Tuesday, October 7, 2014

Global Housing Prices: It’s a Tale of Two Worlds

From the Wall Street Journal by Nick Timiraos:

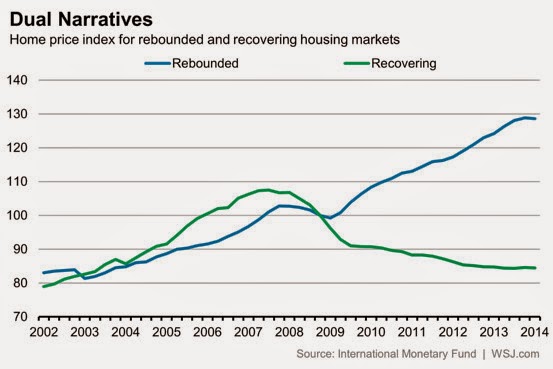

An index tracking global property prices in 50 countries shows prices haven’t much risen over the past five years, but new research from the International Monetary Fund shows how averages can be misleading.

The IMF divided those countries into two groups. The first group of 33 countries, which includes the U.S. and the United Kingdom, are those where prices are still recovering. Prices in this group ran up strongly before the 2008 financial crisis and dropped sharply after it hit. These countries have also witnessed a generally slower economic rebound.

The second group of 17 countries, which includes Australia, Canada and China, had a smaller pre-crisis housing boom and have seen stronger post-crisis economic growth.

The result shows a very clear tale of two recoveries. Home prices in the 33 “recovering” countries are around 20% below their 2008 levels, while prices in the 17 “rebounded” countries are roughly 25% higher.

(The recovering countries are Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Finland, France, Greece, Hungary, Iceland, India, Indonesia, Ireland, Italy, Japan, Korea, Latvia, Lithuania, Malta, Mexico, Netherlands, Poland, Portugal, Russia, Slovak Republic, Slovenia, South Africa, Spain, Thailand, United Kingdom, and the U.S.

The rebounded countries are Australia, Austria, Brazil, Canada, China, Colombia, Germany, Hong Kong, Israel, Luxembourg, Malaysia, New Zealand, Norway, Philippines, Singapore, Sweden and Switzerland.)

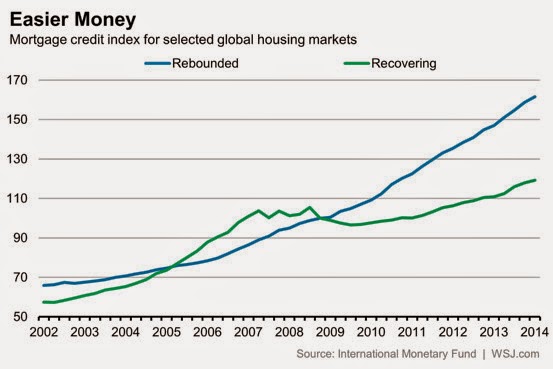

A smaller subset of these countries shows a similar story for mortgage credit. Credit has expanded far more slowly in the recovering countries than for the rebounded countries.

Those countries with stronger housing markets have enjoyed better economic growth. The gross value added of construction and real residential investment are both 15% higher than in 2008, while those countries with weaker housing markets have seen only a small uptick in the last year.

Of course, policy makers in countries with stronger housing markets may also face greater challenges, given concerns that prices may be rising in an unsustainable way. Earlier this year, the IMF began its “Global Housing Watch” as part of an effort to curb complacency among regulators and policy makers about housing bubbles.

The latest IMF report flags China as a particular cause for concern. “The challenge is to allow for the necessary correction in real estate markets while preventing an excessively sharp slowdown,” write authors Hites Ahir and Prakash Loungani.

Canada and Israel are modestly overvalued, the authors write, while Norway and Sweden are substantially overvalued. While the United Kingdom has seen substantial price gains over the last year, sparking concerns from central bankers, the IMF classifies it in the basket of “recovering” markets because it experienced sharp price declines from 2008 to 2010.

From the Wall Street Journal by Nick Timiraos:

An index tracking global property prices in 50 countries shows prices haven’t much risen over the past five years, but new research from the International Monetary Fund shows how averages can be misleading.

The IMF divided those countries into two groups. The first group of 33 countries, which includes the U.S. and the United Kingdom, are those where prices are still recovering.

Posted by at 11:33 PM

Labels: Global Housing Watch

Tuesday, September 23, 2014

Moving on: Labor mobility in the United States

There is an old quip about a guy who hears on the local news that most accidents happen within five miles of home. “Darn, I’ve got to move,” he says to himself. Moving wouldn’t solve this guy’s problem, but moving on has generally been an important means of responding to bad news about regional prospects. For the United States, the importance of labor mobility as an adjustment mechanism in the face of adverse regional shocks was shown in a classic paper by Blanchard and Katz (1992). Over 20 years later, how have the Blanchard-Katz findings held up?

Mai Dao, Davide Furceri and I have updated and extended the Blanchard-Katz findings in a new paper. What do we find?

- Labor mobility remains an important adjustment mechanism in the United States. The use of direct migration data and of instrumental variables estimation, however, suggests that the response of mobility is weaker than in the original Blanchard-Katz paper.

- There are larger mobility responses to regional shocks in recessions than in good times. This seems counter-intuitive: is it really worth moving during a recession from a place with 12 percent unemployment to a place with 7 percent unemployment?. We try to understand why this might be the case and suggest that the answer could lie in cyclical variation in the ability to smooth consumption. Using standard tests, we show that the ability to insure consumption against idiosyncratic risk is pro-cyclical, rising in booms while being almost absent in recessions. Hence it appears that the increased migration during recessions comes out of the desperation of people who have run out of other options.

- Some suggestive evidence in support of this view comes from micro data: we show that it is mostly the long-term unemployed and labor market entrants who undertake the bulk of increased migration during recessions. The long-term unemployed tend to experience larger and more persistent income losses and labor market entrants have the least savings to tap into and less collateral to obtain loans. Therefore one would also expect these groups to have the lowest ability to smooth consumption over the downturn.

In an earlier version of the paper we also compared labor mobility in Europe and the US; these findings were summarized by Krugman.

There is an old quip about a guy who hears on the local news that most accidents happen within five miles of home. “Darn, I’ve got to move,” he says to himself. Moving wouldn’t solve this guy’s problem, but moving on has generally been an important means of responding to bad news about regional prospects. For the United States, the importance of labor mobility as an adjustment mechanism in the face of adverse regional shocks was shown in a classic paper by Blanchard and Katz (1992).

Posted by at 11:16 AM

Labels: Inclusive Growth

What Lies Beneath: A Sub-National Look at Okun’s Law

Saurabh Mishra and I have been estimating Okun’s Law for U.S. states. It seems to hold quite well in most states. Judge for yourself:

http://murmuring-harbor-6048.herokuapp.com/index.html

Saurabh Mishra and I have been estimating Okun’s Law for U.S. states. It seems to hold quite well in most states. Judge for yourself:

http://murmuring-harbor-6048.herokuapp.com/index.html

Posted by at 11:12 AM

Labels: Inclusive Growth

Monday, September 15, 2014

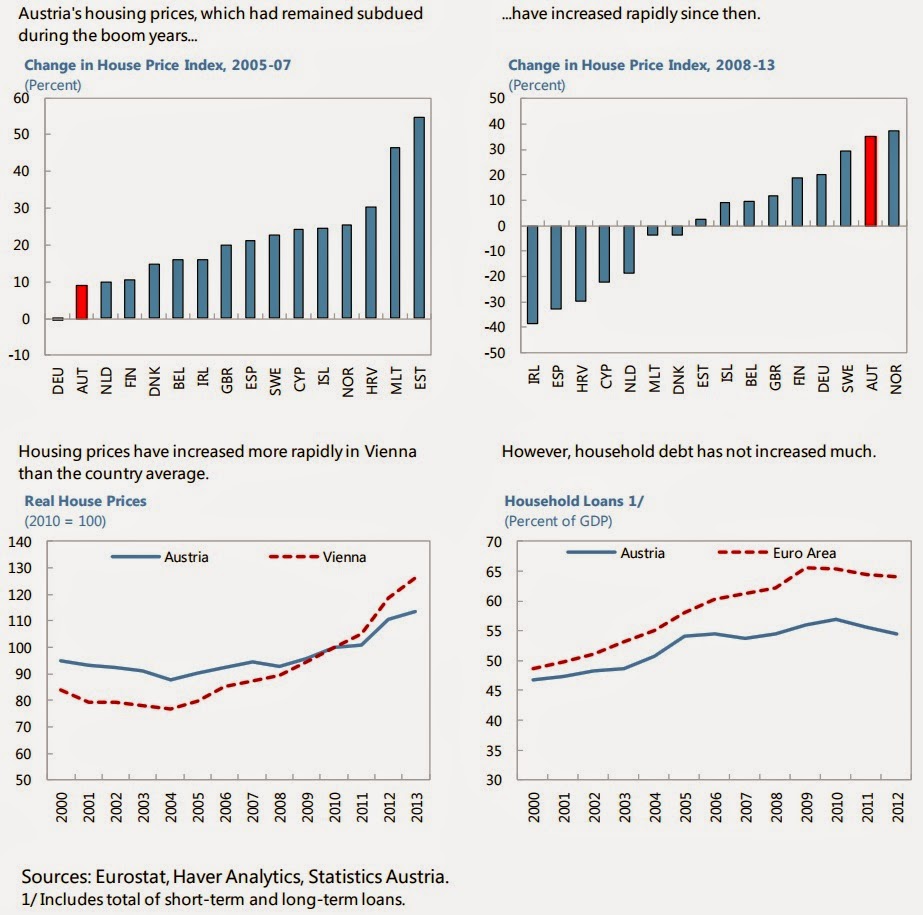

House Prices in Austria

“Neither the non-financial corporate sector nor the household sector is overleveraged, but housing prices warrant monitoring,” according to the IMF’s annual economic report on Austria. The reports says that “Housing price increases have been strong in recent years but purchases have been to a large extent cash-financed and the strongest growth has been predominantly limited to Vienna and some tourist hotspots.”

“Neither the non-financial corporate sector nor the household sector is overleveraged, but housing prices warrant monitoring,” according to the IMF’s annual economic report on Austria. The reports says that “Housing price increases have been strong in recent years but purchases have been to a large extent cash-financed and the strongest growth has been predominantly limited to Vienna and some tourist hotspots.”

Posted by at 2:32 PM

Labels: Global Housing Watch

Wednesday, September 3, 2014

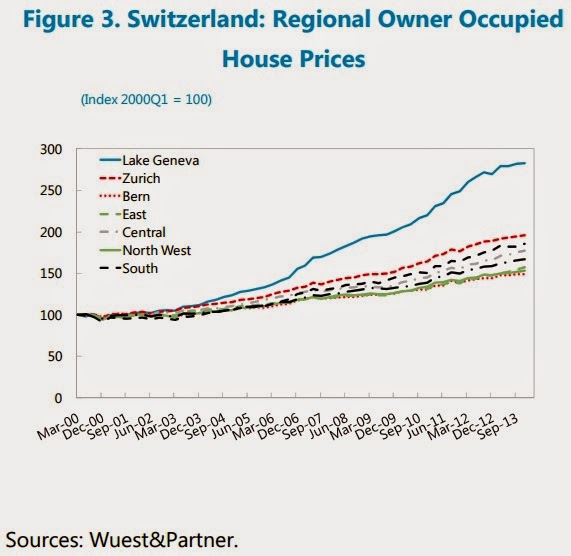

House Prices in Switzerland

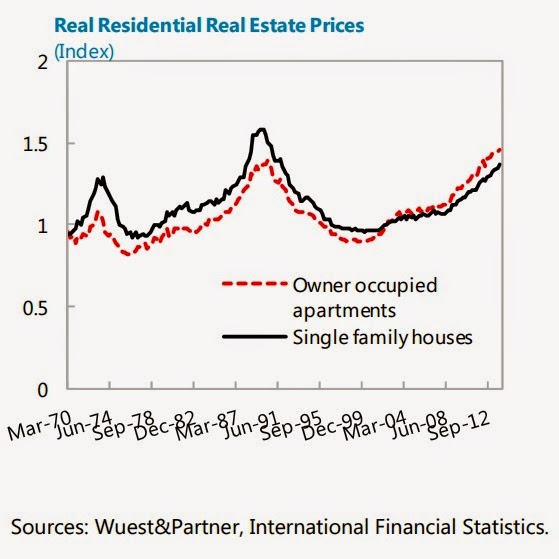

“Residential real estate prices have been on an upward trend since the late 1990s, and increases have been especially strong for owner occupied apartments. Through end-2013 prices for owner occupied apartments had increased by 77 percent in the last ten years, while prices for single family homes increased by 49 percent during the same period (…). Also in real terms have prices increased significantly. Compared to the CPI, owner occupied prices are at an all time high, almost 5 percent above the previous peak in the early 1990s before the sharp downward adjustment. Single family home prices are still about 14 percent below the peak, but above the peak in the 1970s and high in a historical perspective,” according to the IMF’s technical note on Switzerland.

More specifically, the note says that “Real estate price increases have been more dramatic in some regions. In particular at Lake Geneva, where prices for owner occupied apartments during the last ten years had increased by 152 percent through the third quarter of 2013 (…). Single family homes prices had increased by 91 percent during the same period. The price increases also started from already high levels.”

In terms of valuation measures, the note says that “Comparing residential real estate prices to rents and income shows substantially increased ratios. Compared to rents, prices of owner occupied apartments have increased by about 25 percent in the last 10 years, which is significant (…). The ratio is nevertheless well below the historical high, though above the historical average. For single family home, the price to rent ratio is just above the long-run average. Turning to real estate prices compared to GDP per capita, the picture is fairly similar, and the ratio for owner occupied apartments prices is around 10 percent above the long-run average, while single family homes are a little below.”

“Residential real estate prices have been on an upward trend since the late 1990s, and increases have been especially strong for owner occupied apartments. Through end-2013 prices for owner occupied apartments had increased by 77 percent in the last ten years, while prices for single family homes increased by 49 percent during the same period (…). Also in real terms have prices increased significantly. Compared to the CPI, owner occupied prices are at an all time high,

Posted by at 5:20 PM

Labels: Global Housing Watch

Subscribe to: Posts