Friday, May 9, 2014

House Prices in Luxembourg

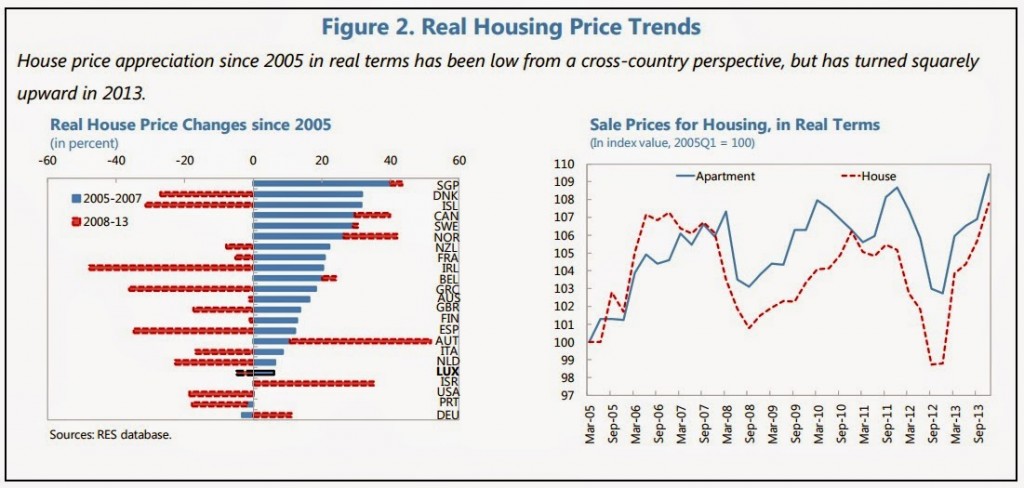

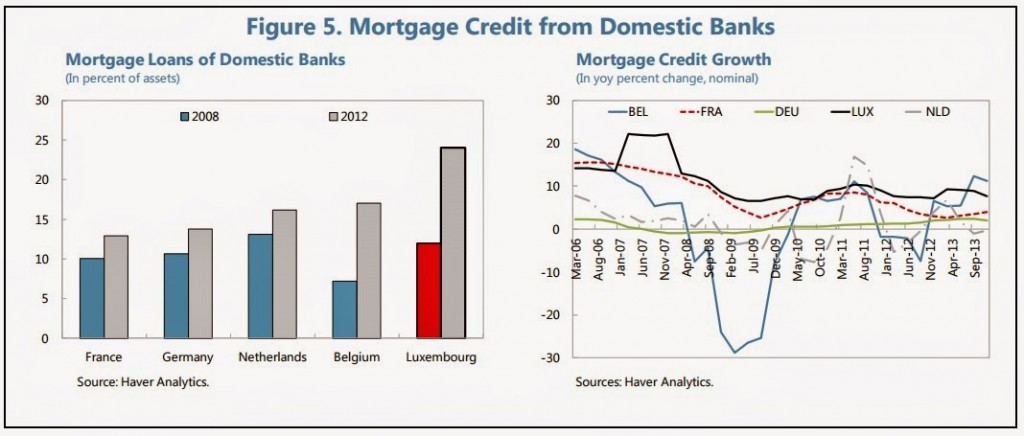

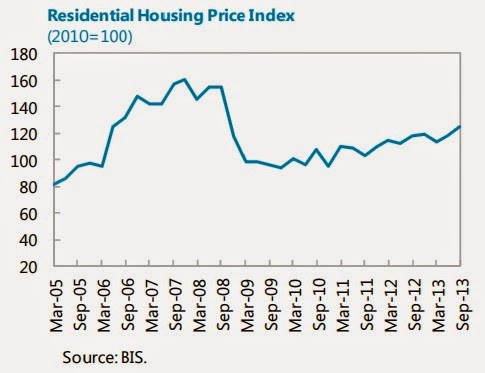

“Without policy action, underlying forces for housing price appreciation will likely persist (…) Prices do not appear overvalued at this time, though they have recently picked up (…) Banks’ increased exposure to mortgages bears vigilance, and buffers should be maintained. The tightening in the risk weights for LTVs above a certain level for banks, and the capital surcharge for domestically-oriented banks, are appropriate. If these measures are found to be insufficient after some period of observation, further steps may be needed (…) Government policies should become more neutral in relation to home ownership vs. renting. Current policies provide incentives for ownership, spurring demand pressures further”–these are the main points from the overall assessment of a new IMF study on Luxembourg’s housing market.

“Without policy action, underlying forces for housing price appreciation will likely persist (…) Prices do not appear overvalued at this time, though they have recently picked up (…) Banks’ increased exposure to mortgages bears vigilance, and buffers should be maintained. The tightening in the risk weights for LTVs above a certain level for banks, and the capital surcharge for domestically-oriented banks, are appropriate. If these measures are found to be insufficient after some period of observation,

Posted by at 6:21 PM

Labels: Global Housing Watch

Thursday, May 8, 2014

House Prices in Estonia

“The housing market is recovering from a very sharp decline during the crisis, but prices and household leverage are well below their peak levels,” says the new IMF economic report on Estonia. The report also says that “the housing market peaked in 2007 before house prices lost roughly half of their value by 2009. Prices have risen since then, but they are roughly midway between the peak and the trough. Loan-to-value ratios on new loans have fallen from roughly 100 percent of the purchase price before the crisis to roughly 60 percent since 2010.”

“The housing market is recovering from a very sharp decline during the crisis, but prices and household leverage are well below their peak levels,” says the new IMF economic report on Estonia. The report also says that “the housing market peaked in 2007 before house prices lost roughly half of their value by 2009. Prices have risen since then, but they are roughly midway between the peak and the trough. Loan-to-value ratios on new loans have fallen from roughly 100 percent of the purchase price before the crisis to roughly 60 percent since 2010.”

Posted by at 12:36 PM

Labels: Global Housing Watch

Wednesday, May 7, 2014

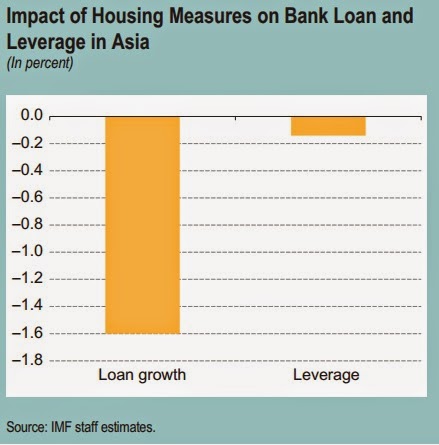

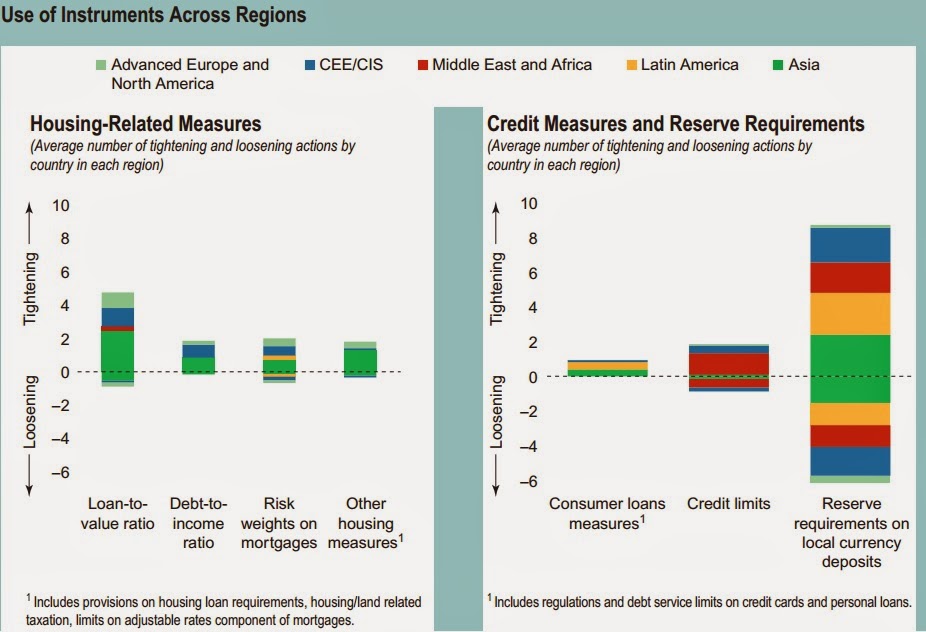

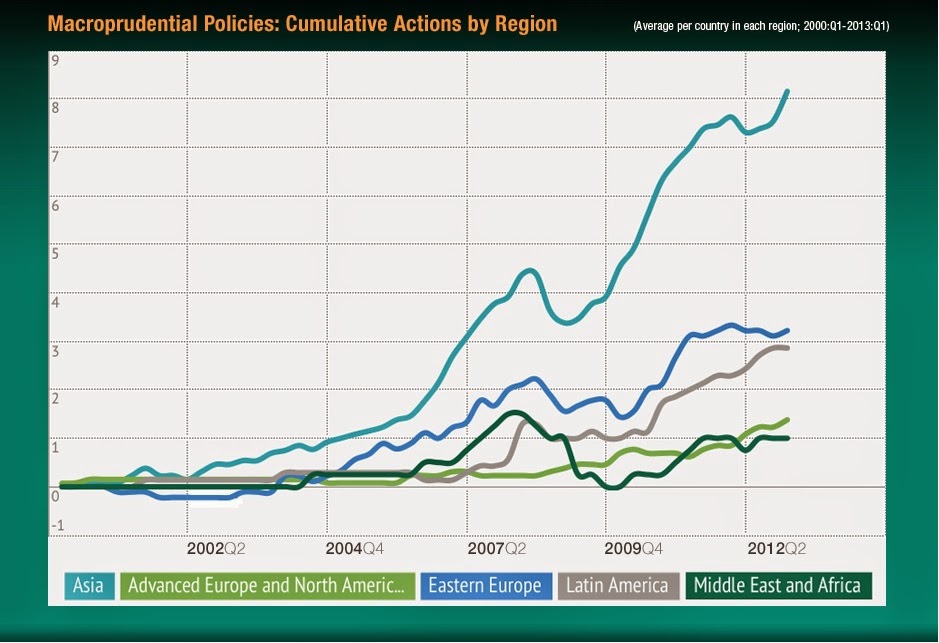

Macroprudential Policies in Asia

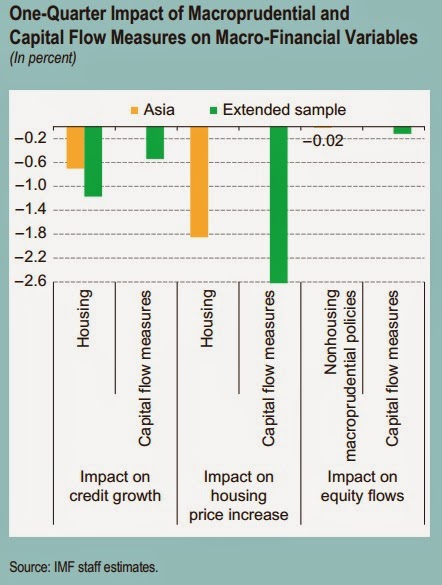

In Asia, macroprudential policies related to the housing sector has been the most effective. They have reduced house price inflation by two percentage points after one quarter. Moreover, “housing-related macroprudential instruments have had an impact—particularly caps on loan-to-value ratios and the taxation of housing transactions. In particular, such instruments have helped lower credit growth, slow house price inflation, and dampen bank leverage in Asia (although the latter effect is quite small),” says a new IMF study on Macroprudential Policy and Capital Flow Measures in Asia: Use and Effectiveness.

In Asia, macroprudential policies related to the housing sector has been the most effective. They have reduced house price inflation by two percentage points after one quarter. Moreover, “housing-related macroprudential instruments have had an impact—particularly caps on loan-to-value ratios and the taxation of housing transactions. In particular, such instruments have helped lower credit growth, slow house price inflation, and dampen bank leverage in Asia (although the latter effect is quite small),” says a new IMF study on Macroprudential Policy and Capital Flow Measures in Asia: Use and Effectiveness.

Posted by at 7:37 PM

Labels: Global Housing Watch

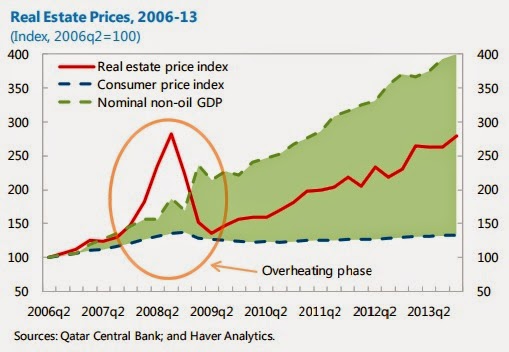

House Prices in Qatar

“House prices have been growing strongly since the crisis-related drop in 2008-09, but according to crude measures, valuations appear broadly in line with fundamentals,” according to the IMF’s annual economic report on Qatar.

“House prices have been growing strongly since the crisis-related drop in 2008-09, but according to crude measures, valuations appear broadly in line with fundamentals,” according to the IMF’s annual economic report on Qatar.

Posted by at 6:55 PM

Labels: Global Housing Watch

Tuesday, April 29, 2014

Global House Prices: Continue Rising

House Prices in OECD Countries: Where Do They Stand?

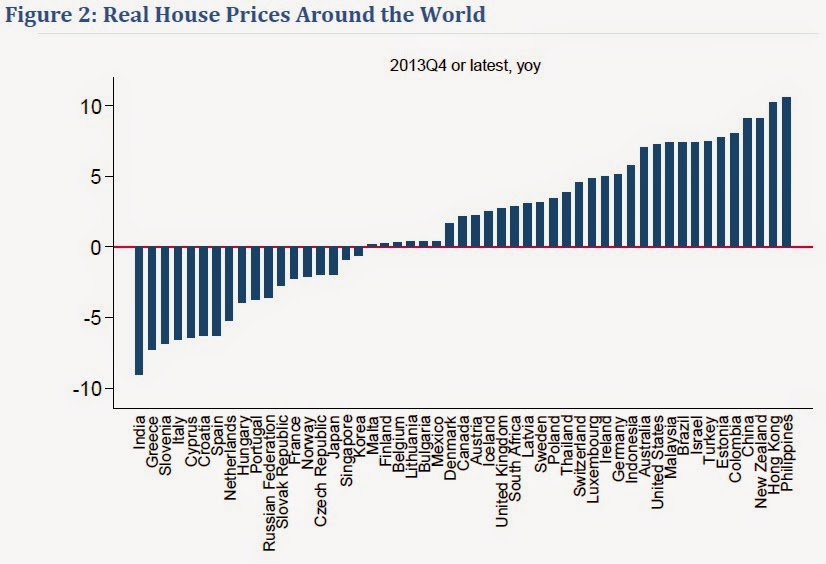

When comparing current house prices to the fourth quarter of 2006, the scale is balanced with half of the countries showing an increase in house prices and the other half showing a decline. However, the picture changes when we look at standard house price valuations in OECD countries. More than half of the OECD countries are above their historical averages for price-to-income and price-to-rent ratios. But, these valuations metrics should be taken with a grain of salt (e.g. in Finland, there is a difference between how actual average markets rents and the CPI rent component have developed, which over time results in difference in price-to-rent ratio).

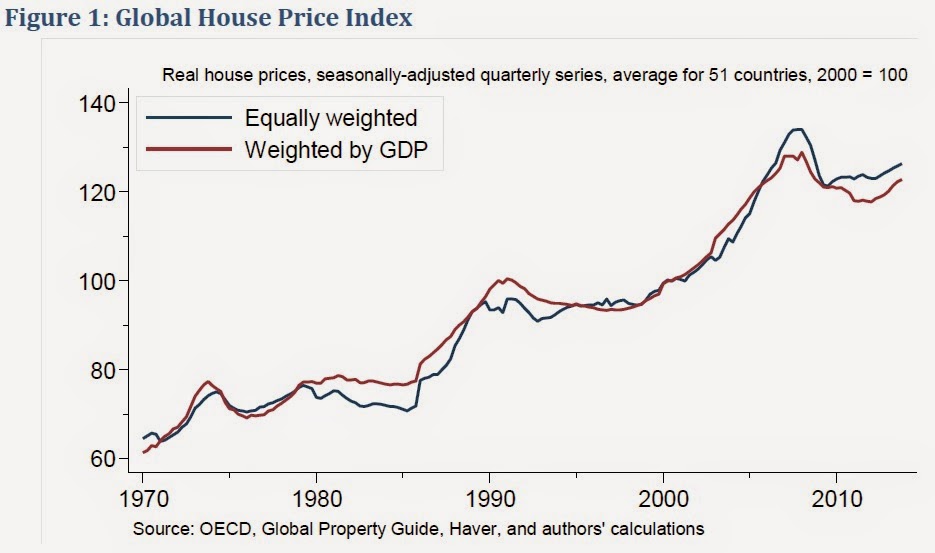

At the aggregate level, global house price index continues to rise, registering seven consecutive quarters of growth. Similarly, at the micro level, more countries are registering growth, thirty three out of fifty one countries.

House Prices in OECD Countries: Where Do They Stand?

When comparing current house prices to the fourth quarter of 2006, the scale is balanced with half of the countries showing an increase in house prices and the other half showing a decline.

Posted by at 3:54 PM

Labels: Global Housing Watch

Subscribe to: Posts