Monday, December 12, 2011

GLOBAL HOUSE PRICE MONITOR

Do house prices have more room to fall?

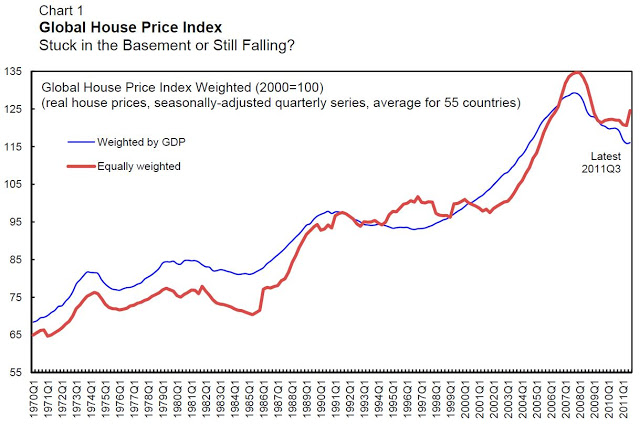

Globally, house prices remain in the doldrums, according to just-released data for 2011:Q3. After a decade of boom, the global house price index peaked in 2007:Q4 and since then has been falling or at best stuck in the basement.

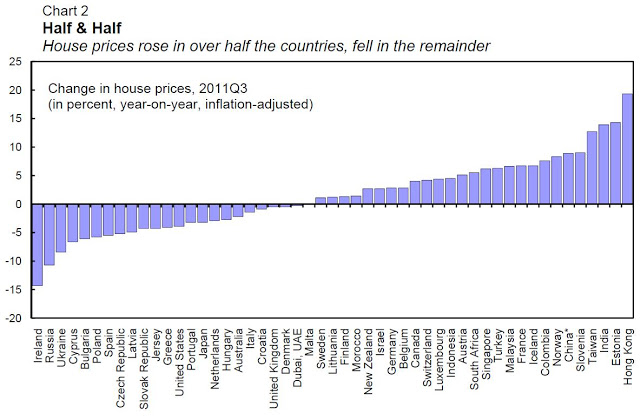

Looking behind the global index, however, reveals the inequality across countries. It’s not quite the 99% vs. the 1%, but more like 50-50: house prices have fallen over the past year in about half the countries and risen in the other half.

More Room to Fall?

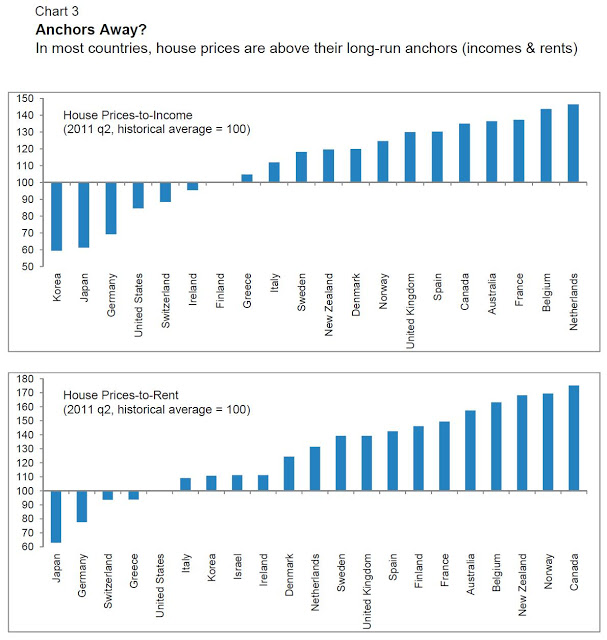

Many factors drive house prices (see: Housing Prices: More Room to Fall? and IMF Research Bulletin article: Seven questions about house price cycles) making it difficult to predict their future course. Two indicators that economists use to predict the direction of change in house prices are the ratio of house prices to income and the ratio of house prices to rents. If these two ratios are above their historical averages, economic theory suggests that declines in house prices may still be in the offing.

How do these indicators look with the latest data on house prices? For all but a handful of countries, these ratios remain above, and in many cases well above, their historical averages, signaling that there may be room to fall.

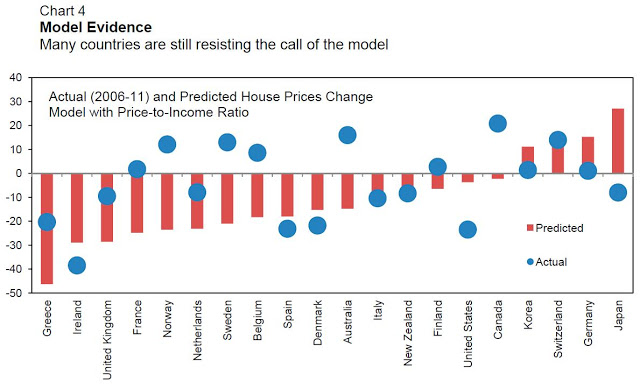

An econometric model of the determinants of house prices, used in the World Economic Outlook (see: House Prices: Corrections and Consequences, and updated here and here ), paints a somewhat different picture. The model explains house price growth based on several short-run momentum factors, such as growth in incomes, asset prices and population, and long-run factors, such as the house price to income ratio. The difference between house prices and those predicted on the basis on these ‘fundamental’ factors gives an indication of whether there is room to fall. The results from this exercise show that in many countries the declines in house prices over the past five years (the ‘actual’) are close to, or even exceed, what was predicted by the model. But for many countries, house prices are still resisting the predictions of the model.

‘This Country is Different’

The indicators presented above are very broad brush. At any time, there are myriad country-specific factors that influence house prices. IMF staff reports for countries often delve into these factors in much detail. Readers interested in developments in house prices in particular countries would be well served by consulting these documents. Links to some recent reports that have featured house price developments are given below.

|

Country

|

Link to report

|

Pages

|

Date

|

|

Australia

|

8

|

Oct-11

|

|

|

Canada

|

30, 36

|

Dec-10

|

|

|

Canada

|

3 to 16

|

Dec-10

|

|

|

China

|

9 to 10

|

Jul-11

|

|

|

Denmark

|

3, 9

|

Dec-10

|

|

|

France

|

24 to 26, 30

|

Jul-11

|

|

|

Korea

|

7, 25

|

Aug-11

|

|

|

Netherlands

|

1, 18, 27

|

Jun-11

|

|

|

Netherlands

|

47 to 55

|

Jun-11

|

|

|

Spain

|

9

|

Jul-11

|

|

|

Sweden

|

9 to 10

|

Jul-11

|

|

|

Switzerland

|

8

|

May-11

|

|

|

United Kingdom

|

8, 10, 30

|

Aug-11

|

|

|

United States

|

19 to 22, 47

|

Jul-11

|

|

|

United States

|

4 to 13

|

Jul-11

|

Also, see two powerpoint presentations on A look at housing prices around the world and Policy Options to Deal With Real Estate Booms.

Do house prices have more room to fall?

Globally, house prices remain in the doldrums, according to just-released data for 2011:Q3. After a decade of boom, the global house price index peaked in 2007:Q4 and since then has been falling or at best stuck in the basement.

Looking behind the global index, however, reveals the inequality across countries. It’s not quite the 99% vs.

Posted by at 4:41 PM

Labels: Global Housing Watch

Tuesday, November 29, 2011

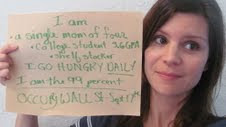

How does Fiscal Austerity affect the 99% vs. the 1%?

During times of fiscal austerity, income inequality goes up. Inequality goes up more when the austerity comes about through spending cuts than through tax hikes. The income share of the richest 1% of the population increases after fiscal austerity. Those are the main findings of a new paper by Luca Agnello and Ricardo Sousa.

The paper adds to a growing, but still scant, literature on how fiscal austerity affects different segments of the population. My paper with Larry Ball of Johns Hopkins University and my IMF colleague Daniel Leigh [available here] shows that fiscal austerity lowers incomes—hitting wage-earners more than others—and raises unemployment, particularly long-term unemployment. These costs must be balanced against the potential longer-term benefits that consolidation can confer.

Agnello and Sousa note that their results are “close in spirit” to the evidence of Ball, Leigh and Loungani that “fiscal consolidation reduces the wage share in total income. The authors suggest that, while the fall in wage income is persistent, the fall in capital and property income is short-lived. This can be explained by the fact that fiscal austerity plans typically call for a fall in public sector wages or lead to an increase in unemployment (in particular, long-term unemployment)” (p. 10, Agnello and Sousa).

During times of fiscal austerity, income inequality goes up. Inequality goes up more when the austerity comes about through spending cuts than through tax hikes. The income share of the richest 1% of the population increases after fiscal austerity. Those are the main findings of a new paper by Luca Agnello and Ricardo Sousa.

The paper adds to a growing, but still scant, literature on how fiscal austerity affects different segments of the population.

Posted by at 11:19 AM

Labels: Inclusive Growth

Monday, November 7, 2011

IMF Book Forum on “Lost Decades: The Making of America’s Debt Crisis and the Long Recovery”

The talents of Menzie Chinn and Jeffry Frieden—a leading international economist and political scientist, respectively—have come together in a nice way in a new book on the U.S. financial crisis and the prospects for the country. The title of the book (“Lost Decades”) gives away what the authors think will happen.

A standing-room only audience at the IMF last month heard a presentation by Chinn and Frieden, along with comments from Diane Lim Rogers (Concord Coalition), Gail Cohen (Joint Economic Committee) and Simon Johnson (MIT and Peterson Institute). The forum was moderated by Nobel Prize-winner George Akerlof.

Two features of the book make it different from the many books on the crisis. The first is the authors’ position that this financial crisis was a typical foreign capital flow cycle in which money flowed in from abroad and was not used productively. In this respect, they say, the U.S. proved to be no different from Argentina in the 1990s or the U.S. in the 1880s.

The second distinctive feature is the book’s focus on the political tussle over who bears the costs of resolving the crisis. When “we turn to political economy,” Frieden quipped, “we’ll see that political economy is the truly dismal science.”

Frieden recalled that in 1985 the military dictator of Brazil made a famous speech in which he said Brazilians have to realize that the party is over. The next day on the streets of Sao Paolo and Rio, there were mass demonstrations and the banners read, “The party is over and we weren’t even invited.”

Frieden said that the demonstrations in the U.S. reflect the growing realization that “the benefits of the party [during the 2000s] were not equally shared while the burden is being unequally distributed.” Over the 2000-07 period, Frieden said, the top one percent of the U.S. population saw its income grow by 60 percent. But the bottom 99 percent of the population had income gains of only 6 percent and “of course that six percent [was] eaten away by the crisis.”

This was a theme picked up by Cohen in her remarks. “What I’m really concerned about,” she said, is that the lost decades that Chinn and Frieden fear “will only be for some segments of the population and that some people will do fine.” Simon Johnson concurred, noting that for some people decades have already been lost: “This is a continuation of losses.”

Cohen noted that long-term unemployment is at historically high levels: half of those unemployed have been out of work for over six months. African-American workers have been disproportionately hit, as have younger workers. The unemployment rate for younger workers is 20 percent. Her examples of the unequal distribution of pain supported Frieden’s assertion that some segments of the populations are “really almost at Depression levels of unemployment and underemployment.”

During the Q&A, the IMF’s Steve Phillips questioned the book’s focus on the international nature of the capital flows. Chinn and Frieden emphasize the “international aspects,” he said, “but you couldn’t have had the bubble without lax regulation. But you could have had a bubble and you could have had the crisis without international capital flows.” In his view, therefore, “the prerequisite was lax regulation.”

In response, Chinn acknowledged that it was difficult to distinguish between a capital flow boom-bust cycle and a credit boom-bust cycle and also agreed that the U.S. had “essentially disarmed ourselves in terms of regulation.” Nevertheless, he defended the book’s focus, saying that “it’s hard for me to think about a boom that doesn’t have some component of savings coming in from the rest of the world.”

The wisdom of the Bush tax cuts of 2001 and 2003 also generated some back-and-forth. In commenting on the book, Diane Lim Rogers noted that she and Menzie Chinn had “worked together at the end of the Clinton Administration on the Council of Economic Advisors and ever since then I became obsessed with the Bush tax cuts and the fiscal irresponsibility of them.”

Taking some issue with this, noted commentator Bruce Bartlett said that with hindsight it is easy to blame the tax cuts or other policy actions, but the main driving force behind the overborrowing was that “we had this huge increase in world saving that had to go somewhere … Even if [the U.S.] had kept the budget balanced, the money would have flowed into something else … Absent capital controls, what could we have done to keep the money out?”

Liaquat Ahamed, author of the 2010 Pulitzer Prize-winning book Lords of Finance, asked whether the debate over the short-run impacts of fiscal policy is really “a disagreement about how the economy actually works?” Frieden responded that “I think the conflicts here are not ideological and they’re not really theoretical … They’re really about who is going to pay the price.”

Event’s transcript and webcast.

The IMF Book Forum was launched in September 2003. Over the years, it has featured nearly 30 books on international economics, political economy, and business cycle analysis.

|

| Photos: Michael Spilotro/IMF |

The talents of Menzie Chinn and Jeffry Frieden—a leading international economist and political scientist, respectively—have come together in a nice way in a new book on the U.S. financial crisis and the prospects for the country. The title of the book (“Lost Decades”) gives away what the authors think will happen.

A standing-room only audience at the IMF last month heard a presentation by Chinn and Frieden, along with comments from Diane Lim Rogers (Concord Coalition),

Friday, November 4, 2011

What’s the Secret to Economic Growth? We Just Don’t Know

Via Bloomberg Businessweek. Charles Kenny writes “You would think that, armed with so much learning, their powerful models, and reams of data, economists would have anticipated that the recovery in the U.S. and Europe would stall, that growth in such places as China, India, and Brazil would accelerate, and that poverty rates would plummet in Africa. You’d be wrong.

A few years ago, Prakash Loungani of the IMF looked at the accuracy of short-term economic growth forecasts by industry experts across a range of countries. Sixty recessions occurred in the countries he studied during the period covered by the forecasts. A grand total of two of those 60 were predicted by forecasters a year before they happened—which means the other 58 took economists by surprise. Two-thirds of all recessions remained unpredicted by April of the year in which they occurred. “The record of failure to predict recessions is virtually unblemished,” Loungani concluded.

So don’t put too much credence in predictions either of a double-dip recession or of an economic recovery in the U.S. over the next 18 months. We just don’t know. Pretty much the only safe bet is that something will happen.

Loungani’s study was relatively limited in scope: It looked at economists’ attempts to predict economic shifts a year or two out in a set of largely advanced countries. Imagine the much larger challenge of predicting longer-term growth outcomes in a wider range of countries—not just rich ones, but also the Nigerias and Vietnams of the world. In fact, there’s no need to imagine: We are awful at it.”

Kenny is a fellow at Center for Global Development and the New America Foundation.

Via Bloomberg Businessweek. Charles Kenny writes “You would think that, armed with so much learning, their powerful models, and reams of data, economists would have anticipated that the recovery in the U.S. and Europe would stall, that growth in such places as China, India, and Brazil would accelerate, and that poverty rates would plummet in Africa. You’d be wrong.

A few years ago, Prakash Loungani of the IMF looked at the accuracy of short-term economic growth forecasts by industry experts across a range of countries.

Posted by at 9:28 PM

Labels: Forecasting Forum

Monday, October 31, 2011

World of Work Report 2011: Making markets work for jobs

ILO says world heading for a new and deeper jobs recession, warns of more social unrest, in its annual World of Work Report.

ILO says world heading for a new and deeper jobs recession, warns of more social unrest, in its annual World of Work Report.

Posted by at 6:10 PM

Labels: Inclusive Growth

Subscribe to: Posts