Friday, December 28, 2018

Housing Market in Bolivia

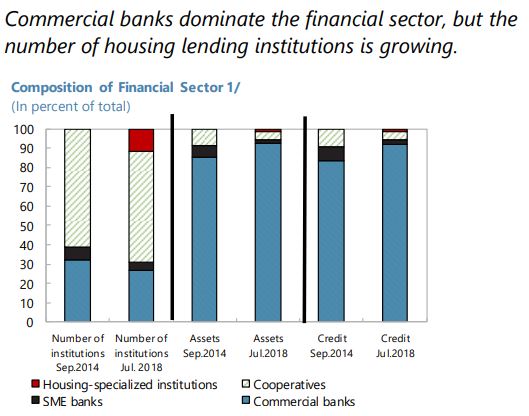

The IMF’s latest report on Bolivia says:

“Credit quotas should be relaxed to limit poor-quality credit growth. Interest caps should also be removed so that lending decisions better reflect intrinsic risks. This would remove distortions in the allocation of credit and support desirable allocation of resources in support of growth. ASFI is urged to monitor closely capital quality for its ability to absorb potential shocks and to scrutinize possible risks arising from rapid credit growth to housing. In this context, the Fund welcomes the opportunity to assist the authorities to prepare a real estate price index and urges rapid progress.”

The IMF’s latest report on Bolivia says:

“Credit quotas should be relaxed to limit poor-quality credit growth. Interest caps should also be removed so that lending decisions better reflect intrinsic risks. This would remove distortions in the allocation of credit and support desirable allocation of resources in support of growth. ASFI is urged to monitor closely capital quality for its ability to absorb potential shocks and to scrutinize possible risks arising from rapid credit growth to housing.

Posted by at 10:15 AM

Labels: Global Housing Watch

Top Ten Posts of 2018

As 2018 draws to a close, below is our list of the top ten blogs of the year.

- RIP Herman Stekler, A Forecasting Giant

- RIP Deena Khatkhate, far-sighted IMF and RBI economist

- How Well Do Economists Forecast Recessions? A Groundhog Day Update

- Economic Growth from Octavian to Obama

- Affordable Housing: Views from Albert Saiz

- The Distribution of Gains from Globalization

- Housing View – January 5, 2018 [2018 AEA Annual Meeting Special Edition]

- Household Credit, Global Financial Cycle, and Macroprudential Policies: Credit Register Evidence from an Emerging Country

- Understanding Singapore’s Housing Market

- Growth and well-being: policy should not be based on GDP alone

Photo by Colton Duke

As 2018 draws to a close, below is our list of the top ten blogs of the year.

- RIP Herman Stekler, A Forecasting Giant

- RIP Deena Khatkhate, far-sighted IMF and RBI economist

- How Well Do Economists Forecast Recessions? A Groundhog Day Update

- Economic Growth from Octavian to Obama

- Affordable Housing: Views from Albert Saiz

- The Distribution of Gains from Globalization

- Housing View – January 5,

Posted by at 9:39 AM

Labels: Macro Demystified

Thursday, December 27, 2018

Top charts of 2018

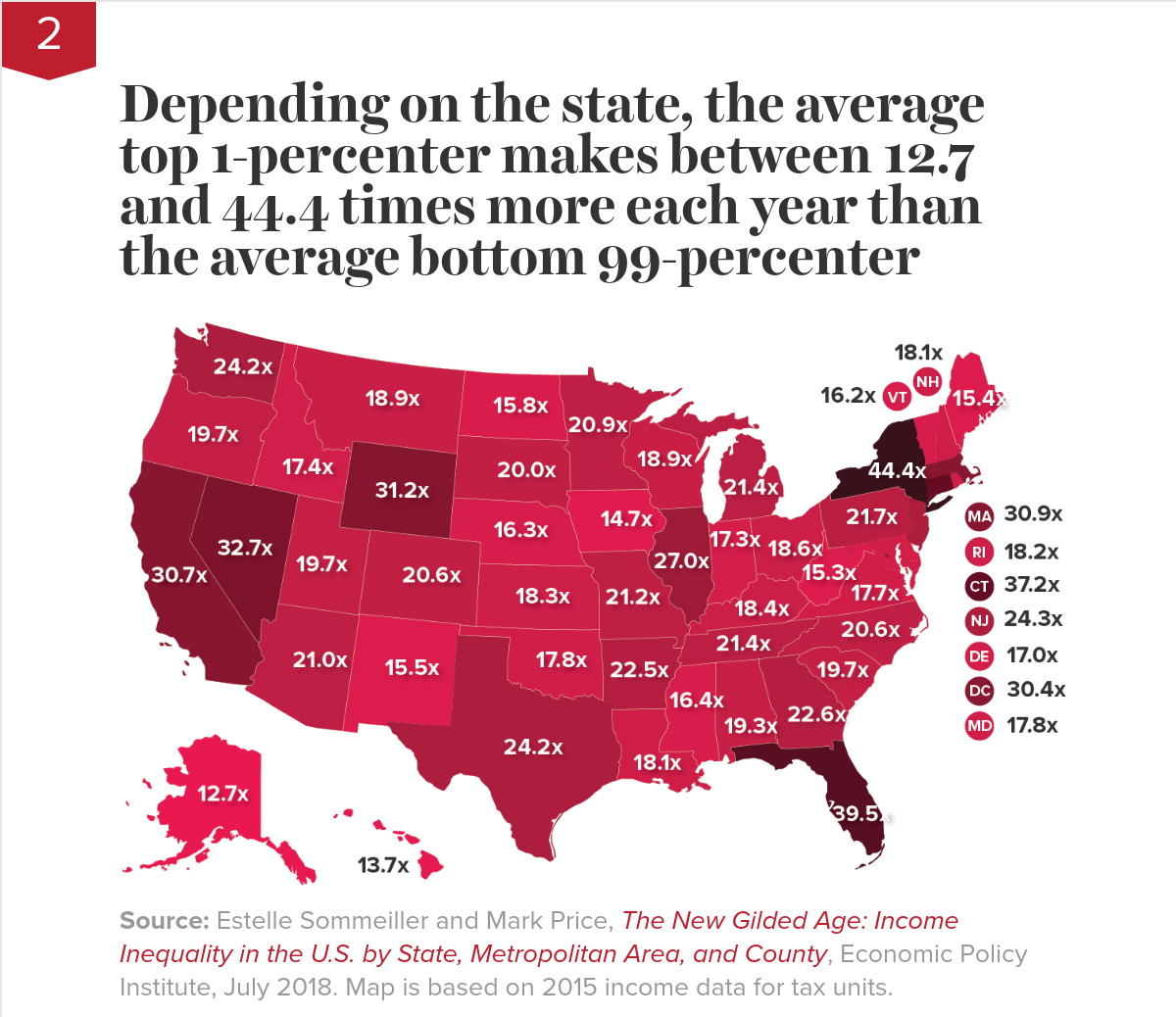

From Economic Policy Institute:

“Twelve charts that show how policy could reduce inequality—but is making it worse instead

With the unemployment rate at 4 percent or below for eight consecutive months, 2018 appears to be the year when the economy finally became healthy again. But while low unemployment is good news, it doesn’t tell the whole story of how typical families are faring in the current economy.

As the economy normalizes following a long, slow recovery from the Great Recession, we are quickly resuming our prerecession course of rising inequality. The fruits of economic growth are bypassing typical families and going straight into the hands of the already-rich.

Our current policy trajectory is doing nothing to reverse the trend of inequality. But it’s doing plenty to widen it. This year’s edition of Top Charts highlights how policy choices continue to exacerbate inequality and how we can achieve more broadly shared prosperity through better policy choices.

Continue reading here.

From Economic Policy Institute:

“Twelve charts that show how policy could reduce inequality—but is making it worse instead

With the unemployment rate at 4 percent or below for eight consecutive months, 2018 appears to be the year when the economy finally became healthy again. But while low unemployment is good news, it doesn’t tell the whole story of how typical families are faring in the current economy.

As the economy normalizes following a long,

Posted by at 12:07 PM

Labels: Macro Demystified

Transmission of U.S. Monetary Policy to Commodity Exporters and Importers

From a new working paper by Myunghyun Kim:

“This paper studies international transmission of U.S. monetary policy shocks to commodity exporters and importers. After first showing empirically that the shocks have stronger effects on commodity exporters than on importers, I then augment a standard three-country model to include commodities. Consistent with the empirical evidence, the model

indicates that an expansionary monetary policy shock to the U.S. increases the aggregate output of commodity exporters by more than that of importers. This is because the increased U.S. aggregate demand triggered by the shock leads to greater U.S. demand for commodities and higher real commodity prices, and thus the exports of commodity exporters increase relative to those of commodity importers. Furthermore, I show that if commodity exporters’ currencies are pegged to the U.S. dollar, then the U.S. monetary policy shocks have stronger spillovers to commodity exporters and importers. In the event that the U.S. becomes a net energy exporter, the shocks will have weaker effects on commodity exporters and stronger impacts on importers.”

From a new working paper by Myunghyun Kim:

“This paper studies international transmission of U.S. monetary policy shocks to commodity exporters and importers. After first showing empirically that the shocks have stronger effects on commodity exporters than on importers, I then augment a standard three-country model to include commodities. Consistent with the empirical evidence, the model

indicates that an expansionary monetary policy shock to the U.S. increases the aggregate output of commodity exporters by more than that of importers.

Posted by at 12:03 PM

Labels: Energy & Climate Change

Tuesday, December 25, 2018

Paper Tigers

From a new post by Adam M. Grossman:

“Economist Prakash Loungani has spent the better part of two decades researching the issue. In a 2001 study, Loungani evaluated experts’ ability to forecast recessions. His conclusion was blunt: “The record of failure to predict recessions is virtually unblemished.” In a follow-up study, looking at the 2008 financial crisis, Loungani’s findings were nearly identical. Economists uniformly failed to predict that global recession.

Perhaps Loungani’s study wasn’t comprehensive enough. What about all-star forecasters? Here the evidence is inevitably more anecdotal, but no more encouraging. Consider Abby Joseph Cohen, the recently-retired Goldman Sachs strategist. Her forecasts during the 1990s earned her the nickname “the Prophet of Wall Street.” But she later missed the two biggest meltdowns of her career: In 2000, when the dot-com bubble burst, Cohen predicted the market would rise. And she, along with virtually everybody else, missed the 2008 collapse.

A more recent example: Ray Dalio, the billionaire founder of hedge fund Bridgewater Associates, proclaimed in January of this year: “If you’re holding cash, you’re going to feel pretty stupid.” The year’s not over yet. But so far, cash has done materially better than the stock market, which is in negative territory.

The reality is that forecasting has always been difficult—and not just in the world of economics. Decca Records told the Beatles they have “no future in show business.” Walt Disney was once fired for “lacking imagination.” The list of incorrect predictions is long.

If forecasts are so error-prone, why do sensible organizations like Vanguard continue issuing them? In part, I believe it’s in response to investor demand: People want to know what’s going to happen and they believe experts can tell them. It’s just human nature. But now that you’ve seen the data, here’s my recommendation: Tune out anyone who approaches you with a crystal ball. Instead, situate yourself so the market’s short-term ups and downs don’t impact your ability to meet your financial goals—or to sleep at night.”

From a new post by Adam M. Grossman:

“Economist Prakash Loungani has spent the better part of two decades researching the issue. In a 2001 study, Loungani evaluated experts’ ability to forecast recessions. His conclusion was blunt: “The record of failure to predict recessions is virtually unblemished.” In a follow-up study, looking at the 2008 financial crisis, Loungani’s findings were nearly identical. Economists uniformly failed to predict that global recession.

Posted by at 8:27 PM

Labels: Forecasting Forum

Subscribe to: Posts