Friday, February 28, 2020

House Prices in Malaysia

From the IMF’s latest report on Malaysia:

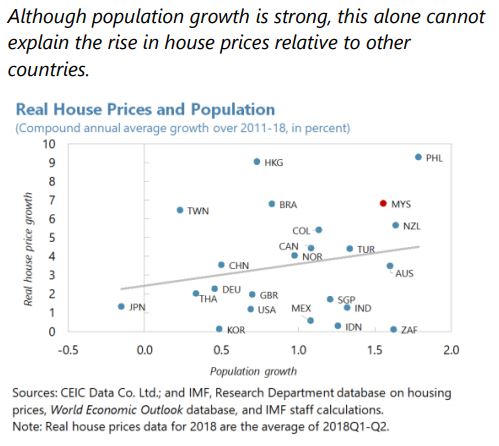

“Over the past decade, real house prices rose faster than income. House prices in Malaysia increased faster than in many regional comparators in the wake of the GFC (text chart). On average real house prices rose by 6 percent in Malaysia annually since 2010, compared with below one percent in regional comparators. At the same time, per capita income in Malaysia grew by around 4 percent annually leading to a deterioration in affordability over this time period (text chart).

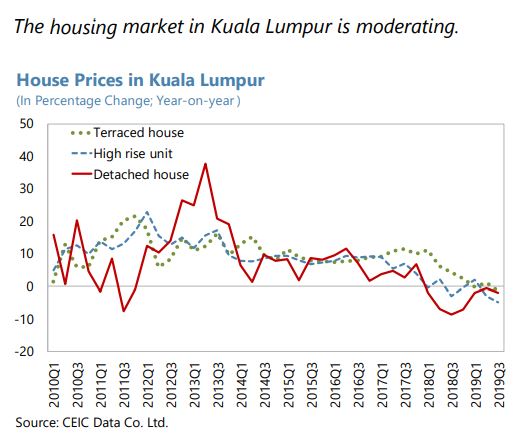

From 2015 onwards, house price growth has moderated from high levels. The average annual nominal house price increase during 2010-14 was 10 percent, but it has declined to an average of 5.5 percent during 2015-19. Most recently, preliminary data indicate that house prices increased by 0.4 percent in 2019Q3 (year-on-year) (text chart). The moderation in house price growth is broad-based across regions, including Kuala Lumpur (text chart).

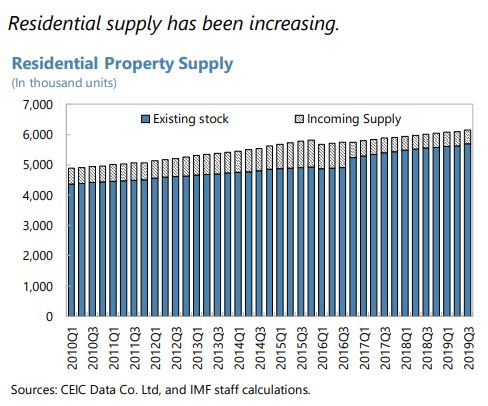

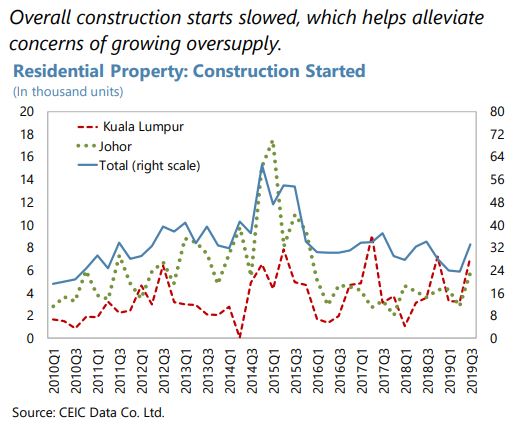

Residential housing supply has responded to higher prices with a lag. Supply factors are important determinants of housing market dynamics, especially considering that residential housing has long planning-to-production lags which can produce temporary supply and demand mismatches. In the aftermath of the GFC, residential property launches plummeted from a peak of nearly 350,000 units before the GFC to a lowest point of 173,000 in 2012 (text chart). The increase in house prices during 2010-15 triggered a strong supply response from 2015 onwards and currently housing starts are well above 300,000.

The strong supply response has led to overproduction in some segments of the market. Affordable housing in Malaysia is usually considered to be below RM300,000.2 Unsold properties in the upper segment (above RM500,000) has increased sharply in 2018-19, particularly in the high-rise apartment segments, whereas recent housing demand has been strong in the lower segments of the market as evidenced by the lower inventory of unsold housing units; unsold units above RM 1 million remain at a high level.

In contrast, there is an undersupply of housing at affordable levels, especially in urban areas. The deterioration of housing affordability can be illustrated in the house price-to-income ratio, which has increased from 4.1 in 2002 to 5.0 in 2016 (see Khazanah Research Institute, 2019). In addition, urban migration has increased housing demand in urban areas. The World Bank (2019) finds that households in Kuala Lumpur and Petaling District with monthly incomes below RM5,000 experience severe unaffordability, and can experience difficulty finding finance given low and often volatile income. Households with incomes from RM6,000-10,000 have moderate difficulty in purchasing a home, while those with incomes above RM10,000 find ample supply within their capacity-to-pay.

House prices are estimated to be moderately overvalued. Using an econometric model with fundamental determinants of house prices such as affordability, per capita income, interest rates, credit growth, working age population and equity share prices, suggest that real house prices remain about 15 percent above what fundamental macroeconomic variables would indicate (Box 1), although the overvaluation has slightly narrowed in recent years as house price increases have moderated.

Along with the increase in house prices, household debt has risen sharply over the past decade. Household debt increased from 60.4 percent of GDP in 2008 to 86.5 percent in 2016. Household debt has stabilized around 82 percent in 2019. Nevertheless, the level of household debt in Malaysia is relatively high by regional standards. Of the total household debt, around 54.5 percent is residential mortgages in 2019. Household debt by monthly income (as a share of total) has decreased for households making less than RM3,000, from 22.8 to 18.5 percent perhaps partly as a result of loan affordability assessments following the introduction of BNM’s Responsible Financing Guidelines in 2012.

High household debt raises financial stability risks, although households also hold substantial assets and non-performing loans are low. Although growth in household debt has moderated in recent years, some households could face increasing stress, particularly if they are over-extended from easier lending conditions in the past and severe income shocks could erode household financial buffers and impact spending (see Nordin et al 2018). Financial stability concerns relating to household debt are cushioned by high household assets (more than twice the debt) of which 2/3 are considered liquid. Moreover, household non-performing loans have declined and are somewhat below the banking sector average of 1.6 percent of total lending.

The concept of “House price at Risk” (HaR) can be used to obtain a measure of worst possible outcome for house prices over a given horizon. Following the approach in IMF (2019), a housing-at-risk approach quantifies the risk of negative house price growth 4-quarters ahead. Specifically, we use the explanatory variables in the econometric model discussed in the appendix to derive a distribution of projected real house price increases four quarters ahead. Using this approach suggests that the mode of house price increase will stabilize around 1.5 percent four quarters ahead (see text chart).”

Continue reading here.

From the IMF’s latest report on Malaysia:

“Over the past decade, real house prices rose faster than income. House prices in Malaysia increased faster than in many regional comparators in the wake of the GFC (text chart). On average real house prices rose by 6 percent in Malaysia annually since 2010, compared with below one percent in regional comparators. At the same time, per capita income in Malaysia grew by around 4 percent annually leading to a deterioration in affordability over this time period (text chart).

Posted by at 5:10 PM

Labels: Global Housing Watch

Foreign Demand and Local House Prices: Evidence from the US

A new IMF working paper by Damien Puy, Anil Ari, and Yu Shi:

“We test whether foreign demand matters for local house prices in the US using an identification strategy based on the existence of “home bias abroad” in international real estate markets. Following an extreme political crisis event abroad, a proxy for a strong and exogenous shift in foreign demand, we show that house prices rise disproportionately more in neighbourhoods with a high concentration of population originating from the crisis country. This effect is strong, persistent, and robust to the exclusion of major cities. We also show that areas that were already expensive in the late 1990s have experienced the strongest foreign demand shocks and the biggest drop in affordability between 2000 and 2017. Our findings suggest a non-trivial causal effect of foreign demand shocks on local house prices over the last 20 years, especially in neighbourhoods that were already rather unaffordable for the median household.”

A new IMF working paper by Damien Puy, Anil Ari, and Yu Shi:

“We test whether foreign demand matters for local house prices in the US using an identification strategy based on the existence of “home bias abroad” in international real estate markets. Following an extreme political crisis event abroad, a proxy for a strong and exogenous shift in foreign demand, we show that house prices rise disproportionately more in neighbourhoods with a high concentration of population originating from the crisis country.

Posted by at 5:04 PM

Labels: Global Housing Watch

Household Debt and House Prices-at-risk: A Tale of Two Countries

From a new IMF working paper by Adrian Alter and Elizabeth M. Mahoney:

“To identify and quantify downside risks to housing markets, we apply the house price-at-risk methodology to a sample of 37 cities across the United States and Canada using quarterly data from 1983 to 2018. This paper finds that downside risks to housing markets in the United States have seemingly fallen over the past decade, while having increased in Canada. Supply-side drivers, valuation, household debt, and financial conditions jointly play a key role in forecasting house price risks. In addition, capital flows are found to be significantly associated with future downside risks to major housing markets, but the net effect depends on the type of flows and varies across cities and forecast horizons. Using micro-level data, we identify households vulnerable to potential housing shocks and assess the riskiness of household debt.”

From a new IMF working paper by Adrian Alter and Elizabeth M. Mahoney:

“To identify and quantify downside risks to housing markets, we apply the house price-at-risk methodology to a sample of 37 cities across the United States and Canada using quarterly data from 1983 to 2018. This paper finds that downside risks to housing markets in the United States have seemingly fallen over the past decade, while having increased in Canada.

Posted by at 3:44 PM

Labels: Global Housing Watch

Economists should learn lessons from meteorologists

From the Financial Times:

“The UK’s national weather service, the Met Office, is to get a £1.2bn computer to help with its forecasting activities. That is a lot of silicon. My instinctive response was: when do we economists get one?

People may grumble about the weather forecast, but in many places we take its accuracy for granted. When we ask our phones about tomorrow’s weather, we act as though we are gazing through a window into the future. Nobody treats the latest forecasts from the Bank of England or the IMF as a window into anything.

That is partly because politics gets in the way. On the issue of Brexit, for example, extreme forecasts from partisans attracted attention, while independent mainstream forecasters have proved to be pretty much on the money. Few people stopped to praise the economic bean-counters.

Economists might also protest that nobody asks them to forecast economic activity tomorrow or even next week; they are asked to describe the prospects for the next year or so. True, some almanacs offer long-range weather forecasts based on methods that are secret, arcane, or both — but the professionals regard such attempts as laughable.

Enough excuses; economists deserve few prizes for prediction. Prakash Loungani of the IMF has conducted several reviews of mainstream forecasts, finding them dismally likely to miss recessions. Economists are not very good at seeing into the future — to the extent that most argue forecasting is simply none of their business. The weather forecasters are good, and getting better all the time. Could we economists do as well with a couple of billion dollars’ worth of kit, or is something else lacking?

The question seemed worth exploring to me, so I picked up Andrew Blum’s recent book, The Weather Machine, to understand what meteorologists actually do and how they do it. I realised quickly that a weather forecast is intimately connected to a map in a way that an economic forecast is not.”

Continue reading here.

From the Financial Times:

“The UK’s national weather service, the Met Office, is to get a £1.2bn computer to help with its forecasting activities. That is a lot of silicon. My instinctive response was: when do we economists get one?

People may grumble about the weather forecast, but in many places we take its accuracy for granted. When we ask our phones about tomorrow’s weather, we act as though we are gazing through a window into the future.

Posted by at 8:48 AM

Labels: Forecasting Forum

Housing View – February 28, 2020

On the US:

- ‘A Mask for Racial Discrimination.’ How Housing Voucher Programs Can Hurt the Low-Income Families They’re Designed to Help – Time

- Why Does It Cost $750,000 to Build Affordable Housing in San Francisco? – New York Times

- The Airbnb Effect On Housing And Rent – Forbes

- US housing finance is stuck in a complex knot of contradictions – Financial Times

- Housing regulations are getting in the way of fighting homelessness – Washington Post

- The declining elasticity of US housing supply – VOX

- Joe Biden wants tougher standards for real-estate appraisers to help black and Latinx homeowners – MarketWatch

- Special briefing on walkability – American Enterprise Institute

- Does Joe Biden Have a Plan to Stop Gentrification? – Citylab

On other countries:

- [China] History and Outlook of China’s Housing Market – SpringerLink

- [Netherlands] Dutch house price boom continues – Global Property Guide

- [New Zealand] New Zealand’s housing market bounced back strongly – Global Property Guide

- [United Kingdom] Housing insecurity, homelessness, and populism: Evidence from the UK – VOX

On the US:

- ‘A Mask for Racial Discrimination.’ How Housing Voucher Programs Can Hurt the Low-Income Families They’re Designed to Help – Time

- Why Does It Cost $750,000 to Build Affordable Housing in San Francisco? – New York Times

- The Airbnb Effect On Housing And Rent – Forbes

- US housing finance is stuck in a complex knot of contradictions – Financial Times

- Housing regulations are getting in the way of fighting homelessness – Washington Post

- The declining elasticity of US housing supply – VOX

- Joe Biden wants tougher standards for real-estate appraisers to help black and Latinx homeowners – MarketWatch

- Special briefing on walkability – American Enterprise Institute

- Does Joe Biden Have a Plan to Stop Gentrification?

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts