Tuesday, July 31, 2018

Happy 106th birthday on July 31, Milton Friedman!

From American Enterprise Institute (AEI):

“An important event takes place this week that is recognized annually on CD. Tuesday, July 31 is Milton Friedman’s birthday — he was born on that day in 1912 and would have been 106 years old this year. Unfortunately, Milton died on November 16, 2006, when he was 94 years old. In an editorial in the Wall Street Journal following Professor Friedman’s death, they reported his loss with the same tribute Milton used when Ronald Reagan died, saying “few people in human history have contributed more to the achievement of human freedom.” In honor of his legacy and birthday, here are 20 of my favorite Milton Friedman quotes, along with a bonus video and some special birthday graphics:

1. There is nothing as permanent as a temporary government program.

2. Many well-meaning people favor legal minimum-wage rates in the mistaken belief that they help the poor. These people confuse wage rates with wage income. It has always been a mystery to me to understand why a youngster is better off unemployed at $15 an hour than employed at $7.25 (updated). The rise in the legal minimum-wage rate is a monument to the power of superficial thinking.

3. First of all, the government doesn’t have any responsibility to the poor. People have responsibility. This building doesn’t have responsibility. You and I have responsibility. People have responsibility. Second, the question is how can we as people exercise our responsibility to our fellow man most effectively? That’s the problem. So far as poverty is concerned, there has never been a more effective machine for eliminating poverty than the free enterprise system and the free market. The period in which you had the greatest improvement in the lot of the ordinary man was the period of the 19th and early 20th century.

4. In the international trade area, the language is almost always about how we must export, and what’s really good is an industry that produces exports, and if we buy from abroad and import, that’s bad. But surely that’s upside-down. What we send abroad, we can’t eat, we can’t wear, we can’t use for our houses. On the other hand, the goods and services we import, they provide us with TV sets we can watch, with automobiles we can drive, with all sorts of nice things for us to use.”

Continue reading here.

From American Enterprise Institute (AEI):

“An important event takes place this week that is recognized annually on CD. Tuesday, July 31 is Milton Friedman’s birthday — he was born on that day in 1912 and would have been 106 years old this year. Unfortunately, Milton died on November 16, 2006, when he was 94 years old. In an editorial in the Wall Street Journal following Professor Friedman’s death,

Posted by at 10:08 AM

Labels: Profiles of Economists

Housing Price, Credit, and Output Cycles: How Domestic and External Shocks Impact Lithuania’s Credit

A new IMF working paper by Iacovos Ioannou says that:

“Lithuania’s current credit cycle highlights the strong link between housing prices and credit. We explore this relationship in more detail by analyzing the main features of credit, housing price, and output cycles in Baltic and Nordic countries during 1995–2017. We find a high degree of synchronization between Lithuania’s credit and housing price cycles. Panel regressions show a strong correlation between a credit upturn and housing price upturn. Moreover, panel VAR suggests that shocks in housing prices, credit, and output within and

outside Lithuania strongly impact Lithuania’s credit.”

A new IMF working paper by Iacovos Ioannou says that:

“Lithuania’s current credit cycle highlights the strong link between housing prices and credit. We explore this relationship in more detail by analyzing the main features of credit, housing price, and output cycles in Baltic and Nordic countries during 1995–2017. We find a high degree of synchronization between Lithuania’s credit and housing price cycles. Panel regressions show a strong correlation between a credit upturn and housing price upturn.

Posted by at 10:05 AM

Labels: Global Housing Watch

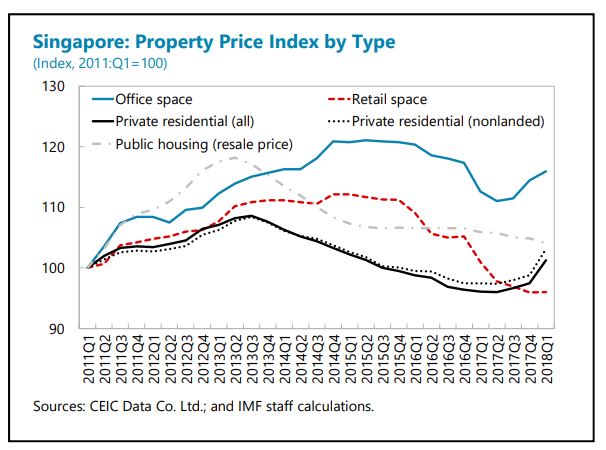

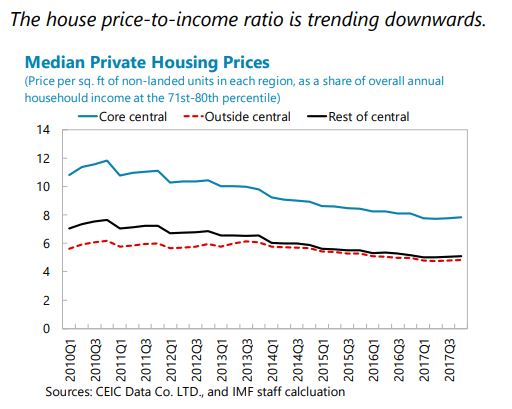

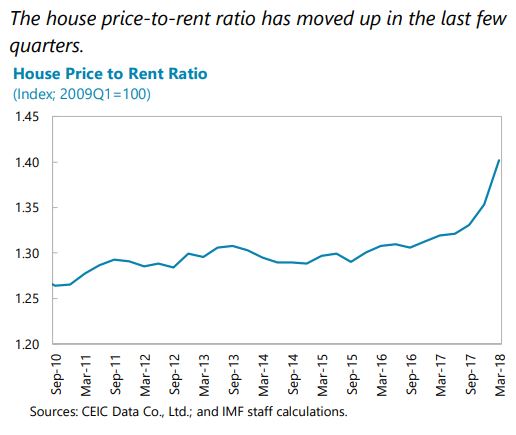

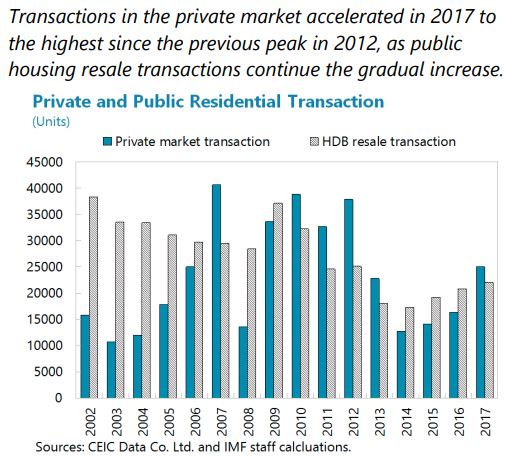

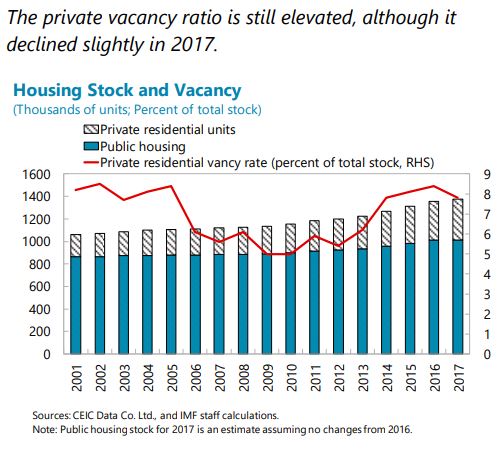

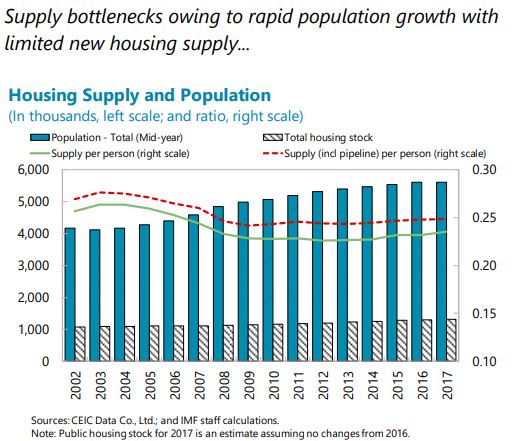

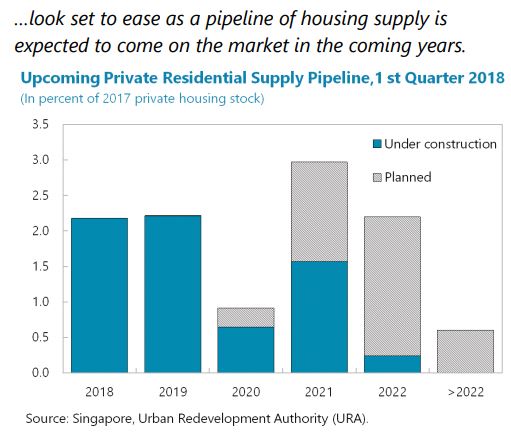

Housing Market in Singapore

The IMF’s latest report on Singapore says that:

“In the housing market, prices of private residential properties staged a steady recovery in 2017, for the first time since 2013, and were up by 5.4 percent y/y in 2018Q1. The share of foreign transactions has remained stable over the past six years (close to 7 percent) but is significantly below the 2011 peak (19.5 percent). Vacancy rates have come down slightly but

are still elevated. In recent quarters, supply in the pipeline (i.e., new and redevelopment projects of private residential units with planning approvals that are expected to be on the market within a few years) has also increased after a few years of falling.”

Singapore’s property market policies are comprehensive, aiming to manage demand and supply with active monitoring and periodic adjustments. Staff’s empirical analysis suggests that the prices of private housing in Singapore are affected by a host of factors, including incomes, rents and interest rates, and by supply and cost determinants. Moreover, while housing prices in major Asian cities are increasingly synchronized, Singapore’s property prices appear to have decoupled and are now relatively attractive to international investors (…). Singapore’s comprehensive set of property market cooling measures, including Additional Buyer’s Stamp Duty (ABSD) and limits on Total Debt Servicing Ratio (TDSR) and Loan to Value (LTV) caps, have been critical to stabilizing the property market. Property prices picked up in the last three quarters and are expected to increase further in the near term. Staff analysis also suggests that prices are now moderately above levels consistent with long-term fundamentals. Higher private property prices have been accompanied by increased transaction volumes amid a stronger economy, improved market sentiments, and the recent increase in collective sales for redevelopment projects. The Seller’s Stamp Duty was relaxed in March 2017. In the 2018 Budget, the Buyer’s Stamp Duty was raised by one percentage point for residential properties valued over S$1 million, justified by the need to make property

taxation more progressive.Against this background, staff’s views on property market measures are as follows:

- On the demand side, property market cooling measures should be maintained, including structural macroprudential policies (TDSR and LTV caps) and cyclical measures, such as ABSD, given the elevated financial risks. However, ABSD is a residency-based capital flow management/macro-prudential measure, and staff recommends eliminating residency-based differentiation by unifying rates (lowering rates charged foreigners to the level charged Singaporeans and foreign residents), and then phasing out the measure once systemic risks from the housing market dissipate.

- On the supply side, housing supply in the pipeline has continued to rise in 2018Q1. A large part of those will be on the market for sale in later this year or the next year, adding significant new supplies of housing stock. Staff encourages the authorities to continue to monitor the supply side to ensure that sufficient land is reserved and released in a timely manner through the government land sales program. In addition, other supply-side measures such as the process of building approval could be targeted to meet housing demand.”

The IMF’s latest report on Singapore says that:

“In the housing market, prices of private residential properties staged a steady recovery in 2017, for the first time since 2013, and were up by 5.4 percent y/y in 2018Q1. The share of foreign transactions has remained stable over the past six years (close to 7 percent) but is significantly below the 2011 peak (19.5 percent). Vacancy rates have come down slightly but

are still elevated.

Posted by at 10:01 AM

Labels: Global Housing Watch

Monday, July 30, 2018

Twin Deficits in Developing Economies

From a new IMF working paper by Davide Furceri and Aleksandra Zdzienicka:

“We provide new evidence of the existence of the “twin deficits” in developing economies. Using unanticipated government spending shocks for an unbalanced panel of 114 developing economies from 1990 to 2015, we find that a one percent of GDP unanticipated improvement in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP. This effect is substantially larger than usually found in the literature using standard measures of fiscal policy changes such as the CAB. This finding has important policy implications as for a given target of external adjustment less fiscal consolidation is required than normally assumed.

Beyond this average effect lies some heterogeneity, both across states of the business cycle and across countries. The effect tends to be larger: (i) during recessions; (ii) in countries that are more open to trade; (iii) that have less flexible exchange rate regimes; and (iv) with lower initial public debt-to-GDP ratios. This heterogeneity has far-reaching implications for policymakers in deciding the magnitude of the fiscal adjustment needed to address external imbalances.”

From a new IMF working paper by Davide Furceri and Aleksandra Zdzienicka:

“We provide new evidence of the existence of the “twin deficits” in developing economies. Using unanticipated government spending shocks for an unbalanced panel of 114 developing economies from 1990 to 2015, we find that a one percent of GDP unanticipated improvement in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP.

Posted by at 10:16 AM

Labels: Macro Demystified

Sunday, July 29, 2018

Difficulties of Making Predictions: Global Power Politics Edition

A new post by Timothy Taylor says that “Making predictions is hard, especially about the future. It’s a comment that seems to have been attributed to everyone from Nostradamus to Niels Bohr to Yogi Berra. But it’s deeply true. Most of us have a tendency to make statements about the future with a high level of self-belief, avoid later reconsidering how wrong we were, and then make more statements. […] The questions of how to predict for what you don’t expect, and how to plan for what you don’t expect, are admittedly difficult. The ability to pivot smoothly to face the new challenge may be one of the most underrated skills in politics and management. ”

Continue reading here.

A new post by Timothy Taylor says that “Making predictions is hard, especially about the future. It’s a comment that seems to have been attributed to everyone from Nostradamus to Niels Bohr to Yogi Berra. But it’s deeply true. Most of us have a tendency to make statements about the future with a high level of self-belief, avoid later reconsidering how wrong we were, and then make more statements. […] The questions of how to predict for what you don’t expect,

Posted by at 3:45 PM

Labels: Forecasting Forum

Subscribe to: Posts