Monday, August 17, 2015

China: How Big Is the Risk of a Real Estate Slowdown and Does It Matter?

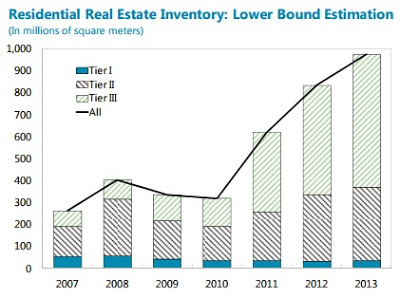

How big is the risk of a real estate slowdown? The report says:

“All indicators point to weakness in China’s housing market. Housing prices have been moderating both at the national level and across all city tiers, with the weakest performance among the smaller cities. (…) Housing inventory ratio—floor space unsold to floor space sold—shows a buildup since 2013, suggesting oversupply. Even though there is uncertainty regarding the level (National Bureau of Statistics (NBS) data show inventory of four months, while data from local housing bureaus suggest higher than two years), the direction of the buildup is clear. Inventory is especially high in Tier 3 and Tier 4 cities.”

Does it matter? The report says:

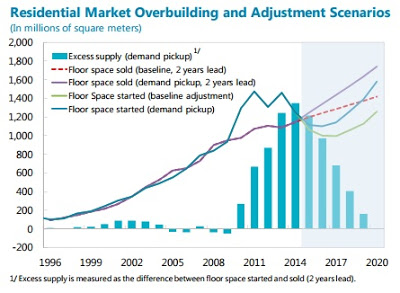

“Continued adjustment in floor space starts is warranted to let demand catch up with supply. (…) The adjustment will have significant impact on GDP growth. Given the estimated relationship between growth in floor space starts and in real estate gross fixed capital formation (GFCF), real estate GFCF could slow to -2 to -4 percent in 2015 from about 3 percent in 2014. As real estate GFCF accounts for about 9 percent of GDP, this would imply a drop of GDP growth by about ½ percentage point in the baseline scenario. This abstracts from the indirect effect arising from real estate linkages to upstream and downstream sectors. Some of these sectors suffer from oversupply, and a slowdown in construction activity could bring losses, exposing vulnerabilities and posing risks (…).”

“China’s housing market has softened visibly since 2014, reflecting oversupply in most cities. More adjustment is likely”, says the IMF’s latest report.

How big is the risk of a real estate slowdown? The report says:

“All indicators point to weakness in China’s housing market. Housing prices have been moderating both at the national level and across all city tiers, with the weakest performance among the smaller cities. (…) Housing inventory ratio—floor space unsold to floor space sold—shows a buildup since 2013,

Posted by at 9:00 AM

Labels: Global Housing Watch

Friday, August 14, 2015

Johan Norberg: India Awakes

At an event at Cato, Norberg said that “India is waking up because the government is starting to take a nap every now and then (imposing fewer regulations)”.

“What you can do and at what price matters more than who you are or what caste,” said Norberg.

“It’s morning in India but that is when the work day begins.”

India has set the goal of being in the top 50 countries in the World Bank’s Doing Business Index. Today it is at number 142 out of 189 countries.

A lesser known fact about Norberg is that he helped me inaugurate the IMF’s Book Forum: the topic was “Capitalism and its Critics”. The transcript makes for very interesting and prescient reading today – all the speakers (Jerry Muller, Ann Florini and Norberg) brought their ‘A’ game. For a short summary of the event click here.

Since 1991, 250 million people have been lifted out of poverty in India. Johan Norberg’s documentary India Awakes discusses how this happened.

It used to be said that Indians succeeded everywhere except in India. Now Indians are starting to succeed in India.

At an event at Cato, Norberg said that “India is waking up because the government is starting to take a nap every now and then (imposing fewer regulations)”.

“What you can do and at what price matters more than who you are or what caste,”

Posted by at 5:50 PM

Labels: Profiles of Economists

Recent Labor Market Reforms in Spain: A Preliminary Assessment

“The 2012 labor market reforms are making a difference. Wage moderation is contributing to a visible recovery in headline employment growth, and the reforms have made the labor market more resilient to shocks. There is also some evidence that the contribution of temporary contracts to employment growth has started to decrease. However, the reliance on temporary workers remains strong overall and further structural reforms will be required to reduce the still very high level of long-term, structural unemployment.”

From a new IMF study:

“The 2012 labor market reforms are making a difference. Wage moderation is contributing to a visible recovery in headline employment growth, and the reforms have made the labor market more resilient to shocks. There is also some evidence that the contribution of temporary contracts to employment growth has started to decrease. However, the reliance on temporary workers remains strong overall and further structural reforms will be required to reduce the still very high level of long-term,

Posted by at 5:25 PM

Labels: Inclusive Growth

Wednesday, August 12, 2015

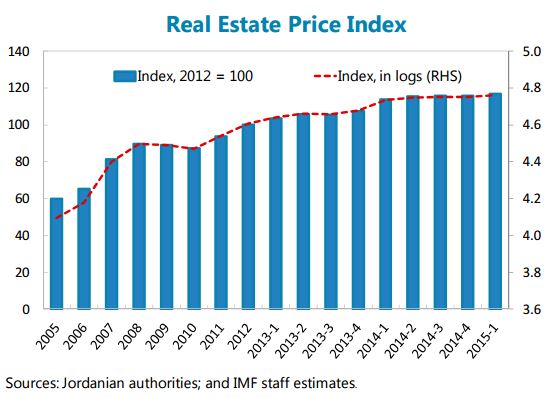

House Prices in Jordan

“Mortgages slowed down in tandem with real estate prices; exposure of banks to real estate credit risk has remained limited”, notes the latest IMF report on Jordan.

Posted by at 9:00 AM

Labels: Global Housing Watch

Monday, August 10, 2015

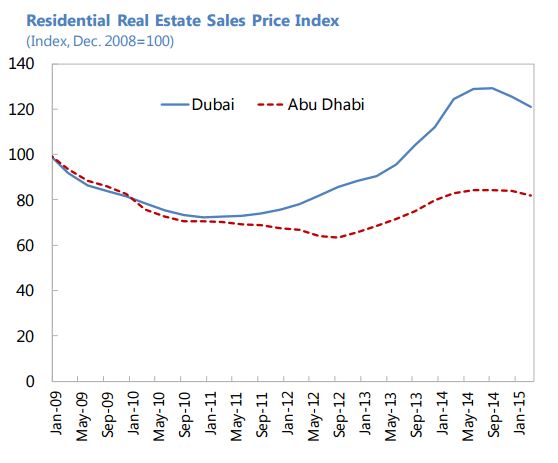

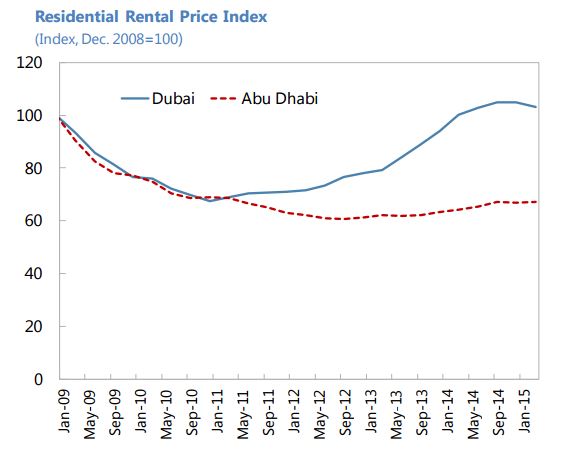

House Prices in United Arab Emirates

“The real estate market in the UAE has cooled down after expanding strongly in 2013 and the first half of 2014. By end-2014, sales price increases moderated in Dubai and Abu Dhabi, and in March 2015, growth in residential sales prices turned slightly negative in both Emirates, in year-on-year terms (…). These developments are taking place amid increased supply, particularly in Dubai, and reduced demand associated with lower oil prices and appreciating US dollar, and following the introduction of mortgage regulations based on loan-to-value ratios and an increase in the property transfer fee in late 2013. Read the full article…

Posted by at 9:00 AM

Labels: Global Housing Watch

Subscribe to: Posts