Friday, December 19, 2014

Macro-Prudential Policies in Kuwait

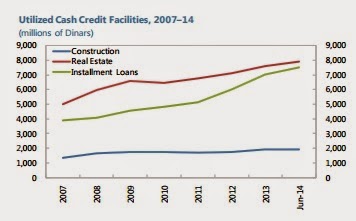

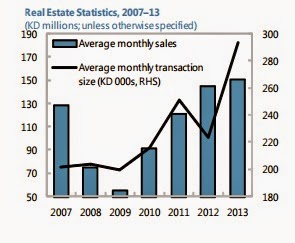

“The CBK has been proactive in introducing macroprudential regulations in line with international practices to mitigate potential financial stability risks. The main source of vulnerability to the banking system comes from credit concentration to the corporate sector and real estate, given the structure of Kuwait’s domestic market, which the central bank regulates through concentration limits. The main sectoral exposures of banks are in real estate, equity and household lending, the latter two regulated through ceilings on equity investments and debt-to-income limits, respectively. Having tracked increased activity in real estate, the central bank introduced a loan-to-value ratio for residential real estate for investment purposes of individuals in November 2013, to limit financial stability risks, which staff welcomes. Staff has also observed that activity has been recently increasing in investment properties and commercial real estate segments of the real estate market, which the central bank is closely watching and ready to use macroprudential tools to limit potential stability risks to the banking system arising from this sector,” according to latest IMF report on Kuwait.

Posted by at 8:20 PM

Labels: Global Housing Watch

Subscribe to: Posts