Friday, August 31, 2018

Housing View – August 31, 2018

On cross-country:

- Big City Housing Doesn’t Have to Be So Expensive – Bloomberg

- The Impact of Housing Costs on Regional Income Inequality – Federal Reserve Bank of St. Louis

- What Airbnb really does to a neighbourhood – BBC

On the US:

- Amazon HQ2: How did we get here? What comes next? – Brookings

- The Politics of Homeownership – Citylab

- The Trump Tax Cuts Were Supposed to Depress Housing Prices. They Haven’t. – New York Times

- Maybe we CAN build our way out of an urban housing shortage – Public Square

Photo by Aliis Sinisalu

On cross-country:

- Big City Housing Doesn’t Have to Be So Expensive – Bloomberg

- The Impact of Housing Costs on Regional Income Inequality – Federal Reserve Bank of St. Louis

- What Airbnb really does to a neighbourhood – BBC

On the US:

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, August 30, 2018

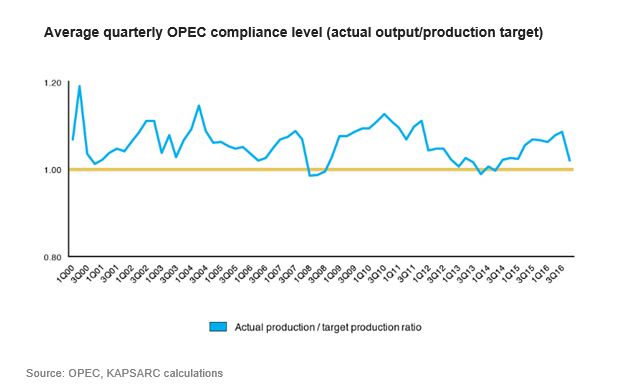

What Drives OPEC’s Quota Decisions?

A new paper from the King Abdullah Petroleum Studies and Research Center finds that:

“This paper identifies key determinants that appear to shape OPEC’s quota strategy and implementation. Using econometric estimations, it examines the factors that seem to most influence members’ adherence to their production commitments in the short term and what drives the organization’s quota decisions and level of compliance in the longer term

Key findings:

- Global oil market indicators such as oil price, global crude oil demand, six-month global demand projections, and the output of non-OPEC producers primarily drive OPEC’s quota decisions. Macroeconomic indicators, such as global gross domestic product growth and inflation, appear to play an insignificant role.

- The sampled OPEC member countries have different drivers of oil production. The output of the Gulf Cooperation Council countries and Iran is significantly affected by OPEC’s quotas and their reaction to the compliance levels of other OPEC members.

- The national oil production of Algeria, Nigeria and Venezuela appears to be primarily driven by a portfolio of economic, financial and political indices.

- Exogenous shocks impact OPEC quota levels and production. These mostly include country-specific shocks which can be external (e.g., sanctions) or domestic (crises, strikes or military conflicts). The impact of such events, however, is usually alleviated on the OPEC level, indicating the organization’s ability to balance its aggregate supply.”

A new paper from the King Abdullah Petroleum Studies and Research Center finds that:

“This paper identifies key determinants that appear to shape OPEC’s quota strategy and implementation. Using econometric estimations, it examines the factors that seem to most influence members’ adherence to their production commitments in the short term and what drives the organization’s quota decisions and level of compliance in the longer term

Key findings:

- Global oil market indicators such as oil price,

Posted by at 11:05 AM

Labels: Energy & Climate Change

Wednesday, August 29, 2018

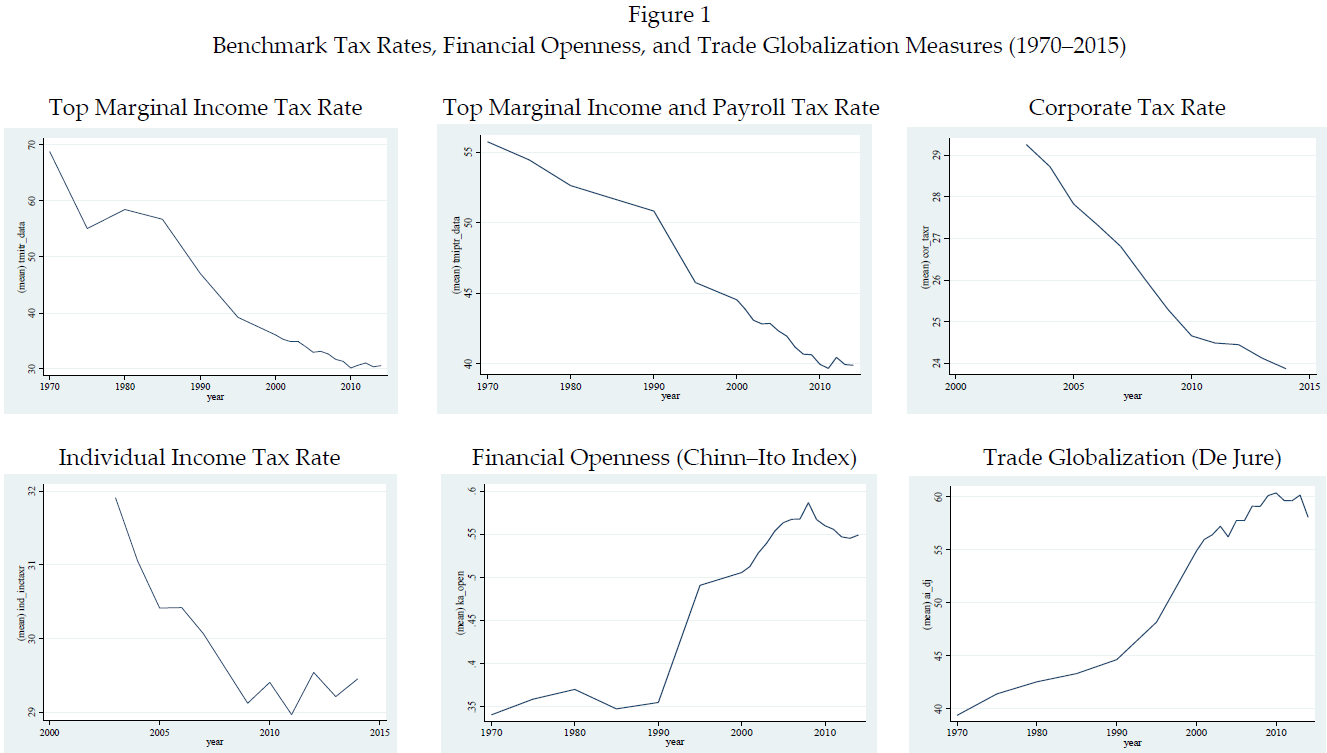

Does Globalization Lower Tax Rates?

From a new working paper by Priya Ranjan and Giray Gozgor:

“We construct a theoretical model to capture the compensation and efficiency effects of globalization in a set up where the redistributive tax rate is chosen by the median voter. The model predicts that the two alternative modes of globalization- trade liberalization and financial openness- could potentially have different effects on taxation. We then provide some empirical evidence on the relationship between taxation and the alternative modes of globalization using a large cross-country panel dataset. We make a distinction between de jure and de facto measures of globalization and find a robust negative relationship between de jure measures financial openness and tax rates. There is no robust relationship between de facto measures of finanical openness and taxation. As well, the relationship between trade liberalization (both de jure and de facto measures) and tax rates is not robust and depends on the measures of taxation as well as the time period of analysis.”

From a new working paper by Priya Ranjan and Giray Gozgor:

“We construct a theoretical model to capture the compensation and efficiency effects of globalization in a set up where the redistributive tax rate is chosen by the median voter. The model predicts that the two alternative modes of globalization- trade liberalization and financial openness- could potentially have different effects on taxation. We then provide some empirical evidence on the relationship between taxation and the alternative modes of globalization using a large cross-country panel dataset.

Posted by at 10:48 AM

Labels: Inclusive Growth

Monday, August 27, 2018

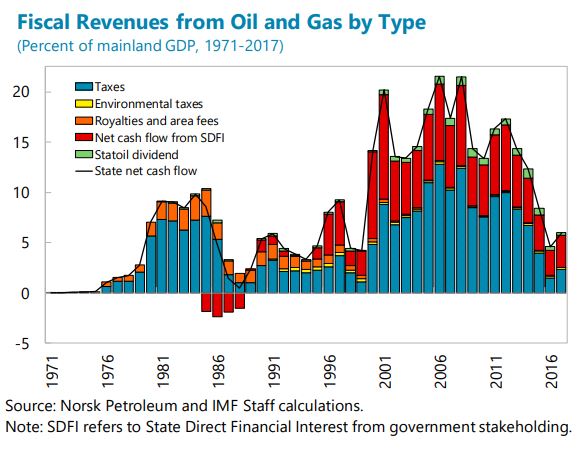

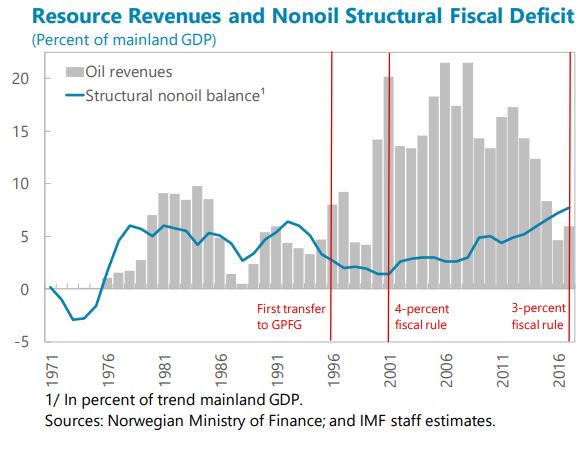

Counting the Oil Money and the Elderly: Norway’s Public Sector Balance Sheet

A new IMF working paper by Ezequiel Cabezon and Christian Henn says:

“Based on a permanent income analysis, Gagnon (2018) has prominently suggested that Norway has saved too much, thereby free-riding on the rest of the world for demand. Our public sector balance sheet analysis comes to the opposite conclusion, chiefly because it also accounts for future aging costs. Unsurprisingly, we find that Norway’s current assets exceed its liabilities by some 340 percent of mainland GDP. But its nonoil fiscal deficits have grown very large (to almost 8 percent of mainland GDP) and aging pressures are only commencing. Therefore, Norway’s intertemporal financial net worth (IFNW) is negative, at about -240 percent of mainland GDP. As IFNW represents an intertemporal budget constraint, this implies that Norway’s savings are likely insufficient to address aging costs without additional fiscal action.”

A new IMF working paper by Ezequiel Cabezon and Christian Henn says:

“Based on a permanent income analysis, Gagnon (2018) has prominently suggested that Norway has saved too much, thereby free-riding on the rest of the world for demand. Our public sector balance sheet analysis comes to the opposite conclusion, chiefly because it also accounts for future aging costs. Unsurprisingly, we find that Norway’s current assets exceed its liabilities by some 340 percent of mainland GDP.

Posted by at 1:50 PM

Labels: Global Housing Watch, Inclusive Growth

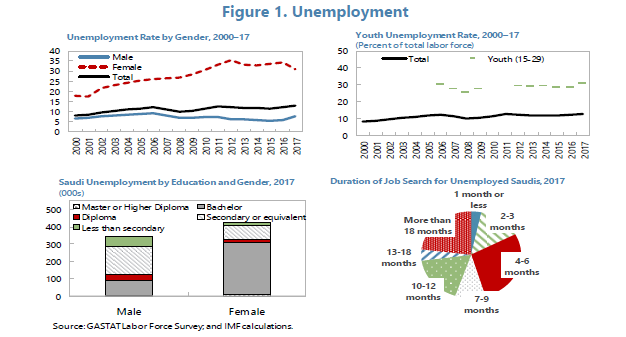

The Economic Impact of Policies to Boost the Employment of Saudi Nationals

A new IMF country report says that “Saudi Arabia’s labor market is characterized by a persistently high unemployment rate, low private employment ratio, and a low labor participation rate for nationals. The authorities are undertaking a wide range of labor market interventions to address these issues. The analysis in this paper shows that these interventions are helping to reduce distortions in the labor market, including by boosting female labor force participation and reducing the wage gap between expatriates and nationals in the private sector, but the impact on the rest of the economy is not always positive as firms adjust to the higher cost of labor. Reforms should therefore be gradual to minimize their impact on growth. A comprehensive set of policies is also needed to foster job creation for nationals. Measures should include policies toward levelling the playing field between national and expatriate workers so that employers have less of a preference for employing expatriates, setting clear expectations about the limited prospects for public sector employment, boosting female labor force participation, and strengthening education and training to support increased productivity of nationals.”

A new IMF country report says that “Saudi Arabia’s labor market is characterized by a persistently high unemployment rate, low private employment ratio, and a low labor participation rate for nationals. The authorities are undertaking a wide range of labor market interventions to address these issues. The analysis in this paper shows that these interventions are helping to reduce distortions in the labor market, including by boosting female labor force participation and reducing the wage gap between expatriates and nationals in the private sector,

Posted by at 9:51 AM

Labels: Inclusive Growth

Subscribe to: Posts