Wednesday, August 3, 2016

Japan: Minimum wages as a policy tool

A new IMF report discusses whether increases in the minimum wage in Japan will succeed in raising wage growth. It concludes: “In order to revamp growth and permanently exit deflation, Japan needs vigorous wage growth. The government has recognized this and announced substantial increases in the minimum wage and we empirically estimate its impact on average wages. Our econometric results suggest that the 3 percent hourly minimum wage increase could cause monthly wages to increase by about 1.5 percent on a year-on-year basis. The minimum wage policy should be complemented by other income policies—e.g. a “soft target” for wage growth and increases in public wages to create cost-push pressures in line with the inflation target.”

A new IMF report discusses whether increases in the minimum wage in Japan will succeed in raising wage growth. It concludes: “In order to revamp growth and permanently exit deflation, Japan needs vigorous wage growth. The government has recognized this and announced substantial increases in the minimum wage and we empirically estimate its impact on average wages. Our econometric results suggest that the 3 percent hourly minimum wage increase could cause monthly wages to increase by about 1.5 percent on a year-on-year basis.

Posted by at 10:45 AM

Labels: Inclusive Growth

Tuesday, August 2, 2016

Labor Mobility in the United States

The United States has always been regarded as a highly mobile society. Previous work has left the impression that when adverse economic shocks hit their cities or regions, Americans are quickly able to move and find jobs elsewhere within the country. In a new paper, Mai Dao, Davide Furceri and I provide new evidence that questions this view. Our evidence shows that the ability to migrate is not as immediate as previously supposed; in the first year or two after an adverse shock to a state, the bulk of the burden is borne by an increase in the state unemployment and a decline in its labor force participation rate. We also find that while net mobility across states picks up during national recessions, this increase is driven more by a stronger population inflow into states that are doing better rather than stronger population outflow from states that are doing worse; the outflow occurs only toward the end of the recession. Overall, therefore, our results offer a less sanguine view of the ability of U.S. workers to shield themselves from the consequences of adverse shocks than is available in the literature. Here is a link to the paper and to an online appendix which is a wonk’s delight.

The United States has always been regarded as a highly mobile society. Previous work has left the impression that when adverse economic shocks hit their cities or regions, Americans are quickly able to move and find jobs elsewhere within the country. In a new paper, Mai Dao, Davide Furceri and I provide new evidence that questions this view. Our evidence shows that the ability to migrate is not as immediate as previously supposed; in the first year or two after an adverse shock to a state,

Posted by at 4:40 PM

Labels: Inclusive Growth

Okun’s Law: Fit at 55?

In a revised version of our 2013 paper, Larry Ball, Daniel Leigh and I still conclude: “It is rare to call a macroeconomic relationship a “law.” Yet we believe that Okun’s Law has earned its name. It is not as universal as the law of gravity (which has the same parameters in all advanced economies), but it is strong and stable by the standards of macroeconomics. Reports of deviations from the Law are often exaggerated. Okun’s Law is certainly more reliable than a typical macro relationship like the Phillips curve, which is constantly under repair as new anomalies arise in the data.” The paper provides estimates of Okun’s Law for 20 advanced economies, including the United States.

In a revised version of our 2013 paper, Larry Ball, Daniel Leigh and I still conclude: “It is rare to call a macroeconomic relationship a “law.” Yet we believe that Okun’s Law has earned its name. It is not as universal as the law of gravity (which has the same parameters in all advanced economies), but it is strong and stable by the standards of macroeconomics. Reports of deviations from the Law are often exaggerated.

Posted by at 4:13 PM

Labels: Inclusive Growth

Monday, August 1, 2016

Real Estate Market in Ireland

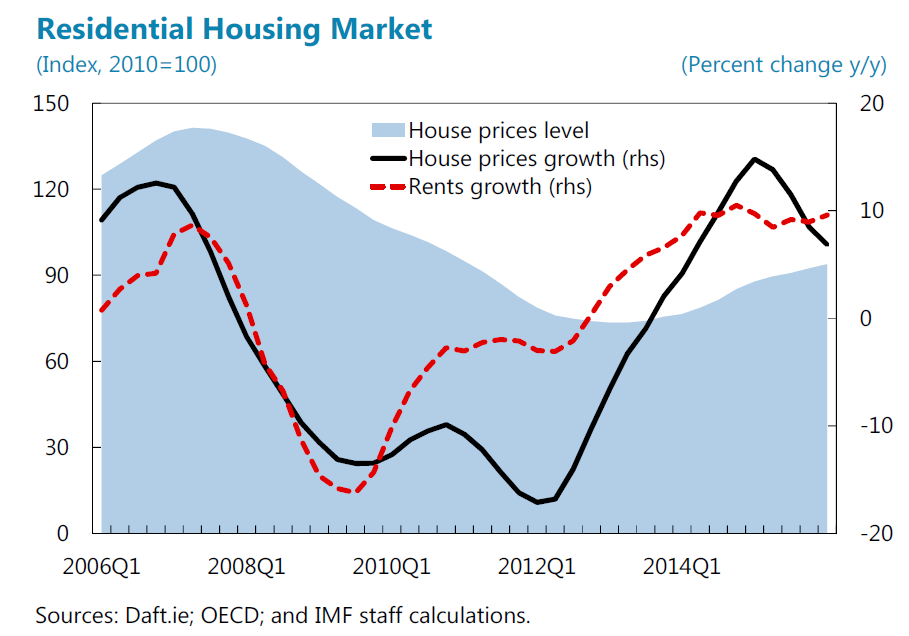

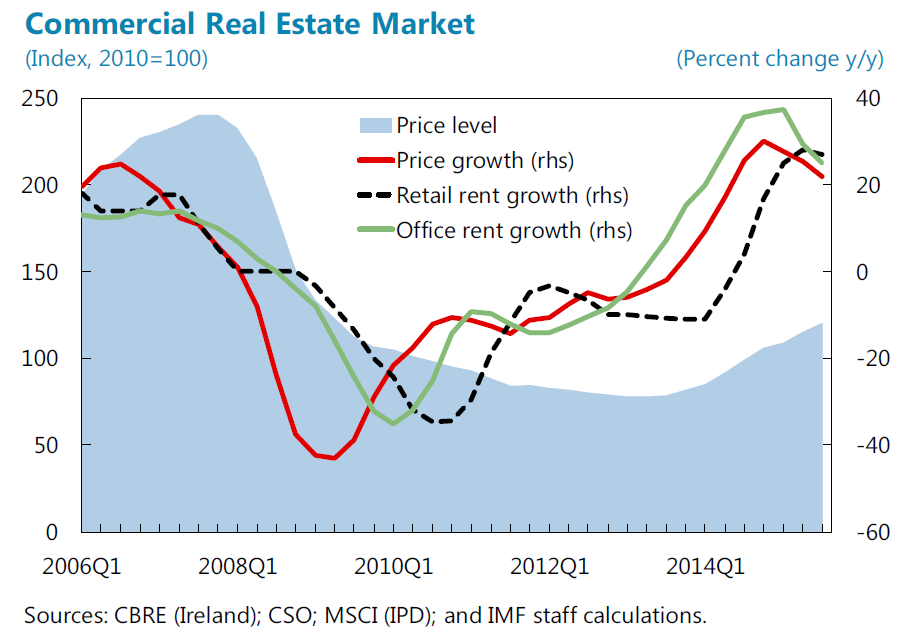

“Residential real estate (RRE) prices and rents continued to increase. Nevertheless, following the abolishment of tax exemptions on capital gains in December 2014 and the introduction of new macroprudential loan-to-value (LTV) and loan-to-income (LTI) limits in February 2015 (…), the market somewhat cooled off: RRE price growth decelerated in late 2015 and the number of mortgage approvals temporarily declined (…). [Meanwhile,] Commercial real estate (CRE) prices rose even more rapidly. Total returns of the Irish CRE sector outstripped those of other European countries, reflecting the confluence of strong equity investment largely financed by foreigners in search for high yield, and still limited new construction”, says IMF’s report on Ireland.

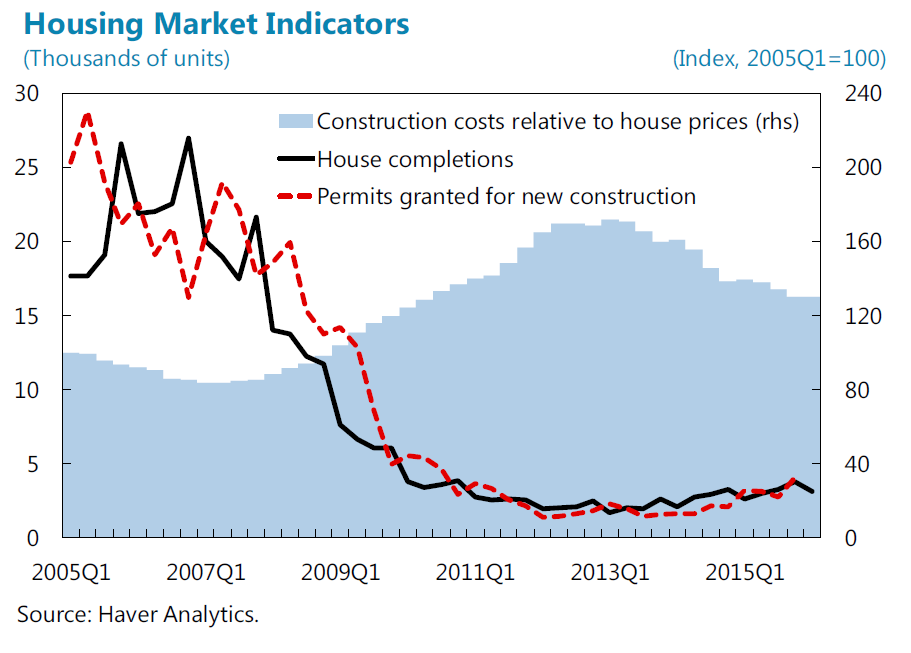

On housing supply, the report says that “Boosting the housing supply would help mitigate property price and rent pressures. The sluggish construction activity in recent years reflects the sector’s downsizing after the bursting of the property market bubble in 2008-09 and the ensuing limited access to finance for companies. High construction costs due to strict planning requirements have also been a factor. In response to mounting pressures in the housing market, the government introduced a package of measures in November 2015, including rebates for housing construction schemes that meet certain criteria, and new planning guidelines, which seek to reduce the building costs.16 Additionally, the National Asset Management Agency (NAMA), within its mandate, is to fund the delivery of 20,000 residential units by 2020. Staff stressed that additional policy actions should help expedite new construction, and welcomed the authorities’ intent to publish an Action Plan for Housing over the summer.”

There is also a separate report on commercial real estate.

“Residential real estate (RRE) prices and rents continued to increase. Nevertheless, following the abolishment of tax exemptions on capital gains in December 2014 and the introduction of new macroprudential loan-to-value (LTV) and loan-to-income (LTI) limits in February 2015 (…), the market somewhat cooled off: RRE price growth decelerated in late 2015 and the number of mortgage approvals temporarily declined (…). [Meanwhile,] Commercial real estate (CRE) prices rose even more rapidly. Total returns of the Irish CRE sector outstripped those of other European countries,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, July 28, 2016

Housing Market in United Arab Emirates

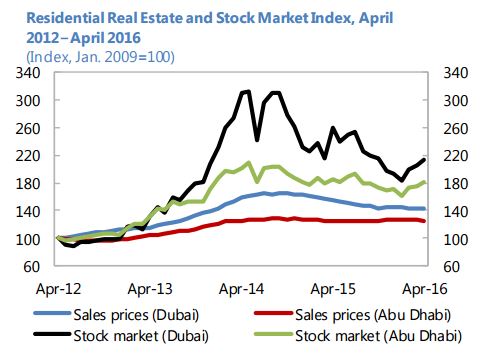

“Real estate prices have continued to decline, but the quality of the real estate loan portfolio has remained resilient. Structural measures taken in 2014, such as the tightening of industry self-regulation, higher real estate fees, and tighter macroprudential regulation for mortgage lending, have helped contain speculative demand for real estate and led to declining prices. This trend has continued with Dubai’s real estate average residential prices falling by 11 percent in 2015, also reflecting oversupply and strong headwinds on demand. In Abu Dhabi where the supply growth slowed, they fell by 0.8 percent. However, these developments do not appear to pose systemic risks for the financial sector, as the nonperforming loans for construction and real estate development declined from 12.3 percent in 2013 to 7.5 percent by end-March 2016. Similar improvements have been experienced for loans to households with NPLs ratio down from 10 to 4.9 percent over the same period”, according to the IMF’s report on United Arab Emirates.

“Real estate prices have continued to decline, but the quality of the real estate loan portfolio has remained resilient. Structural measures taken in 2014, such as the tightening of industry self-regulation, higher real estate fees, and tighter macroprudential regulation for mortgage lending, have helped contain speculative demand for real estate and led to declining prices. This trend has continued with Dubai’s real estate average residential prices falling by 11 percent in 2015, also reflecting oversupply and strong headwinds on demand.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts