Tuesday, May 26, 2015

Europe’s Housing Market

The performance of the European housing market remains mixed. In Europe, house prices are rising in some countries and falling in others. Moreover, even though the number of transactions is recovering, housing supply indicators remain in the doldrums. There is also an issue of housing affordability. The bullet points below gives a summary of these developments.

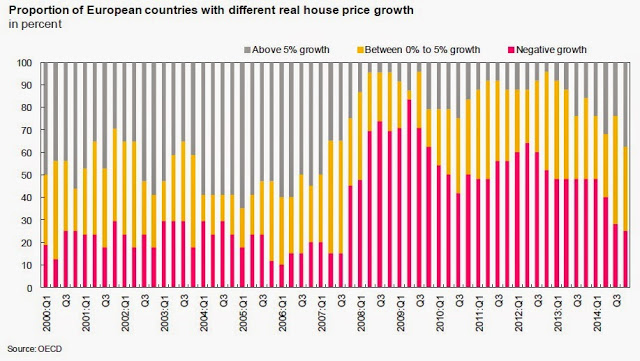

House price developments. Europe was the weakest-performing world region in 2014, with house prices rising on average by 1.6 percent, says Knight Frank. Similarly, Global Property Guide notes that “Europe’s property markets are surging ahead [(…) However,] some parts of Europe continue to struggle. Seven of the 22 European housing markets included in our global survey saw house price falls in 2014.” This mixed performance in the housing market reflects the divergent economic performance in Europe, according to Scotiabank. However, the momentum in house prices could be shifting. The graph below shows that the proportion of European countries with negative real house price growth has been on a downward trend since the last three quarters of 2014.

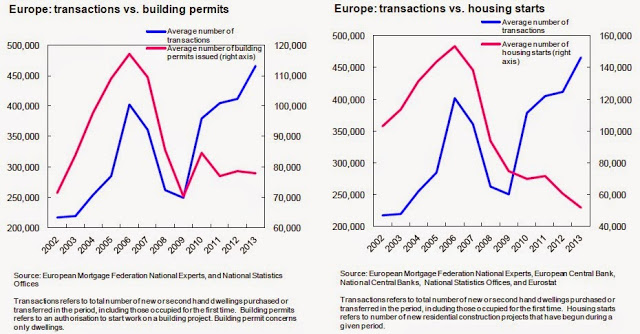

Housing supply developments. “The continued recovery in housing starts, relative to a period considered normal [2002], is not isolated to the United States, says Michael Neal of the National Association of Home Builders. Indeed, a review of Europe’s mortgage and housing market shows that housing supply indicators are continuing to shrink (EMF Hypostat 2014). The report notes that “Data for 2012 and 2013 shows a continued contraction in the [housing supply] market, which still is not feeling the positive effect of a pick-up in mortgage activity in many EU countries. This mainly reflects the existence of an overhang in the housing market in terms of unsold units, which therefore makes new construction unnecessary at the moment. It is likely that construction will pick up again in the coming months and years, though it is uncertain when (and whether) it will return to pre-crisis levels in Europe.”

Affordability. The issue of housing affordability has been discussed in many countries. In Europe, there are more people without a home today than six years ago, and there are not enough affordable homes available in most European countries to meet the increasing demand; these are two emerging issues from a new report that looks at the state of the housing market in the Europe (Housing Europe).

From the Global Housing Watch Newsletter: May 2015 Issue

The performance of the European housing market remains mixed. In Europe, house prices are rising in some countries and falling in others. Moreover, even though the number of transactions is recovering, housing supply indicators remain in the doldrums. There is also an issue of housing affordability. The bullet points below gives a summary of these developments.

House price developments. Europe was the weakest-performing world region in 2014,

Posted by at 6:57 PM

Labels: Global Housing Watch

Monday, May 25, 2015

House Prices in Korea

On housing finance, the report says that “at the same time the structure of household debt could be strengthened. Reflecting Korea’s relatively young and rapidly growing mortgage market (…), a large share of houses are financed short-term either in the form of chonsei rental deposits or the rolling over of floating-rate interest-only mortgage loans with short maturities and bullet repayments. One key challenge will be to facilitate the transition by households and financial institutions toward a more stable, long-term structure (…).”

“Measures to try to revive a housing market that has been in a multi-year slump including legislation to unwind major regulatory roadblocks for housing reconstruction projects which had been previously introduced to curb house price inflation and speculative demand. In the wake of these measures, together with some unwinding of the earlier tightening of mortgage lending restrictions (…), there have been some preliminary signs of a pickup in house prices and transactions volumes,” says the latest IMF report on Korea. Read the full article…

Posted by at 4:33 AM

Labels: Global Housing Watch

Wednesday, May 13, 2015

House Prices in Brazil

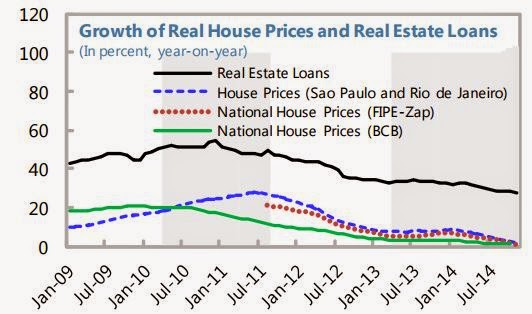

“Even with strong mortgage loan growth, house price inflation slowed, indicating improved housing penetration,” according to the IMF’s economic report on Brazil.

Posted by at 1:46 PM

Labels: Global Housing Watch

Thursday, May 7, 2015

House Prices in Thailand

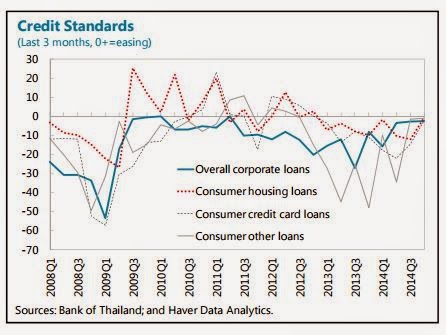

“In view of the slowing credit growth, low share of real estate loans, and no apparent real estate boom, staff does not see a need to tighten macroprudential policies despite the low-interest-rate environment. Looking forward, credit is expected to provide a smaller contribution to growth given the high leverage of households (…) Mirroring the relatively low share of real estate loans, Thailand has not gone through a real estate boom in recent years, except in selected urban locations. Read the full article…

Posted by at 6:14 PM

Labels: Global Housing Watch

House Prices in Jordan

“Real estate prices increased faster than inflation in 2014, but bank and household exposure to credit risk in real estate has remained limited,” according to latest IMF report on Jordan.

Posted by at 6:06 PM

Labels: Global Housing Watch

Subscribe to: Posts