Friday, December 19, 2014

House Prices in Georgia

“Despite an overall positive outlook, there are several key macroeconomic vulnerabilities that would impact the financial sector: (…) Sudden decline in asset prices. As more than half of domestic private credit is backed by real estate, continued increases in real estate prices toward the pre-collapse level in 2008 could become a source of vulnerability,” says a new IMF report on Georgia.

Posted by at 9:06 PM

Labels: Global Housing Watch

House Prices in Denmark

Moreover, the report says that “Danish household debt continues to be the highest among the OECD countries, in large part to finance housing wealth. Household debt has been always relatively high in Denmark, but it grew rapidly during the housing boom, facilitated by the introduction of deferred amortization loans in 2003, reaching about 300 percent of disposable income. On the other side of the balance sheet, household assets are also large with positive net worth. However, these assets consist mostly of illiquid mandatory pension accounts and housing, leaving households with limited liquid buffers and making them more vulnerable to interest rate shocks. The need to rebuild balance sheets has depressed private consumption, weighing on the recovery in recent years.” Continue reading here. Also, see a special note on the mortgage finance system here.

“Danish house prices bottomed out and have recently started to pick up gradually. From the 2007 peak to the 2012 bottom, real house price dropped by about 30 percent. Real house prices started to rise in 2013 and grew 2.6 percent (y/y) in the second quarter of 2014 even though the pace of house price recovery varies across regions and types of housing (e.g., a stronger recovery in the prices of owner occupied flats in the Copenhagen area). Staff estimates based on three different metrics (price-to income ratio, Read the full article…

Posted by at 8:45 PM

Labels: Global Housing Watch

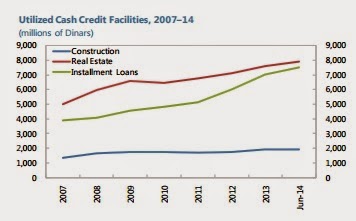

Macro-Prudential Policies in Kuwait

“The CBK has been proactive in introducing macroprudential regulations in line with international practices to mitigate potential financial stability risks. The main source of vulnerability to the banking system comes from credit concentration to the corporate sector and real estate, given the structure of Kuwait’s domestic market, which the central bank regulates through concentration limits. The main sectoral exposures of banks are in real estate, equity and household lending, the latter two regulated through ceilings on equity investments and debt-to-income limits, respectively. Having tracked increased activity in real estate, Read the full article…

Posted by at 8:20 PM

Labels: Global Housing Watch

Macro-Prudential Policies in Turkey

The latest IMF’s report on Turkey lists the recent macro-prudential policies implemented. To see the list click here. Read the full article…

Posted by at 8:08 PM

Labels: Global Housing Watch

House Prices in Netherlands

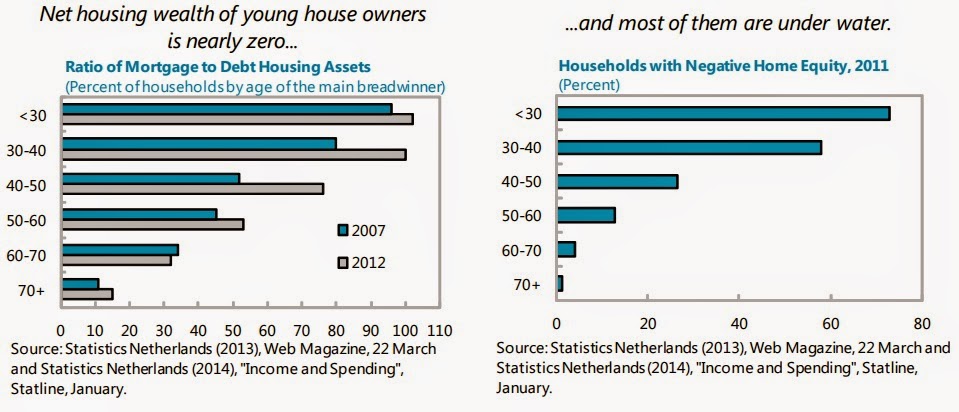

“The global recession and regulatory tightening have helped deflate the housing prices with the losses falling disproportionately on the younger generations. House prices have declined by 27 percent in real terms since their peak in late 2008. The deflation of Dutch housing prices has caused massive losses of wealth which are unevenly distributed across generations. Younger house buyers are burdened by the lion’s share of losses in housing wealth. In addition to greater housing losses, younger households have not have sufficient time to accumulate pension claims and other (financial) assets households under the age of 35 have negligible levels of net worth,” Read the full article…

Posted by at 8:02 PM

Labels: Global Housing Watch

Subscribe to: Posts