Thursday, February 13, 2014

House Prices in Australia

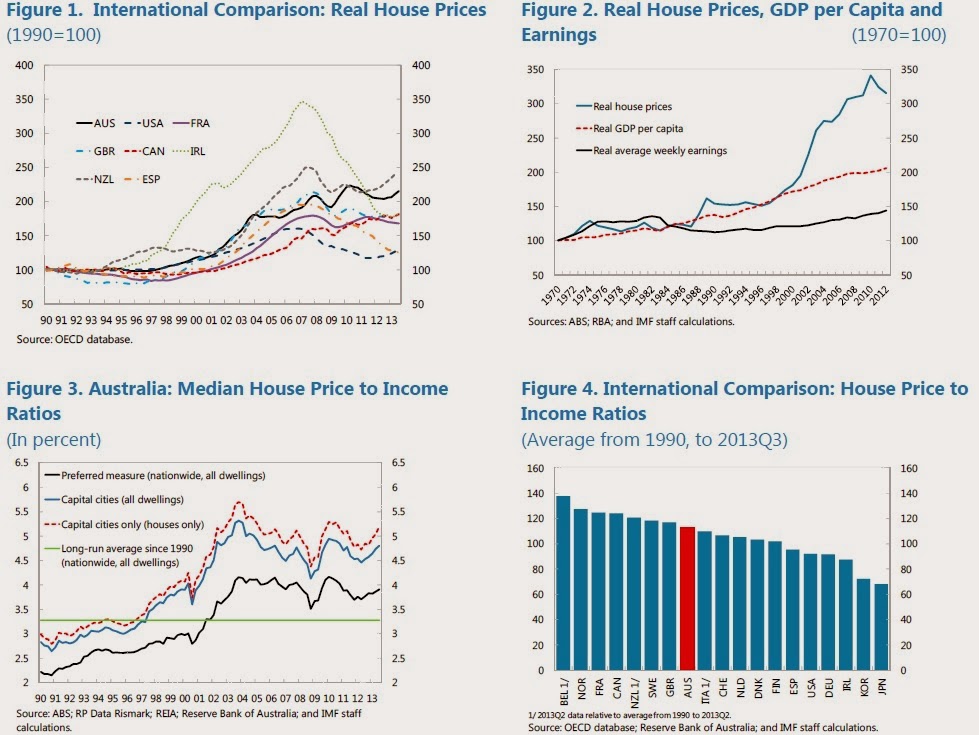

“Reflecting structural factors both shared with many other countries and unique to Australia, real house prices have roughly doubled since 1990 (Figure 1). After growing broadly in line with real GDP per capita from 1960-90, real house price inflation picked up in the 2000s and exceeded income growth for much of the period up to the global financial crisis (Figure 2). As a result, the median house price to income ratio rose sharply from around 3 at the beginning of the 2000s (when based on the authorities’ preferred measure for all dwellings) peaking at just over 4 in 2009 (Figure 3). Since then the price/income ratio has eased back and international comparisons suggest that while Australia’s is on the high side it is not out of line with peers (Figure 4). Rising house prices were also accompanied by increased household borrowing with the debt to income ratio rising from among the lowest at 46 percent in 1990 to around 150 per cent in 2013,” according to the latest IMF’s annual report on Australia.

“Reflecting structural factors both shared with many other countries and unique to Australia, real house prices have roughly doubled since 1990 (Figure 1). After growing broadly in line with real GDP per capita from 1960-90, real house price inflation picked up in the 2000s and exceeded income growth for much of the period up to the global financial crisis (Figure 2). As a result, the median house price to income ratio rose sharply from around 3 at the beginning of the 2000s (when based on the authorities’ preferred measure for all dwellings) peaking at just over 4 in 2009 (Figure 3).

Posted by at 6:50 PM

Labels: Global Housing Watch

House Prices in Israel

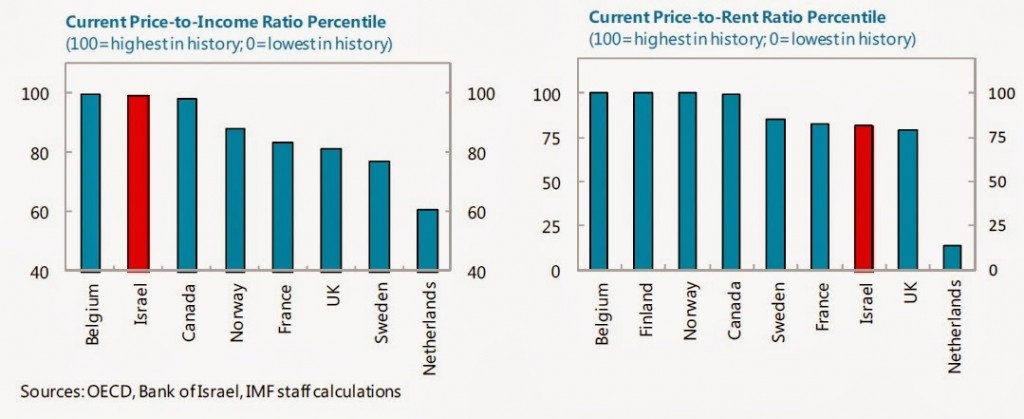

“Property prices in Israel are currently about 25 percent above their equilibrium value, owing largely to low mortgage interest rates and supply shortages. The risk of a sharp correction in house prices, while mitigated by the supply shortages, remains a concern and could have important macro-financial implications. To contain such risks, macroprudential policies should be further tightened. At the same time, concerted efforts should be made to alleviate supply-side constraints,” says IMF’s special issues study on Israel’s housing market. The study talks about the developments in the housing market, Read the full article…

Posted by at 6:19 PM

Labels: Global Housing Watch

Tuesday, February 4, 2014

Unconventional Energy Boom in Canada

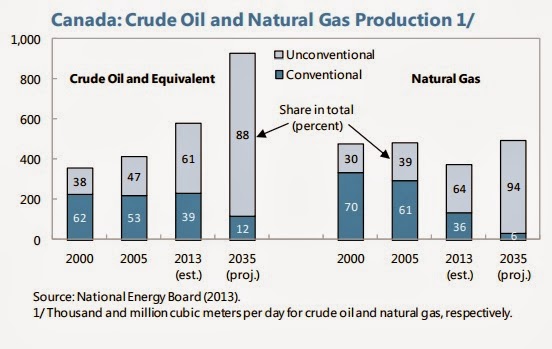

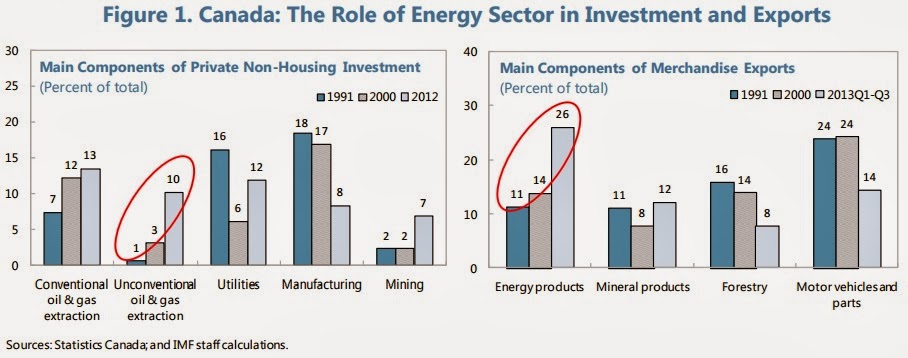

“The unconventional energy boom has had significant positive effects on Canada’s economic activity and has the potential to contribute even more in the future with the appropriate extension of infrastructure capacity,” according to a new IMF study.

“The unconventional energy boom has had significant positive effects on Canada’s economic activity and has the potential to contribute even more in the future with the appropriate extension of infrastructure capacity,” according to a new IMF study.

The study “(…) suggest that while limited exports capacity would result in output losses over the medium term, the potential output gains from a full market access of Canada’s energy products could reach about 2 percent of GDP over a ten year horizon. Read the full article…

Posted by at 1:19 AM

Labels: Energy & Climate Change

Monday, February 3, 2014

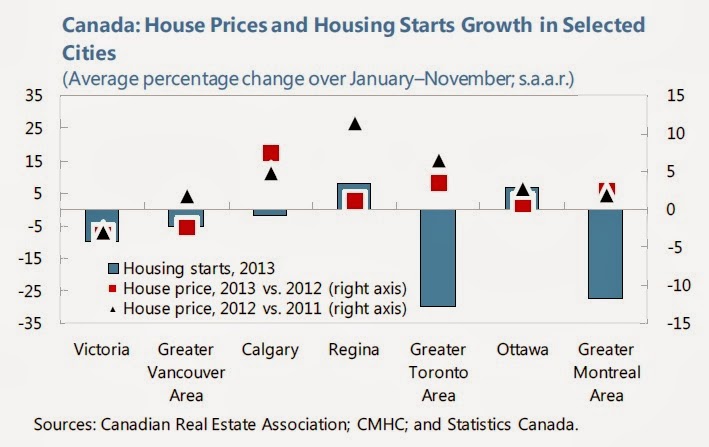

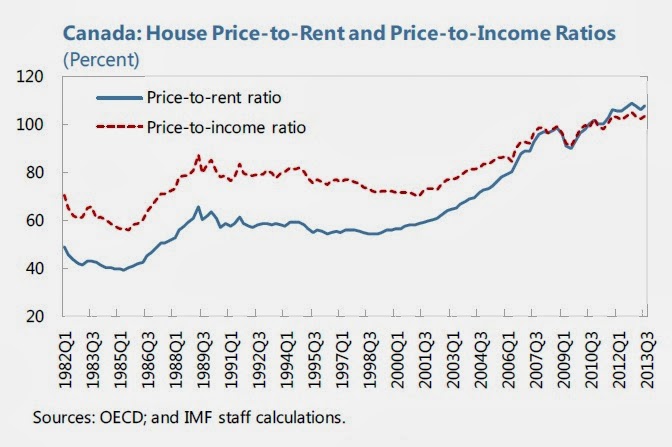

House Prices in Canada

“Household leverage remains high, and while house price and construction growth have come off their post-crisis peaks, high valuations and excess supply in a number of housing markets are a source of vulnerability. If maintained, the ongoing moderation in the housing market suggests little need for additional macro-prudential measures but it is important to remain vigilant. Over the longer term, rethinking the role of government-backed mortgage insurance may reduce the government exposure to housing sector risks and lead to a more efficient allocation of resources,” says the new IMF report on Canada.

More specifically on house prices and valuation measures, it says “Canada’s housing market has cooled but house prices remain overvalued, although with important regional differences. Despite picking up somewhat in mid-2013, in line with renewed strength in resale activity, Canada’s house price inflation and residential investment growth have slowed. On average across Canada, house prices grew about 4 percent (y/y) in November 2013, up from 2 percent in April but about half the pace two years ago. The slowdown involved all large metropolitan areas except Calgary, particularly Vancouver (where house prices in the first eleven months of 2013 were about 3 percent lower than a year ago). Housing starts have also picked up since April 2013, but are on a declining trend: as of November 2013, their 6-month moving average was about 10 percent below last year’s peak, mainly owing to weaker construction of multiple units, especially in Ontario. Despite the downward trend in growth, a few simple indicators continue to suggest overvaluation in the Canadian housing market. In particular, house prices are high relative to both income and rents, compared to historical averages and many other advanced economies. Staff estimates that, in real terms, average house prices in Canada are about 10 percent above what would be justified by fundamentals, with most of the gap coming from the real estate markets in Ontario and Québec.”

“Household leverage remains high, and while house price and construction growth have come off their post-crisis peaks, high valuations and excess supply in a number of housing markets are a source of vulnerability. If maintained, the ongoing moderation in the housing market suggests little need for additional macro-prudential measures but it is important to remain vigilant. Over the longer term, rethinking the role of government-backed mortgage insurance may reduce the government exposure to housing sector risks and lead to a more efficient allocation of resources,”

Posted by at 5:42 PM

Labels: Global Housing Watch

Wednesday, January 29, 2014

House Prices in Peru

“Real estate prices have risen substantially over the past few years (…) However, deviation of prices from fundamentals has apparently been minimal,” according to the new IMF report on the Peruvian economy.

“Real estate prices have risen substantially over the past few years (…) However, deviation of prices from fundamentals has apparently been minimal,” according to the new IMF report on the Peruvian economy.

The report also points out that (i) the “ratio of house prices to annual rental income has increased slightly to 15½ in 2013 from around 13½ in 2010″ and (ii) the recent macroprudential measures taken–“capital charges on higher loan-to-value mortgages, Read the full article…

Posted by at 6:09 PM

Labels: Global Housing Watch

Subscribe to: Posts