Friday, September 25, 2015

The Stekler Award for Courage in Forecasting (Recessions Inaccurately)

My presentation at the Federal Forecasters Conference summarized my work on the inability or unwillingness of forecasters to predict recessions. I also suggested that to get forecasters to predict recessions (even inaccurately) we should have a Stekler Award for Courage in Forecasting. The award would be in honor of noted forecaster Herman Stekler who says that forecasters should predict recessions early and often and that he himself has predicted 9 of the last 5 recessions. Read the full article…

Posted by at 2:00 PM

Labels: Forecasting Forum

Monday, September 21, 2015

Developments in Israel’s Housing Market

Another IMF report compares the system of taxation on housing in Israel with other countries. It finds that “The current framework of housing taxation in Israel is broadly in line with global standards, but with few elements that have likely increased underlying demand for housing. (…) The Israeli government has appropriately taken steps to tighten the eligibility of exemptions for the capital gains, acquisition tax, and gift taxes. (…) Addressing the supply-side issues will be critical.”

The IMF’s latest report on Israel points out that “To contain further housing price increases, supply needs to be boosted. Concerted efforts among relevant ministries and local governments are needed. To contain the increase in leverage, macroprudential measures should be used.”

Another IMF report compares the system of taxation on housing in Israel with other countries. It finds that “The current framework of housing taxation in Israel is broadly in line with global standards,

Posted by at 9:00 AM

Labels: Global Housing Watch

Friday, September 18, 2015

Housing Market in Saudi Arabia

The report also “(…) emphasized the need for ensuring that the housing needs of the population are met in a cost-effective way while minimizing the disruption to private real estate and mortgage markets. Housing is appropriately an important policy priority, but the program cost is high and to date it has moved slowly. Measures to expand supply should include a strengthened role for the government acting as a facilitator and regulator rather than a developer to help expand housing supply in a cost effective way. In this context, streamlining regulatory and approval processes to achieve efficiency gains could improve the functioning of private real estate markets. With respect to the support for buyers, financing should be targeted to those who are unable to obtain financing from banks or finance companies, and focus on purchases of new dwellings to avoid bidding real estate prices up further.”

“The government is continuing to implement its program to provide affordable housing. In light of the growing population and reported high house prices in the major cities, this is a considerable challenge. Estimates suggest that 160-180,000 new homes will need to be built each year over the next few years to meet growing demand. The government has allocated SR 250 billion from the budget surplus fund for the program, and the Ministry of Housing is continuing to develop options to support buyers which include the provision of interest-free loans (up to SR 500,000), Read the full article…

Posted by at 9:00 AM

Labels: Global Housing Watch

Wednesday, September 16, 2015

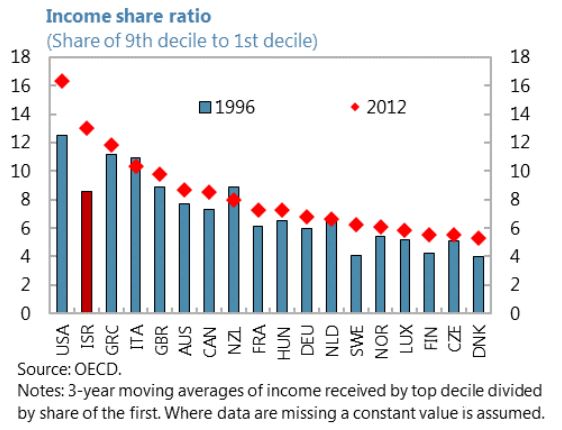

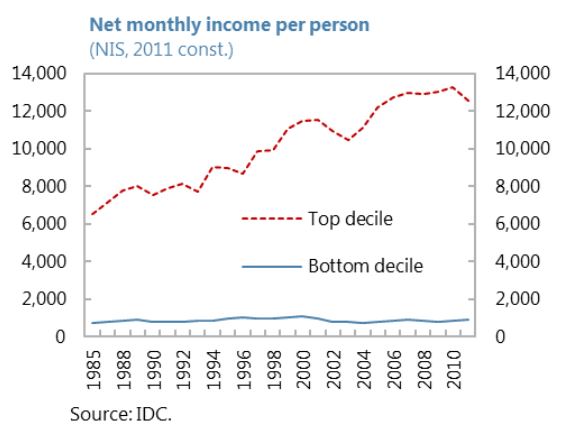

Israel’s Labor Market: High Inequality, Low Productivity

- Inequality in Israel is among the highest in the OECD (this refers to net income inequality, that is, inequality of income after tax and transfers). The income share of the richest 10 percent of people is 13 times the share of the bottom 10 percent, a ratio that is exceeded only by the United States. Real disposable incomes of the top decile have increased since the 1980s, while incomes of the bottom decile have stagnated. Israel’s Gini coefficient of disposable income is among the highest in the OECD.

- Average incomes in Israel are similar to those in Korea and New Zealand but well below the level in richer Western European countries and the United States. There was rapid catch-up toward U.S. incomes between 1950 and the mid- 1970s, but since then Israel’s average income has stagnated at around 60 percent of US average incomes.

- Part of this stagnation is due to low productivity growth. One reason may be that Israel is the most restrictive amongst advanced economies in terms of product market regulations—state control, barriers to entrepreneurship, and barriers to trade and investment all rank amongst the highest across its peers.. In terms of sectors, Israel ranks amongst the highest in regulation of network sectors, retail trade and professional services.

A new IMF report provides an in-depth look at Israel’s labor market:

- Inequality in Israel is among the highest in the OECD (this refers to net income inequality, that is, inequality of income after tax and transfers). The income share of the richest 10 percent of people is 13 times the share of the bottom 10 percent, a ratio that is exceeded only by the United States. Real disposable incomes of the top decile have increased since the 1980s,

Posted by at 5:58 PM

Labels: Inclusive Growth

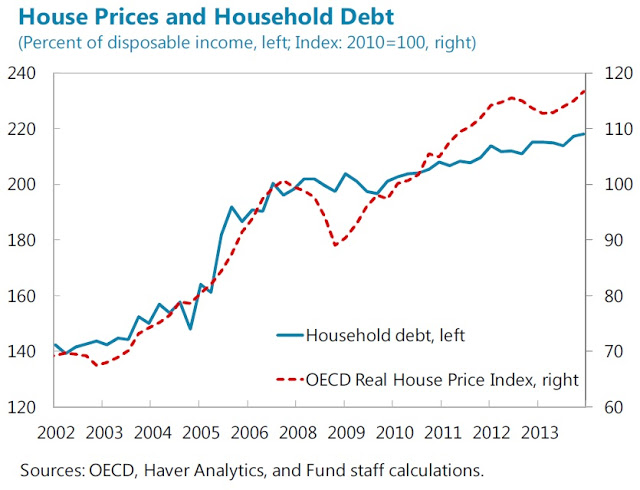

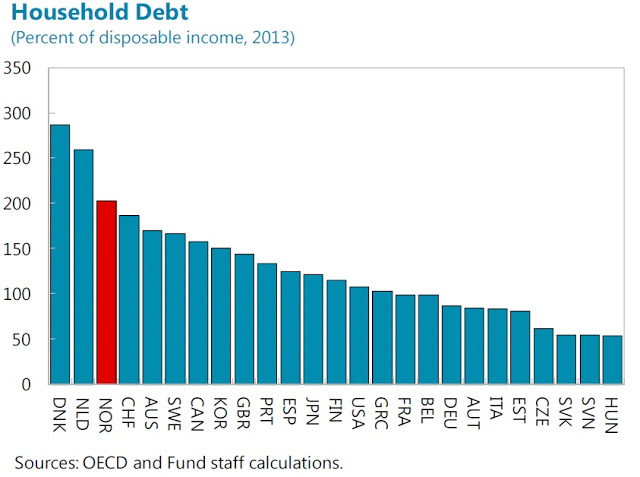

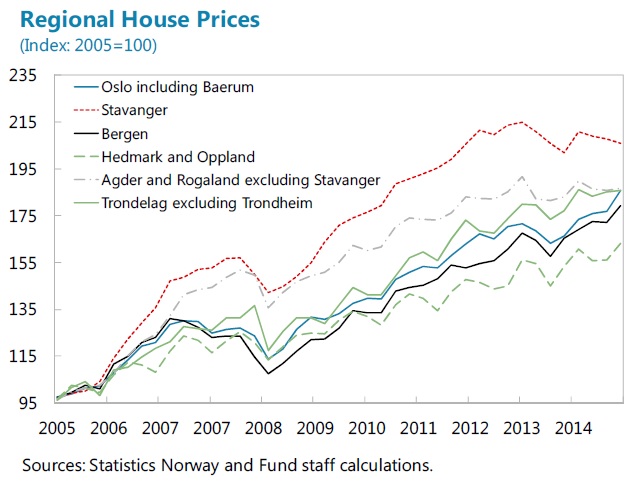

Rising House Prices and Household Debt: A Twin Boom in Norway?

“The Norwegian housing market was only moderately affected by the global financial crisis, and the rising trend of house prices resumed shortly after the crisis. In the meantime, household debt reached more than 200 percent of disposable income, and it is expected to grow further”, a new IMF paper examines the characteristics of household debt and the factors driving the housing boom and debt accumulation. The paper also examines the potential macroeconomic impact of a possible house price correction. Read the full article…

Posted by at 9:00 AM

Labels: Global Housing Watch

Subscribe to: Posts