Monday, June 17, 2013

MAULDIN: Economists Are Totally Clueless About The Economy

“In November of 2008, as stock markets crashed around the world, the Queen of England visited the London School of Economics to open the New Academic Building. While she was there, she listened in on academic lectures. The Queen, who studiously avoids controversy and almost never lets people know what she’s actually thinking, finally asked a simple question about the financial crisis: “How come nobody could foresee it?” No one could answer her.”

“If you’ve suspected all along that economists are useless at the job of forecasting, you would be right. Dozens of studies show that economists are completely incapable of forecasting recessions. But forget forecasting. What’s worse is that they fail miserably even at understanding where the economy is today. In one of the broadest studies of whether economists can predict recessions and financial crises, Prakash Loungani of the International Monetary Fund wrote very starkly, “The record of failure to predict recessions is virtually unblemished.” He found this to be true not only for official organizations like the IMF, the World Bank, and government agencies but for private forecasters as well. They’re all terrible. Loungani concluded that the “inability to predict recessions is a ubiquitous feature of growth forecasts.” Most economists were not even able to recognize recessions once they had already started.” Read the full article here.

“In November of 2008, as stock markets crashed around the world, the Queen of England visited the London School of Economics to open the New Academic Building. While she was there, she listened in on academic lectures. The Queen, who studiously avoids controversy and almost never lets people know what she’s actually thinking, finally asked a simple question about the financial crisis: “How come nobody could foresee it?”

Posted by at 6:43 PM

Labels: Forecasting Forum

Wednesday, May 29, 2013

Tackling Unemployment: Return of the Two-Handed Approach

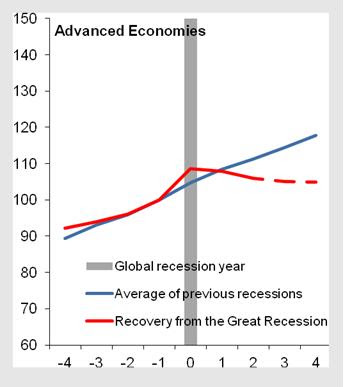

Unemployment in advanced economies averages 8% today, a sharp rise from 5 ½ % at the start of the Great Recession. European unemployment is particularly high—about 11% on average. What can be done?

In a celebrated mid-1980s paper, Olivier Blanchard, along with Rudi Dornbusch and others, argued that tackling the high unemployment and low growth in Europe at that time would require a ‘two-handed approach’: a combination of demand-side and supply-side policies. It is not coincidental that the IMF’s current advice to countries reflects the return of the two-handed approach.

In presentations delivered at the European Commission, ILO, World Bank and other venues, Prakash Loungani—advisor in the Research Department and co-chair of the IMF’s “Jobs & Growth” working group—has made the case for balancing demand and supply initiatives to tackle unemployment in advanced economies. He notes that, contrary to some assertions, unemployment and growth have remained linked during the Great Recession and the Not-So-Great Recovery. This preserves the hope that the jobs will return when the growth does.

Evidence suggests that the bulk of the rise in unemployment in most countries has been cyclical. Hence, as the Wall Street Journal noted recently, it’s time to “stop worrying about the ‘jobless recovery’ [and] start worrying about the recovery-less recovery.” Citing work on Okun’s Law by IMF authors and other recent evidence, the Journal concluded that “it isn’t unemployment benefits or other specific [structural] factors that are holding back hiring. It’s the economy, stupid.”

Several factors are behind the tepid recovery in output. In work done for the recent World Economic Outlook, Ayhan Kose, Prakash Loungani and Marco Terrones note that a key difference between the current global recovery and past global recoveries is that fiscal policy has not been able to provide the support this time that it did in the past—a point that has been picked by many observers including Paul Krugman (see the figure on fiscal spending below and Krugman’s essay here).

|

| Real Primary Government Expenditures |

The two-handed approach does not neglect supply. In a recent Staff Discussion Note, Olivier Blanchard, Florence Jaumotte and Prakash Loungani discuss many labor market reforms that have been advocated in recent IMF programs in Europe. They argue that, by and large, these reforms can be expected to contribute to ‘micro flexibility’ (the ability of the economy to reallocate workers across jobs to boost productivity) and ‘macro flexibility’ (the ability of the economy to adjust to macroeconomic shocks).

Unemployment in advanced economies averages 8% today, a sharp rise from 5 ½ % at the start of the Great Recession. European unemployment is particularly high—about 11% on average. What can be done?

In a celebrated mid-1980s paper, Olivier Blanchard, along with Rudi Dornbusch and others, argued that tackling the high unemployment and low growth in Europe at that time would require a ‘two-handed approach’: a combination of demand-side and supply-side policies.

Posted by at 1:39 PM

Labels: Inclusive Growth

Tuesday, May 21, 2013

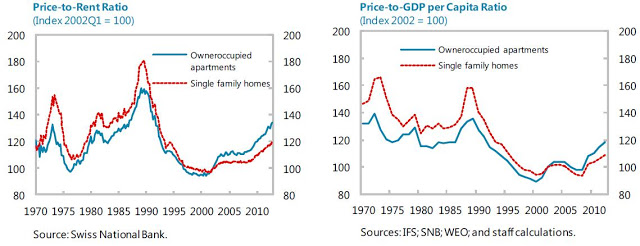

House Prices in Switzerland

“House prices are high, but it’s too early to call it a bubble,” according to an IMF study on the Swiss Housing Market: What are the risks? It says that “real house prices are high, and at an all-time high for owner-occupied apartments. Prices have been on an increasing trend since the late 1990s and the average price for a single family home has increased by about 49 percent. Prices for owner occupied apartments have increased even more (72 percent) and in the last four years the annualized price increase (5 1/2 percent) substantially exceed nominal GDP growth. When deflating house prices by the CPI, owner-occupied apartment prices are slightly above the peak of the boom-bust period in the late 80s to early 90s. Single family home prices are still below the peak, but still high by historic standards. Residential house price increases are especially pronounced in certain segments and region. Turning to regional patterns, Geneva stands out with price increases far exceeding the other regions in both the single family home and the owner occupied segments. It is also important to note that the price increases started from already high price levels.”

However, “current prices look less elevated when compared to income and rents. Following the

boom in the late 80s housing prices fell dramatically and their subsequent growth remained

subdued relative to growth in rents and in GDP per capita until the late 2000s, when housing price growth accelerated. While these ratios are still well below the levels reached at the peak of the previous boom, the ratio of price to rents for owner occupied apartments is already 15 percent above its long-term average.”

“House prices are high, but it’s too early to call it a bubble,” according to an IMF study on the Swiss Housing Market: What are the risks? It says that “real house prices are high, and at an all-time high for owner-occupied apartments. Prices have been on an increasing trend since the late 1990s and the average price for a single family home has increased by about 49 percent. Prices for owner occupied apartments have increased even more (72 percent) and in the last four years the annualized price increase (5 1/2 percent) substantially exceed nominal GDP growth.

Posted by at 2:47 PM

Labels: Global Housing Watch

What’s Holding Back Hiring?

From the Wall Street Journal:

Stop worrying about the “jobless recovery.” Start worrying about the recovery-less recovery.

Nearly four years after the recession officially ended, the unemployment rate remains elevated, at 7.5%. The share of the population that’s working or looking for work is at a 30-year low. More than 2.5 million fewer Americans are working today than when the recession began.

Such grim statistics have led many economists to ask whether there might be deep, “structural” factors holding back hiring. Various papers have attributed the slow pace of job growth to the weak housing market, the downturn in specific industries and the long-run decline in the share of the population that’s working.

Others, however, have argued that there is little evidence for structural problems, and have said weak hiring is due to something much simpler: the slow pace of overall economic growth. In one recent paper, economists Laurence Ball, Daniel Leighand Prakash Loungani said the improvement in the job market during the recovery has been consistent with a long-documented relationship between unemployment and economic growth known as Okun’s Law.

In a new paper published by the National Bureau of Economic Research,University of Wisconsin economist (and blogger) Menzie Chinn and French economists Laurent Ferrara and Valerie Mignon also look at the relationship between economic growth and the job market. But rather than focus on unemployment, they focus on employment — an approach that allows them to avoid the nettlesome question of who should count as unemployed.

Mr. Chinn and his colleagues find that slow growth accounts for the majority of the continued jobs gap — but not all of it. The U.S. has about 1.2 million fewer jobs than it should based on long-run trends. The authors are careful not to say the entire gap is due to structural factors — some of it may be due to short-term issues, or to flaws in their economic model — but their findings do suggest the weak recovery alone doesn’t explain the weak job market.

Continue to the read the article here.

From the Wall Street Journal:

Stop worrying about the “jobless recovery.” Start worrying about the recovery-less recovery.

Nearly four years after the recession officially ended, the unemployment rate remains elevated, at 7.5%. The share of the population that’s working or looking for work is at a 30-year low. More than 2.5 million fewer Americans are working today than when the recession began.

Such grim statistics have led many economists to ask whether there might be deep,

Posted by at 1:18 AM

Labels: Inclusive Growth

Friday, May 17, 2013

House Prices in Belgium

“Real estate prices have continued to increase steadily through the financial crisis, outpacing increases in other advanced countries,” according to the IMF’s annual economic report on Belgium. It says that “prices have increased by 60 percent in real terms since 2000, and—unlike in other EU countries—there has been no price correction during the crisis. Marked increases in price-to-income and price-to-rent ratios relative to historical average suggest significant overvaluation. However, these measures do not account for the fact that housing was relatively inexpensive to begin with, and that there is therefore a large catching up effect underlying the rise of these indicators. Also, the rental market is very narrow as it is focused only on low-income social housing on one hand and high-end apartments in Brussels on the other. A broader assessment, including a comparison of absolute price levels relative to the rest of Europe, suggests that the degree of overvaluation is of the order of 5 to 20 percent.”

“Real estate prices have continued to increase steadily through the financial crisis, outpacing increases in other advanced countries,” according to the IMF’s annual economic report on Belgium. It says that “prices have increased by 60 percent in real terms since 2000, and—unlike in other EU countries—there has been no price correction during the crisis. Marked increases in price-to-income and price-to-rent ratios relative to historical average suggest significant overvaluation. However, these measures do not account for the fact that housing was relatively inexpensive to begin with,

Posted by at 3:55 PM

Labels: Global Housing Watch

Subscribe to: Posts