Monday, July 31, 2017

Housing Market in Singapore

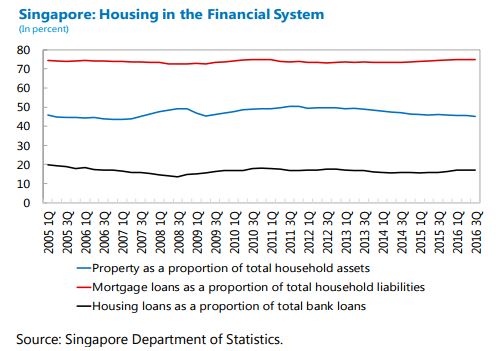

A new IMF report on Singapore says that: “In Singapore, property market stability is closely linked to macroeconomic and financial stability. Property is the largest component of household wealth, representing about half of total household assets. Mortgage loans account for some three-quarters of total household liabilities, and property-related loans form a substantial portion of banks’ loan books. In addition, housing affordability is a key concern for the Singapore public (Lum, 1996 and 2011; Phang, 2015; Phang and others, 2013). Therefore, when property prices rose rapidly shortly after the Global Financial Crisis (GFC), the Singapore authorities responded with a series of macroprudential measures, including fiscal-based measures, to promote a more stable and sustainable property market. ”

The report also says that: “Finally, Singapore’s banks are well-positioned to withstand shocks from the property market, partly as a result of macro-prudential tightening. Average loan-to-value ratios are low, loan-loss coverage is adequate, and capital and liquidity buffers are strong. Households also have healthy balance sheets and well-diversified assets. ”

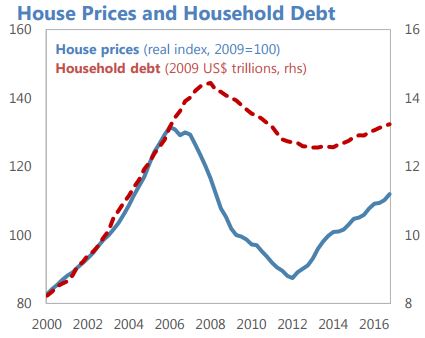

On international comparison, the report says that “In Hong Kong SAR, Singapore, and Taiwan Province of China, property tightening measures in recent years have achieved different results. Since peaking in 2013, house prices in Singapore have declined gradually to 2010 levels. The impact contrasts with Hong Kong SAR, where prices have continued to rise and mortgage growth has shown no clear downward trend. House price growth has also remained rapid in New Zealand and Australia where tightening began in 2013 and 2014 respectively. Hence, there is significant liquidity in the regional markets calling for continued vigilance and careful calibration of the measures to guard against speculative capital inflows that can hamper financial stability.”

A new IMF report on Singapore says that: “In Singapore, property market stability is closely linked to macroeconomic and financial stability. Property is the largest component of household wealth, representing about half of total household assets. Mortgage loans account for some three-quarters of total household liabilities, and property-related loans form a substantial portion of banks’ loan books. In addition, housing affordability is a key concern for the Singapore public (Lum, 1996 and 2011;

Posted by at 11:41 AM

Labels: Global Housing Watch

Friday, July 28, 2017

Housing in the U.S.

The IMF’s latest report on the U.S. says that: “After a prolonged deleveraging, the housing sector is showing healthy growth.”

The IMF’s latest report on the U.S. says that: “After a prolonged deleveraging, the housing sector is showing healthy growth.”

Posted by at 3:36 PM

Labels: Global Housing Watch

A Profile of Assaf Razin

Below is an extract from the Jerusalem Post:

“In 1924, the late English economist John Maynard Keynes deliberated on what makes a great economist: “The master-economist … must be mathematician, historian, statesman, philosopher—in some degree. He must understand symbols and speak in words. He must contemplate the particular in terms of the general and touch abstract and concrete in the same flight of thought. He must study the present in the light of the past for the purposes of the future.”

Keynes was eulogizing a colleague economist who passed 17 years before Israeli economist Assaf Razin was born in 1941. However, if you ask colleagues and students, Keynes’ words could have been describing the ideal this 2017 EMET Prize winner for social sciences aspires to achieve.

Razin studied and shared ideas about globalization before many modern commentators on the subject even heard of the word, according to Prakash Loungani, an adviser at the International Monetary Fund. Migration and its impact on welfare states, economic policies that would have to shift in a world that is smaller and more accessible – “All the issues we are dealing with now, he was writing about all of it 20 or 30 years ago,” said Loungani.

Razin’s accomplishments are most surprising, considering his upbringing in Kibbutz Shamir in the Upper Galilee. He was born to a family of modest means with Marxist ideals. The professor describes his life as one of extremes – from the kibbutz to Tel Aviv University; from Israel to different parts of the world; and from his childhood in the nursery bed of socialism to the Economics Department at the University of Chicago, the cradle of intellectual capitalism, from where he received his Ph.D. in economics.”

Despite some rather dramatic personal events, including the death of his son in 1996 at the age of 30, Razin’s academic and professional achievements are truly outstanding, said Lars E.O. Svensson, a professor in the Stockholm School of Economics.

“Assaf has an excellent standing in the international community of scholars,” said Svensson. “He is a most welcome visitor to universities, research institutes and international organizations all over the world, and he is a high appreciated participant in international conferences.”

Continue reading here.

ASSAF RAZIN. (photo credit:Courtesy)

Below is an extract from the Jerusalem Post:

“In 1924, the late English economist John Maynard Keynes deliberated on what makes a great economist: “The master-economist … must be mathematician, historian, statesman, philosopher—in some degree. He must understand symbols and speak in words. He must contemplate the particular in terms of the general and touch abstract and concrete in the same flight of thought. He must study the present in the light of the past for the purposes of the future.”

Keynes was eulogizing a colleague economist who passed 17 years before Israeli economist Assaf Razin was born in 1941.

Posted by at 6:31 AM

Labels: Profiles of Economists

Housing View – July 28, 2017

On cross-country:

- Why Jimmy Carter Believes Housing Is a Basic Human Right – Citylab

- When the (Empty) Apartment Next Door Is Owned by an Oligarch – New York Times

- ¿Por qué las ciudades se vuelven incosteables? – El Economista

- The impact of oil shocks on the housing market: Evidence from Canada and U.S – Journal of Economics and Business

On the US:

- Having Shed Young Workers, the Construction Industry Needs Change – BuildZoom

- The Toughest Places to Build: Behind the Scenes of a Wall Street Journal Analysis – BuildZoom

- Inventory Myth Busting: Why is Home Inventory So Low? – Trulia

- Housing Prices: Highs and Lows – Conversable Economist

- We’re Finally Building More Small Homes, but Construction Remains at Historically Low Levels – Harvard Joint Center for Housing Studies

- Housing Shortage: Where is the Undersupply of New Construction Worst? – Apartment List

- Echoes of Rising Tuition in Students’ Borrowing, Educational Attainment, and Homeownership in Post-Recession America – Federal Reserve Bank of New York

- A promising new coalition looks to rewrite the politics of urban housing – Vox

- Boosting Taxes for Boasting about Houses: Status Concerns in the Housing Market – TU Wien

- Study: Tax subsidies like the mortgage interest deduction have ‘zero effect on homeownership’ – American Enterprise Institute

- These four trends in rental housing have big implications for the growing affordable housing crisis – Urban Institute

On other countries:

- [Canada] Housing Market Assessment — CMHC

On cross-country:

- Why Jimmy Carter Believes Housing Is a Basic Human Right – Citylab

- When the (Empty) Apartment Next Door Is Owned by an Oligarch – New York Times

- ¿Por qué las ciudades se vuelven incosteables? – El Economista

- The impact of oil shocks on the housing market: Evidence from Canada and U.S – Journal of Economics and Business

On the US:

- Having Shed Young Workers,

Posted by at 6:16 AM

Labels: Global Housing Watch

Thursday, July 27, 2017

Why economists cannot forecast recessions

A new article by Alasdair Macleod quoted my research: “Loungani was recently interviewed for a BBC programme, updating his original paper. In that interview, he claimed that over three decades, of the 150 recessions recorded only two had been forecast, implying that since the turn of the century no recessions had been forecast at all.ii The failure rate has increased to 100%, not decreased, as might be expected from economic models that are updated in the light of experience.”

Continue reading here.

A new article by Alasdair Macleod quoted my research: “Loungani was recently interviewed for a BBC programme, updating his original paper. In that interview, he claimed that over three decades, of the 150 recessions recorded only two had been forecast, implying that since the turn of the century no recessions had been forecast at all.ii The failure rate has increased to 100%, not decreased, as might be expected from economic models that are updated in the light of experience.”

Posted by at 6:43 PM

Labels: Forecasting Forum

Subscribe to: Posts