Friday, July 12, 2013

House Prices in Malta

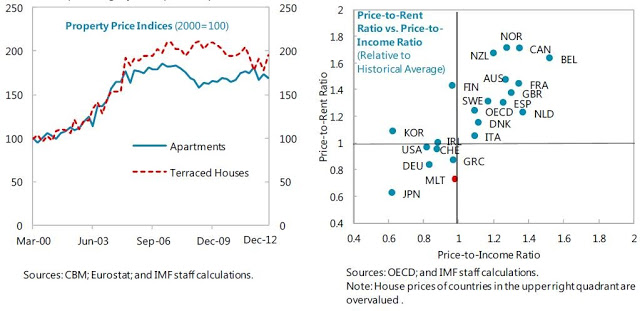

“House prices slightly below pre-crisis peaks,” says IMF’s report on Malta that was released today. According to the report, “the fall in property prices was not drastic. The decline in property prices during the crisis was 8 percent. The loss in household wealth from property was thus moderate. Malta’s house prices are one of the most undervalued amongst the advanced economy countries, indicating there is no potential risk of correction in the property market. Both the price-to-income and price-to rent ratio remain one of the lowest among the advanced economies.”

“House prices slightly below pre-crisis peaks,” says IMF’s report on Malta that was released today. According to the report, “the fall in property prices was not drastic. The decline in property prices during the crisis was 8 percent. The loss in household wealth from property was thus moderate. Malta’s house prices are one of the most undervalued amongst the advanced economy countries, indicating there is no potential risk of correction in the property market. Both the price-to-income and price-to rent ratio remain one of the lowest among the advanced economies.”

Posted by at 9:41 PM

Labels: Global Housing Watch

Wednesday, July 10, 2013

House Prices in Chile

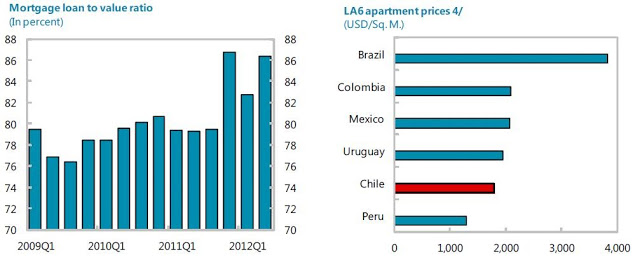

“The increase in housing prices has been strong but standard indicators do not suggest significant misalignment with fundamentals,” according to latest IMF’s report on Chile. On real estate developments, the report says that “real estate activity (supply and demand) has been dynamic. While residential housing prices in aggregate do not suggest bubbles, these averages hide considerable variation and some regions have seen substantial price increases that could spill over to other parts of the country. One sign of incipient froth in the housing market is the jump in average loan-to-value ratios to above 85 percent since late 2011, as highlighted in recent central bank financial stability reports. Another issue is the above-mentioned worsening in construction companies’ financial strength. As for construction, while residential housing activity seems to be cooling off, commercial real estate (for which data are spotty) remains hot with a substantial amount of office space being completed in 2013-14.”

“The increase in housing prices has been strong but standard indicators do not suggest significant misalignment with fundamentals,” according to latest IMF’s report on Chile. On real estate developments, the report says that “real estate activity (supply and demand) has been dynamic. While residential housing prices in aggregate do not suggest bubbles, these averages hide considerable variation and some regions have seen substantial price increases that could spill over to other parts of the country. One sign of incipient froth in the housing market is the jump in average loan-to-value ratios to above 85 percent since late 2011,

Posted by at 2:39 PM

Labels: Global Housing Watch

Friday, June 21, 2013

Does Fiscal Consolidation Raise Inequality?

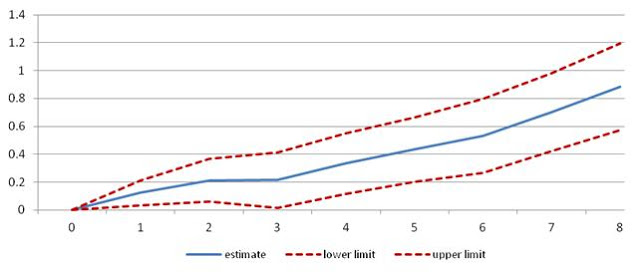

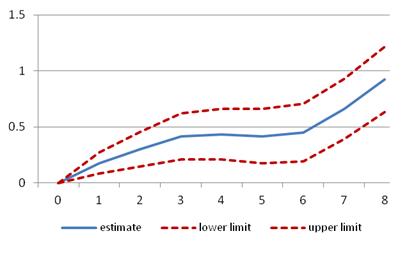

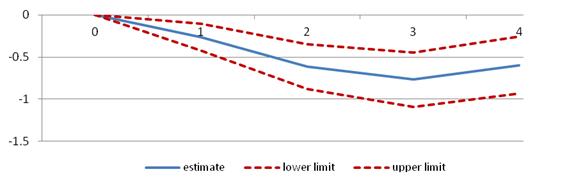

Fiscal tightening, whether based on cutting spending or raising taxes, has raised inequality and lowered the wage share of income. These are the main findings of my co-authored IMF working paper released today. The results are based on 173 episodes of fiscal consolidation during 1978-2009 for 17 OECD economies (Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, Portugal, Spain, Sweden, the United Kingdom, and the United States). Some of the key charts from the paper are given below.

Fiscal consolidation raises inequality (as measured by the Gini Coefficient)

(The horizontal axis shows the year of the consolidation—year 0—and the impact up to 8 years after the consolidation)

Consolidation based on spending cuts raises inequality …

… as does consolidation based on tax increases

Fiscal consolidation lowers the wage share of income

Fiscal tightening, whether based on cutting spending or raising taxes, has raised inequality and lowered the wage share of income. These are the main findings of my co-authored IMF working paper released today. The results are based on 173 episodes of fiscal consolidation during 1978-2009 for 17 OECD economies (Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, Portugal, Spain, Sweden, the United Kingdom, and the United States). Some of the key charts from the paper are given below.

Posted by at 7:07 PM

Labels: Inclusive Growth

Wednesday, June 19, 2013

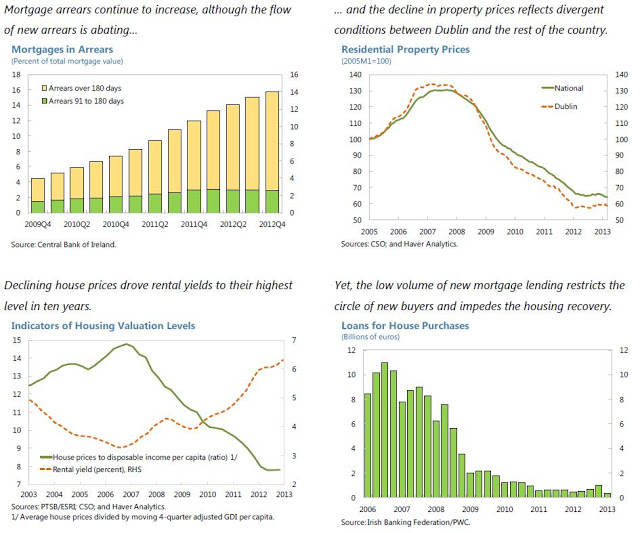

House Prices in Ireland

“House prices slipped back reflecting developments outside Dublin. After stabilizing over much of 2012, national residential property prices fell 2.6 percent in the first quarter of 2013, bringing the index to a new low 51 percent below its pre-crisis peak,” according a new IMF report on Ireland. What explains the drop in prices? The report says that “this decline was driven by an almost 4 percent price fall outside Dublin, reflecting divergent market conditions—the stock of property available for sale in Dublin amounts to around 6 months‘ supply, Read the full article…

Posted by at 4:49 PM

Labels: Global Housing Watch

Monday, June 17, 2013

MAULDIN: Economists Are Totally Clueless About The Economy

“In November of 2008, as stock markets crashed around the world, the Queen of England visited the London School of Economics to open the New Academic Building. While she was there, she listened in on academic lectures. The Queen, who studiously avoids controversy and almost never lets people know what she’s actually thinking, finally asked a simple question about the financial crisis: “How come nobody could foresee it?” No one could answer her.”

“If you’ve suspected all along that economists are useless at the job of forecasting, you would be right. Dozens of studies show that economists are completely incapable of forecasting recessions. But forget forecasting. What’s worse is that they fail miserably even at understanding where the economy is today. In one of the broadest studies of whether economists can predict recessions and financial crises, Prakash Loungani of the International Monetary Fund wrote very starkly, “The record of failure to predict recessions is virtually unblemished.” He found this to be true not only for official organizations like the IMF, the World Bank, and government agencies but for private forecasters as well. They’re all terrible. Loungani concluded that the “inability to predict recessions is a ubiquitous feature of growth forecasts.” Most economists were not even able to recognize recessions once they had already started.” Read the full article here.

“In November of 2008, as stock markets crashed around the world, the Queen of England visited the London School of Economics to open the New Academic Building. While she was there, she listened in on academic lectures. The Queen, who studiously avoids controversy and almost never lets people know what she’s actually thinking, finally asked a simple question about the financial crisis: “How come nobody could foresee it?”

Posted by at 6:43 PM

Labels: Forecasting Forum

Subscribe to: Posts