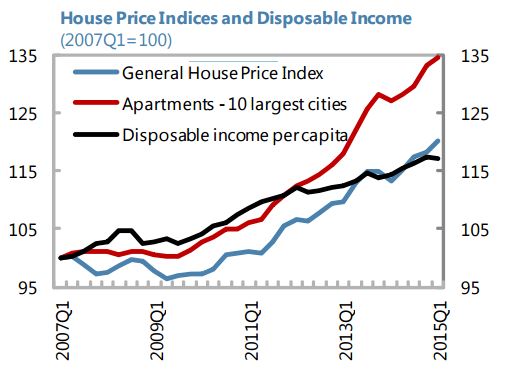

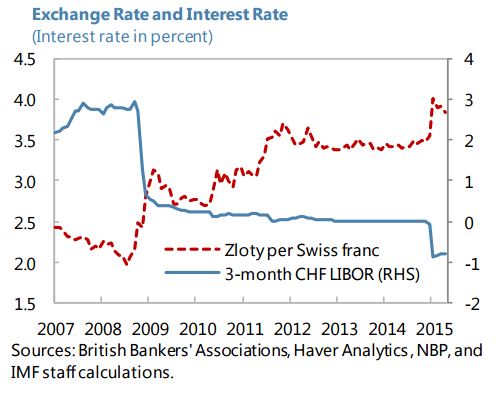

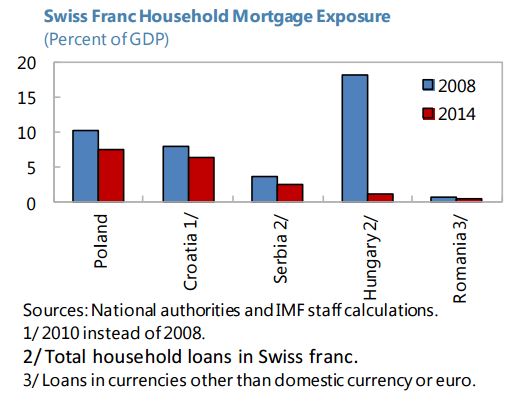

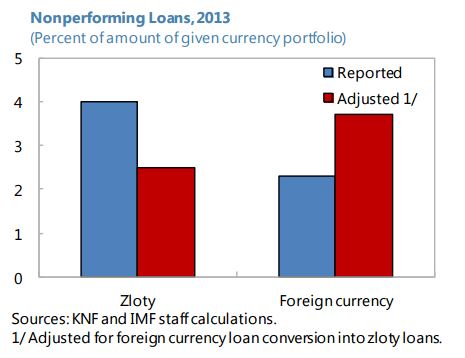

Housing Market in Poland

On foreign-currency mortgages, the new IMF report on Poland says that “While tighter prudential regulation has halted new FX lending, a substantial legacy stock of these loans remains. Close to half of mortgages are denominated in FX (mostly Swiss franc), exposing households and banks to sudden zloty depreciation—as was the case in January when the zloty depreciated around 20 percent against the Swiss franc. As such, the January episode had little macroeconomic impact and high capital buffers in banks mitigated financial stability risks. Read the full article…

Posted by at 6:52 PM

Labels: Global Housing Watch

Friday, July 10, 2015

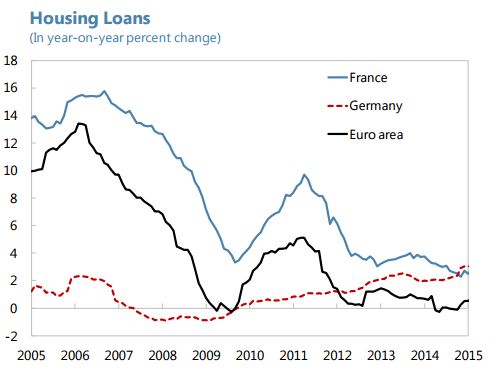

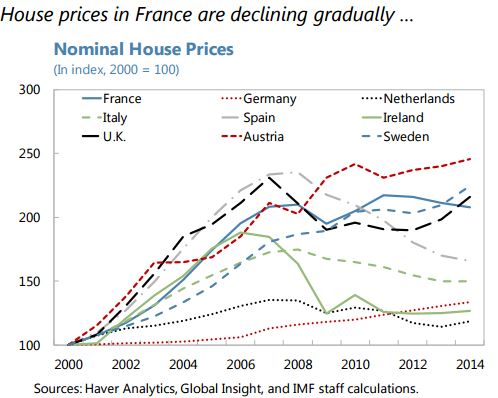

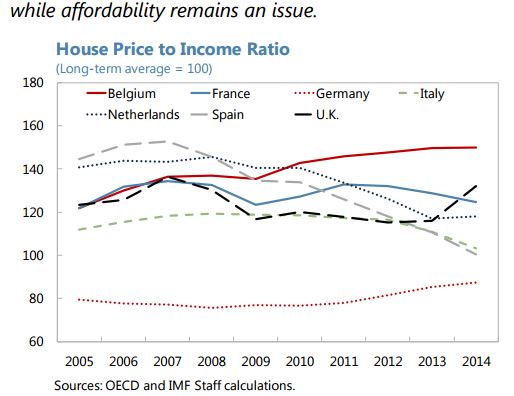

Housing Market in France

Moreover, the report says that “More could be done to alleviate structural rigidities in the housing market. Residential construction has fallen by 14 percent, and real house prices by 11 percent, since the peak in 2007. While this decline is partly cyclical, a succession of laws introducing regulatory and tax changes may also have contributed. Another long-standing factor affecting the market is the extensive system of housing subsidies, which include rental cash assistance (received by 44 percent of tenants), subsidized mortgage rates for households, and fiscal breaks for providers (including of social housing), together amounting to 1.9 percent of GDP in 2013. While these were aimed at making housing more affordable, studies have found that rental assistance may contribute to rising rents. Staff recommended reviewing the functioning of the housing market, with a view to alleviating constraints on the supply of affordable housing and improving the targeting of benefits.”

A separate IMF note on the Financial Sector, Housing Prices and Private Balance Sheets notes the following: “House prices have continued to decline gently since their peak in 2011, but affordability metrics remain above long-run averages. House price overvaluation is currently estimated at around 10–15 percent. Nevertheless, household debt appears manageable, at around 10–15 percent.

On the housing market, “they [the French government] do not see risks to financial stability at this point, given prudent lending practices based on repayment ability, the predominance of fixed-rate mortgages, and the mortgage insurance scheme”, according to the new IMF report on France.

Moreover, the report says that “More could be done to alleviate structural rigidities in the housing market. Residential construction has fallen by 14 percent, and real house prices by 11 percent,

Posted by at 6:11 PM

Labels: Global Housing Watch

Tuesday, July 7, 2015

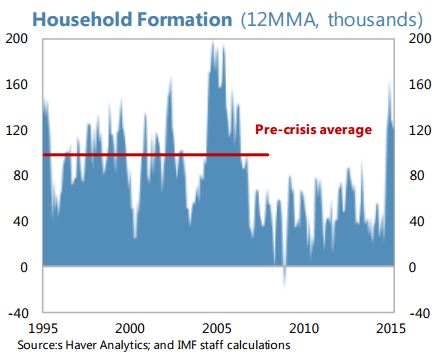

US Housing Market

Also, a separate IMF report on US housing finance notes that “While a number of important steps have been taken to address the structural weaknesses exposed by the crisis in mortgage markets, comprehensive housing finance reform remains the largest piece of unfinished business. In particular, it is not clear when Fannie Mae and Freddie Mac will exit conservatorship and what an end point for a reformed housing finance system will look like. This creates not only fiscal but also financial risks: moral hazard from coverage of credit losses by the government or the government-sponsored enterprises, a distorted competitive landscape due to the dominant footprint of Fannie Mae and Freddie Mac, and large subsidies for homeownership that create incentives to take on excessive levels of household debt.”

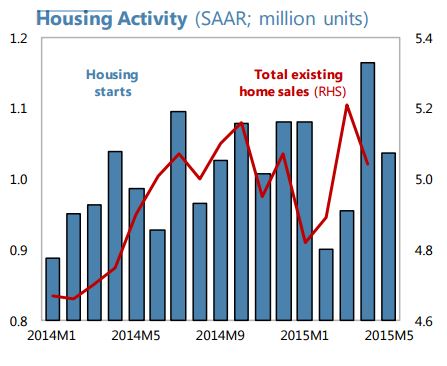

The latest IMF report on the United States points out the following: “Housing market activity has struggled to recover. Up until recently, household formation has been depressed despite the potential for pent-up demand from demographics and more secure job prospects. The slow return of millennials to the first-time home buyers market could signal a preference shift away from traditional suburban, owner-occupied housing. Indeed, the urban rental market remains strong which could represent an enduring increase in demand for multi-family housing units with a smaller square footage. Read the full article…

Posted by at 5:12 PM

Labels: Global Housing Watch

Tuesday, June 30, 2015

Latest Work on Macroprudential Policy

Since the Great Recession, there has been a lot of research done on macroprudential policy. Here is the new research of the past month:

Macruprudential policy in country-specific cases: A new IMF paper reviews the use of macroprudential policy in Hong Kong SAR, the Netherlands, New Zealand, Singapore, and Sweden. The analysis shows that each country reviewed adopted an institutional framework for macroprudential policy suited to their own circumstances. The evidence reviewed confirms that “one size does not fit all,” and that it is possible to conduct macroprudential policy with a heterogenous set of institutional frameworks. In all cases, most of the macroprudential tools used were directed at containing risks arising from a booming housing market (for e.g., LTV and DSTI ratio limits). This study complements an earlier note issued by the IMF, which provides a framework for staff’s advice on macroprudential policy in its bilateral surveillance.

Macroprudential policy in Asia and Pacific: A new working paper from the Bank for International Settlements (BIS) finds that macroprudential policies are more successful when they complement monetary policy by reinforcing monetary tightening, than when they act in opposite directions (on a related note, see Box IV.A of the latest BIS annual report).

Macroprudential policy in Europe: A new paper from the European Central Bank (ECB) says that policies need to be granular enough to deal with the fact that property credit cycles can exhibit strong regional features. There is increasing theoretical support and empirical evidence that borrower-based regulatory policies can be effective, diminishing the credibility of claims that there is not enough experience to practically apply such instruments. In the case of the euro area there may be room in a significant number of countries for putting these instruments more clearly in the hands of newly created macroprudential policy authorities and for creating coordination mechanisms for national LTV or DTI policies at the area-wide level to address the cross-border spillovers potentially caused by these policies.

Experience with macroprudential policy: Research by Kenneth N. Kuttner (Williams College) and Ilhyock Shim (BIS) concurs with the work of others who say that experience with macro-prudential policy measures in various countries is not extensive and may, in any case, have only limited applicability elsewhere because of differences in economic conditions, the relative importance of capital market and traditional bank intermediation, and many other factors. Therefore, it would be unwise to rely solely on macroprodudential policies for taming financial booms and busts.

Riksbank macroprudential conference: The Riksbank has started to hold an annual conference for frontier thinking on macroprudential policies. The keynote speaker at this year’s conference was Raghuram Rajan, Governor of the Reserve Bank of India. It also included presentations from: Jeremy Stein of Harvard University, Atif Mian of Princeton University, Gianni De Nicolò of the IMF and others.

From the Global Housing Watch Newsletter: June 2015

Since the Great Recession, there has been a lot of research done on macroprudential policy. Here is the new research of the past month:

Macruprudential policy in country-specific cases: A new IMF paper reviews the use of macroprudential policy in Hong Kong SAR, the Netherlands, New Zealand, Singapore, and Sweden. The analysis shows that each country reviewed adopted an institutional framework for macroprudential policy suited to their own circumstances.

Posted by at 12:50 PM

Labels: Global Housing Watch

Subscribe to: Posts