Thursday, September 5, 2013

House Prices in Sweden

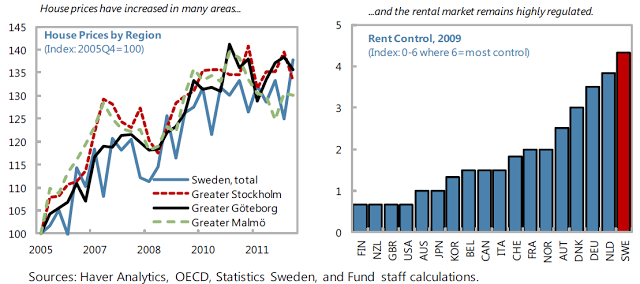

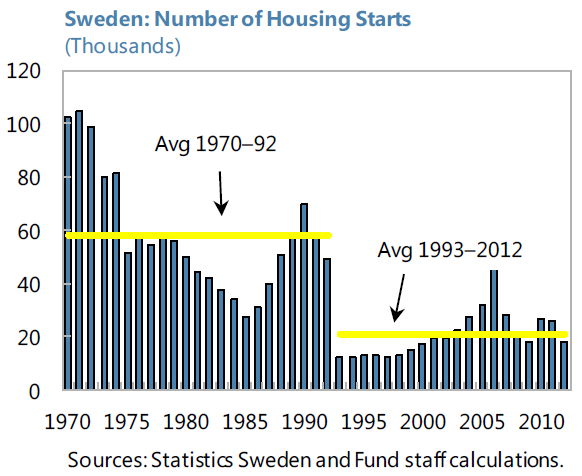

“Swedish house prices are potentially overvalued by more than 15 percent. House prices have more than doubled since the mid-1990s, increasing by about 140 percent in real terms between 1995 and 2007 and remaining broadly stable since then. Current estimates suggest that house prices are overvalued by 15 to 18 percent, accounting for rental regulations,” the IMF said in its latest annual report on Sweden.

“Swedish house prices are potentially overvalued by more than 15 percent. House prices have more than doubled since the mid-1990s, increasing by about 140 percent in real terms between 1995 and 2007 and remaining broadly stable since then. Current estimates suggest that house prices are overvalued by 15 to 18 percent, accounting for rental regulations,” the IMF said in its latest annual report on Sweden.

Posted by at 7:39 PM

Labels: Global Housing Watch

House Prices in Norway

“House prices continue to rise in Norway. There was only a brief correction at the time of the global financial crisis. Real house prices increased by nearly 30 percent from its lowest level in 2008. Standard affordability indicators are also worsening. Price-to-income and price-to-rent ratios increased by 14 percent and 23 percent, respectively, from their lowest levels in 2008. Several factors have been identified to explain the upward trend of house prices, including robust income growth and high population growth due to immigration (see Box 2.1). While these factors may partly explain recent house price developments, there are also risks associated with a house price reversal, and household would be vulnerable to house price corrections given the high levels of household debt,” according to a new report by the IMF.

“House prices continue to rise in Norway. There was only a brief correction at the time of the global financial crisis. Real house prices increased by nearly 30 percent from its lowest level in 2008. Standard affordability indicators are also worsening. Price-to-income and price-to-rent ratios increased by 14 percent and 23 percent, respectively, from their lowest levels in 2008. Several factors have been identified to explain the upward trend of house prices, including robust income growth and high population growth due to immigration (see Box 2.1).

Posted by at 7:39 PM

Labels: Global Housing Watch

Wednesday, September 4, 2013

A Marxist theory is (sort of) right

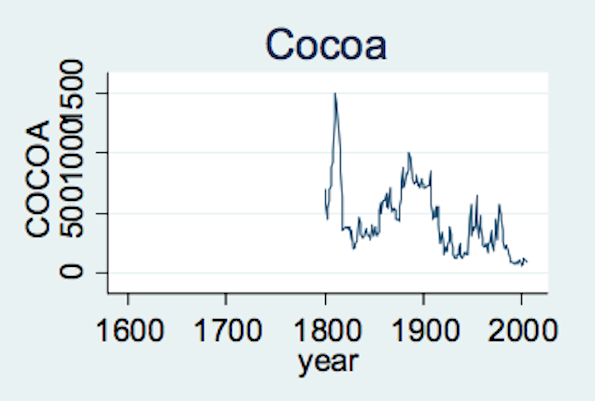

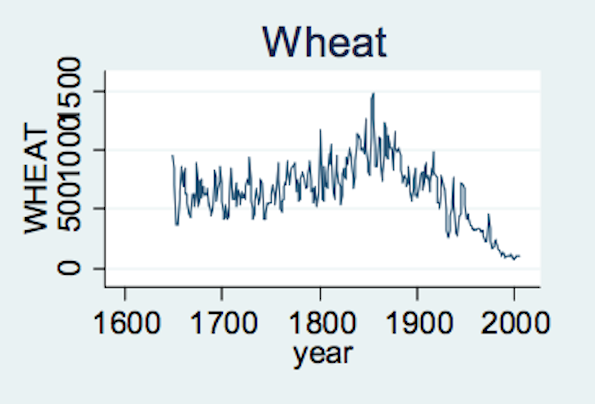

THE Prebisch-Singer hypothesis (PSH) was a staple of leftist economics during the second half of the 20th century. Raúl Prebisch and Hans Singer, working independently, showed that the “terms of trade” between primary products and manufactured goods tended to decline over time. In other words, producers of crops and raw materials gradually became poorer relative to producers of cars and household appliances. If true, the theory would have important implications for world trade; it would suggest that commodity-focused economies must diversify into other sectors or risk falling ever further behind richer countries.

A new paper* by the International Monetary Fund discusses the PSH. The authors examine 25 commodities, from sugar to silver, with some data going back to 1650. Since 1900, around 50% of the commodities show clear downward relative price slopes. About 25% show a clear upward slope. You will have to forgive the confusing labelling of the graphs, but you get the idea:

These graphs show prices relative to manufactured goods; in dollar terms many commodity prices have trended upward over the past century. So countries that produce high levels of primary products have, over time, done worse than economies which rely on manufactured goods. The authors cautiously conclude that “in the majority of cases the PSH is not rejected”.

What can primary producers do about this? In a recent conference at the IMF in Washington, one of the authors, Kaddour Hadri, suggested that commodity-dependent economies should take advantage of short periods of price spikes to invest in alternative industries. But many commodity-dependent economies fail to do this. William Sawyer, of Texas Christian University, argues that South America has failed to take advantage of high commodity prices over the past decade. As a result, their economies are not well-equipped to deal with the current price declines.

But according to Javier Blas, a journalist for the Financial Times who spoke at the IMF conference, commodity producers have been fighting against the Prebisch-Singer hypothesis for the last century. Many have shifted production away from commodities which do relatively badly against manufactured goods. The development of the soybean market, as well as shifts towards farming of chicken and pork, are some examples of this. None of these commodities appears in the IMF paper, so it does not tell a complete story. Still, and oddly enough, the IMF seems to have turned up some evidence support a bit of Marxist economic theory.

*Rabah Arezki, Kaddour Hadri, Prakash Loungani and Yao Rao (2013) ‘Testing the Prebisch-Singer Hypothesis since 1650: Evidence from Panel Techniques that Allow for Multiple Breaks’ Working Paper No. 13/180

From the Economist:

THE Prebisch-Singer hypothesis (PSH) was a staple of leftist economics during the second half of the 20th century. Raúl Prebisch and Hans Singer, working independently, showed that the “terms of trade” between primary products and manufactured goods tended to decline over time. In other words, producers of crops and raw materials gradually became poorer relative to producers of cars and household appliances. If true, the theory would have important implications for world trade;

Posted by at 11:33 AM

Labels: Energy & Climate Change

Thursday, August 29, 2013

Stan Fischer: A Class Act

In 2012, the magazine Global Finance gave Stanley Fischer, then central bank governor of Israel, an A for his handling of the economy during the financial crisis. It was the fourth year in a row that Fischer had received an A. It’s a grade the former professor—who taught both Federal Reserve Board Chairman Ben Bernanke and European Central Bank (ECB) President Mario Draghi—cherishes: “Those were some tough tests we faced in Israel.”

Fischer stepped down as central bank governor in June this year after eight years in the job, bringing the curtain down on an extraordinary third act of his career. The second act was as the IMF’s second-in-command during the tumultuous period of financial crises in emerging markets from 1994 to 2001. This role as policymaker came after a rousing opening act in the 1970s and 1980s, during which Fischer established himself as a preeminent macroeconomist, one who defined the contours of the field through his scholarly work and textbooks. It speaks to Fischer’s success that stints as the World Bank’s chief economist in the 1980s and as vice chairman at Citigroup in the 2000s—which would be crowning achievements of many a career—come across as interludes between the main acts. For the full profile, continue reading here.

In 2012, the magazine Global Finance gave Stanley Fischer, then central bank governor of Israel, an A for his handling of the economy during the financial crisis. It was the fourth year in a row that Fischer had received an A. It’s a grade the former professor—who taught both Federal Reserve Board Chairman Ben Bernanke and European Central Bank (ECB) President Mario Draghi—cherishes: “Those were some tough tests we faced in Israel.”

Fischer stepped down as central bank governor in June this year after eight years in the job,

Posted by at 9:54 PM

Labels: Profiles of Economists

Wednesday, August 28, 2013

Florida vs. Spain: Labor Mobility within Currency Unions

Paul Krugman has blogged extensively on how states within the US currency union have adjusted better than regions and countries within the European currency unions. My presentation at the European Regional Science Association today gives some background on this discussion and some new results.

Paul Krugman has blogged extensively on how states within the US currency union have adjusted better than regions and countries within the European currency unions. My presentation at the European Regional Science Association today gives some background on this discussion and some new results.

Posted by at 11:14 AM

Labels: Inclusive Growth

Subscribe to: Posts