Tuesday, September 10, 2013

Okun’s Not Broken: Jobs and Growth are Still Linked

I sound like a broken record (young people will not know how a broken record sounds, let alone what a ‘record’ is) but I gave a talk at the New School for Social Research today on how jobs and growth are linked in many countries across the globe. On a personal note: It was difficult not to ‘feel verklempt’ giving a talk at New School–Robert’s Heilbroner’s “The Wordly’s Philosophers” is probably why I became an economist.

I sound like a broken record (young people will not know how a broken record sounds, let alone what a ‘record’ is) but I gave a talk at the New School for Social Research today on how jobs and growth are linked in many countries across the globe. On a personal note: It was difficult not to ‘feel verklempt’ giving a talk at New School–Robert’s Heilbroner’s “The Wordly’s Philosophers” is probably why I became an economist. Read the full article…

Posted by at 8:00 PM

Labels: Inclusive Growth

“Austerity” and Inequality: Engaging UNICEF

In my presentation at UNICEF today I spoke about the impacts of fiscal consolidation (often called “austerity” in the blogosphere) on long-term unemployment, labor’s share of income, and inequality.

Here’s a link to the paper.

|

| The announcement |

|

| The view from the UNICEF conference room |

In my presentation at UNICEF today I spoke about the impacts of fiscal consolidation (often called “austerity” in the blogosphere) on long-term unemployment, labor’s share of income, and inequality.

Here’s a link to the paper.

The announcement

The view from the UNICEF conference room Read the full article…

Posted by at 7:33 PM

Labels: Inclusive Growth

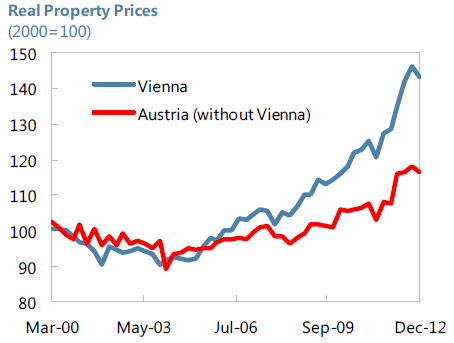

House Prices in Austria

“The housing market has experienced strong price growth but from low levels. In nominal terms at end-2012, house prices rose 14.9 percent y-o-y in Vienna compared with 11.5 percent y-o-y for Austria overall. In real terms and from a medium-term perspective, the price increase appears more modest: a cumulative 40 percent over 10 years in Vienna and about 5 percent in the rest of Austria. Housing market activity seems to be driven largely by non-resident buyers and domestic investors seeking an alternative to low fixed-income returns, though continued immigration also likely supported demand for housing in urban areas. Mortgage credit has exhibited slow growth, suggesting the prevalence of equity buyers,” according to the IMF’s annual report on Austria.

“The housing market has experienced strong price growth but from low levels. In nominal terms at end-2012, house prices rose 14.9 percent y-o-y in Vienna compared with 11.5 percent y-o-y for Austria overall. In real terms and from a medium-term perspective, the price increase appears more modest: a cumulative 40 percent over 10 years in Vienna and about 5 percent in the rest of Austria. Housing market activity seems to be driven largely by non-resident buyers and domestic investors seeking an alternative to low fixed-income returns,

Posted by at 4:01 PM

Labels: Global Housing Watch

Friday, September 6, 2013

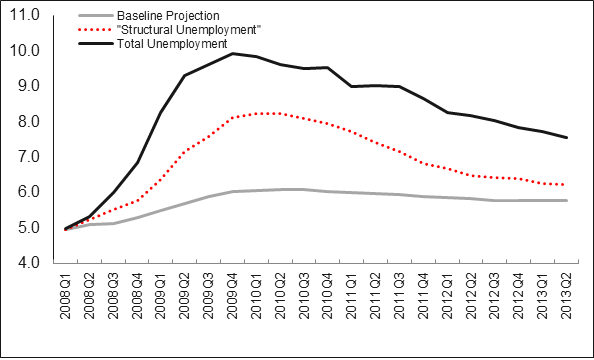

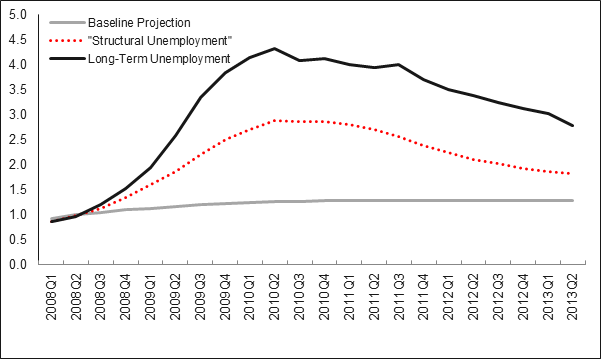

U.S. “Structural” Unemployment: Updated Estimates

Each release of the U.S. payroll employment report leads to a debate on the extent to which unemployment is cyclical vs. structural. I’ve just updated the estimates of U.S. structural unemployment reported in my 2011 IMF Working Paper. (Please note that IMF working papers represent the views of the authors and not the official view of the IMF or of any institution with which my co-authors are affiliated.)

The bottom line? The estimate of structural unemployment has declined over the past year in line with the decline in the actual unemployment rate. In the figure below, the solid (black) line shows the U.S. unemployment rate declining from nearly 10 percent in 2009:Q4 to about 7 ½ percent today. The dotted (red) line is the estimate of structural unemployment; it too has declined over that time and the latest estimate of structural unemployment is 6.2 percent. There is a lot of concern about U.S. long-term unemployment. In this case too, there has been a decline in the estimate of the structural component of long-term unemployment, but it is more gradual than in the case of total unemployment.

Intrigued? This post by Menzie Chinn (Econbrowser) has a nice ‘cheat sheet’ on how these estimates were constructed.

Each release of the U.S. payroll employment report leads to a debate on the extent to which unemployment is cyclical vs. structural. I’ve just updated the estimates of U.S. structural unemployment reported in my 2011 IMF Working Paper. (Please note that IMF working papers represent the views of the authors and not the official view of the IMF or of any institution with which my co-authors are affiliated.)

Estimate of Structural Unemployment, Read the full article…

Posted by at 10:34 AM

Labels: Inclusive Growth

Thursday, September 5, 2013

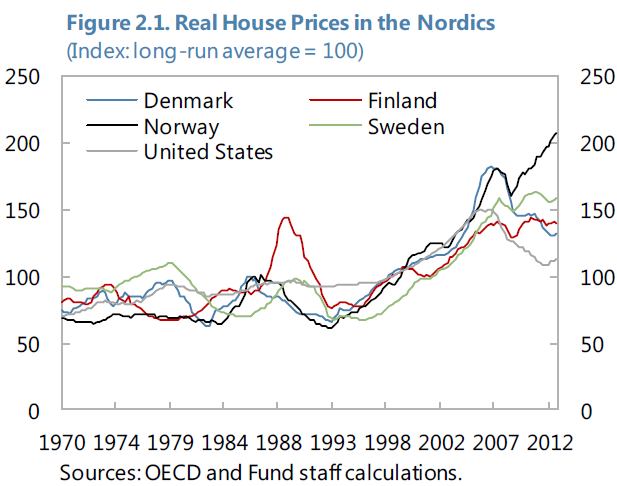

House Prices in the Nordics

“House prices in the Nordic-4 [Denmark, Finland, Norway, and Sweden] rose in tandem from the mid-1990s until the recent peaks in 2007 but diverged afterwards. House prices increased by more than 120 percent on average in the Nordic countries between 1995 and 2007 (see Figure 2.1). Since 2007 peaks, house price co-movements seem to have dissipated. The real house price in Norway increased by more than 10 percent relative to the 2007 peak level, while house prices fell by close to 30 percent in Denmark. In Finland and Sweden, house prices have remained broadly constant around 2007 levels,” according to an IMF report on the Nordic Region.

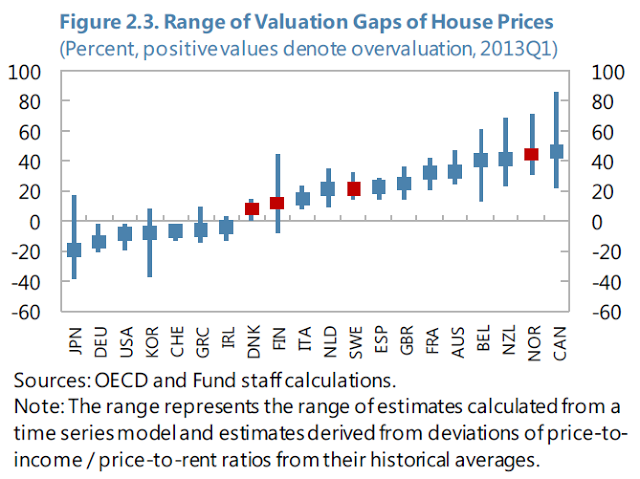

“The estimates suggest house prices are overvalued in the Nordic-4, but the extent of overvaluation varies (see Figure 2.3). The chart shows both the range and the mean of house price gaps based on the three different measures discussed above [(i) a time-series model; (ii) deviations from a long-run price-to-income ratio; and (iii) deviations from a long-run price-to-rent ratio]. The average estimate of the valuation gap for Norway is just over 40 percent while the estimated valuation gap is less than 10 percent in Denmark. Average estimates for Finland and Sweden suggest that house prices are moderately overvalued, by 12 and 22 percent, respectively.”

“House prices in the Nordic-4 [Denmark, Finland, Norway, and Sweden] rose in tandem from the mid-1990s until the recent peaks in 2007 but diverged afterwards. House prices increased by more than 120 percent on average in the Nordic countries between 1995 and 2007 (see Figure 2.1). Since 2007 peaks, house price co-movements seem to have dissipated. The real house price in Norway increased by more than 10 percent relative to the 2007 peak level, while house prices fell by close to 30 percent in Denmark. In Finland and Sweden,

Posted by at 7:40 PM

Labels: Global Housing Watch

Subscribe to: Posts