Thursday, January 13, 2022

Fiscal Inflation

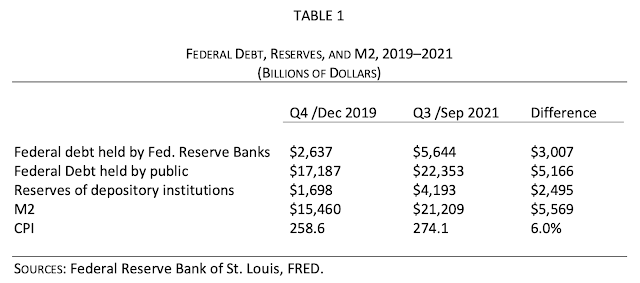

In his blog, The Grumpy Economist, John H. Cochrane, Senior Fellow at Stanford University’s Hoover Institution writes about the role of fiscal policy in pushing inflation.

“Starting in March 2020, in response to the disruptions of Covid-19, the U.S. government created about $3 trillion of new bank reserves, equivalent to cash, and sent checks to people and businesses. (Mechanically, the Treasury issued $3 trillion of new debt, which the Fed quickly bought in return for $3 trillion of new reserves. The Treasury sent out checks, transferring the reserves to people’s banks. See Table 1.) The Treasury then borrowed another $2 trillion or so, and sent more checks. Overall federal debt rose nearly 30 percent. Is it at all a surprise that a year later inflation breaks out? It is hard to ask for a clearer demonstration of fiscal inflation, an immense fiscal helicopter drop, exhibit A for the fiscal theory of the price level (Cochrane 2022a, 2022b).”

Click here to read the full blog.

Related Reading:

In his blog, The Grumpy Economist, John H. Cochrane, Senior Fellow at Stanford University’s Hoover Institution writes about the role of fiscal policy in pushing inflation.

“Starting in March 2020, in response to the disruptions of Covid-19, the U.S. government created about $3 trillion of new bank reserves, equivalent to cash, and sent checks to people and businesses. (Mechanically, the Treasury issued $3 trillion of new debt, which the Fed quickly bought in return for $3 trillion of new reserves.

Posted by at 8:53 AM

Labels: Macro Demystified

Sunday, January 2, 2022

The new consensus of economists is further to the left

They say economists rarely agree on one thing.

However, now this statement may not hold true as before. Based on a survey of members of the American Economic Association, a paper by Doris Geide-Stevenson and Alvaro La Parra Perez of the Weber State University compares the academic positions of economists over four decades.

“The main result is an increased consensus on many economic propositions, specifically the appropriate role of fiscal policy in macroeconomics and issues surrounding income distribution. Economists now embrace the role of fiscal policy in a way not obvious in previous surveys and are largely supportive of government policies that mitigate income inequality. Another area of consensus is concern with climate change and the use of appropriate policy tools to address climate change.”

Click here to download the paper and here to be a part of the discussion on it.

They say economists rarely agree on one thing.

However, now this statement may not hold true as before. Based on a survey of members of the American Economic Association, a paper by Doris Geide-Stevenson and Alvaro La Parra Perez of the Weber State University compares the academic positions of economists over four decades.

“The main result is an increased consensus on many economic propositions, specifically the appropriate role of fiscal policy in macroeconomics and issues surrounding income distribution.

Posted by at 10:33 AM

Labels: Inclusive Growth, Macro Demystified

Wednesday, December 22, 2021

Why low interest rates force us to revisit the scope and role of fiscal policy

In an article for the Peterson Institute for International Economics, economist Olivier Blanchard discusses 45 takeaways on the changing scope of fiscal policy and debt sustainability, in the light of consistently low interest rates. He also discusses three applications of the same- in the US, Japan, and Europe. Excerpts from the article:

- “A case of too little? The shift from output stabilization to debt reduction in the wake of the global financial crisis in Europe was too strong and too costly, reflecting an excessive weight on the costs of debt and an insufficient belief in the adverse effects of contractionary fiscal policy on demand and output.

- A case of just right? Faced with a strong case of secular stagnation, Japan has run large deficits for three decades and debt ratios have increased to very high levels, while the Bank of Japan remained at the effective lower bound. Was it the right strategy (if indeed it was a strategy)? The answer is a qualified yes, but, looking forward, the high debt ratios raise issues of debt sustainability. Alternative ways of boosting demand should be a high priority.

- A case of too much? To boost the US recovery from the initial COVID-19 shocks, the Biden administration embarked in 2021 on a major fiscal expansion. The strategy (again, if indeed it was a strategy) was for fiscal policy to increase demand and thus increase the neutral rate, and for monetary policy to delay the adjustment of the policy rate to the neutral rate, and in the process generate temporary inflation. Inflation has turned out to be much higher than expected. Was the fiscal expansion too strong? Was the strategy a mistake?”

Click here to read the full article.

In an article for the Peterson Institute for International Economics, economist Olivier Blanchard discusses 45 takeaways on the changing scope of fiscal policy and debt sustainability, in the light of consistently low interest rates. He also discusses three applications of the same- in the US, Japan, and Europe. Excerpts from the article:

- “A case of too little? The shift from output stabilization to debt reduction in the wake of the global financial crisis in Europe was too strong and too costly,

Posted by at 2:50 PM

Labels: Macro Demystified

Subscribe to: Posts