Tuesday, March 13, 2018

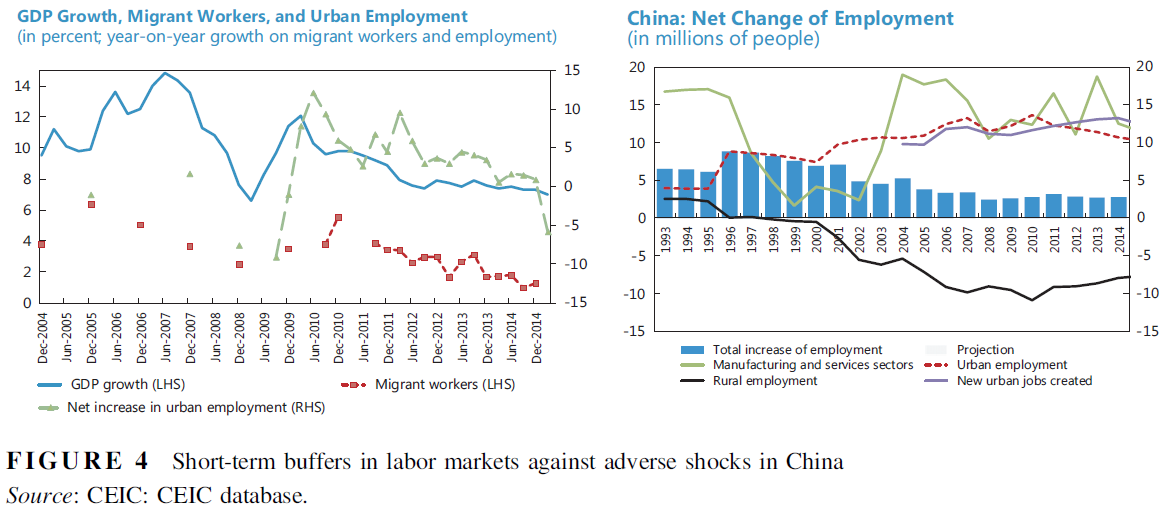

Okun’s Law in China: Understanding China’s Labor Market Resilience

From a new paper on China’s labor market:

“A stable labor market is a policy priority for most countries, especially after the burst of the global financial crisis. Unlike most countries, the labor market in China appears to be holding up well, despite sharp slowdown in economic growth. This paper argues that there are underlying fundamental mechanisms that help explain the resilience of China’s labor market. The key to understanding labor market dynamics in China is that rural-to-urban migrant flows are more sensitive to growth than urban workers in the process of fast urbanization, which serves as a main shock absorber to buffer employment against adverse shocks. Therefore, we propose a generalized Okun’s Law (GOL) that incorporates migrant flows with unemployment rates to capture the relation between labor market dynamics and economic cycles. The original Okun’s Law can be regarded as a special case of the GOL for developed countries that have already completed urbanization. Conducting empirical analysis with both China’s national- and city-level data and cross-country panel data, we find strong evidence supporting the GOL theory. Findings in the paper have implications for a deeper understanding of the wisdom of Okun’s Law and its application in labor market policies.”

From a new paper on China’s labor market:

“A stable labor market is a policy priority for most countries, especially after the burst of the global financial crisis. Unlike most countries, the labor market in China appears to be holding up well, despite sharp slowdown in economic growth. This paper argues that there are underlying fundamental mechanisms that help explain the resilience of China’s labor market. The key to understanding labor market dynamics in China is that rural-to-urban migrant flows are more sensitive to growth than urban workers in the process of fast urbanization,

Posted by at 9:26 AM

Labels: Inclusive Growth

Monday, March 12, 2018

Can Central Bankers Become Superforecasters?

From a new post by Aakash Mankodi and Tim Pike:

“Tetlock and Gardner’s acclaimed work on Superforecasting provides a compelling case for seeing forecasting as a skill that can be improved, and one that is related to the behavioural traits of the forecaster. These so-called Superforecasters have in recent years been pitted against experts ranging from U.S intelligence analysts to participants in the World Economic Forum, and have performed on par or better by accurately predicting the outcomes of a broad range of questions. Sounds like music to a central banker’s ears? In this post, we examine the traits of these individuals, compare them with economic forecasting and draw some related lessons. We conclude that considering the principles and applications of Superforecasting can enhance the work of central bank forecasting.

[…]

With continuous forecasting challenges on the horizon in coming years, perhaps it is an opportune time to incorporate these ideas in the central banking sphere. Economic forecasting will always be an imperfect science. So while it is unlikely that a major shock such as the global financial crisis would have been averted by improving the accuracy of forecasting efforts in these ways, we believe the lessons learnt through the experiment of Superforecasting have a lot to offer to take forecasting a step forward in that direction. Potentially over time, we might be able to create a next generation of central bank Superforecasters.”

From a new post by Aakash Mankodi and Tim Pike:

“Tetlock and Gardner’s acclaimed work on Superforecasting provides a compelling case for seeing forecasting as a skill that can be improved, and one that is related to the behavioural traits of the forecaster. These so-called Superforecasters have in recent years been pitted against experts ranging from U.S intelligence analysts to participants in the World Economic Forum,

Posted by at 9:10 AM

Labels: Forecasting Forum

The time series figures for the most basic of business cycle macro analyses: What is to be explained and accounted for

Posted by at 7:37 AM

Labels: Macro Demystified

Sunday, March 11, 2018

Economic Forecasts with the Yield Curve

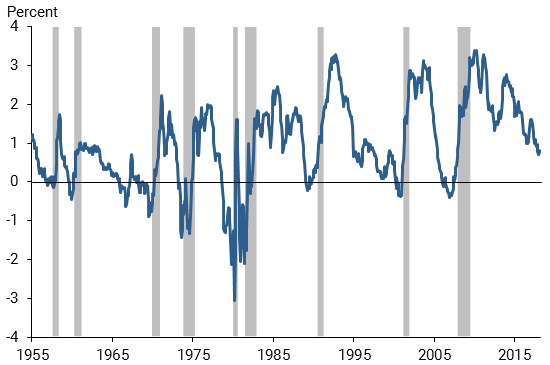

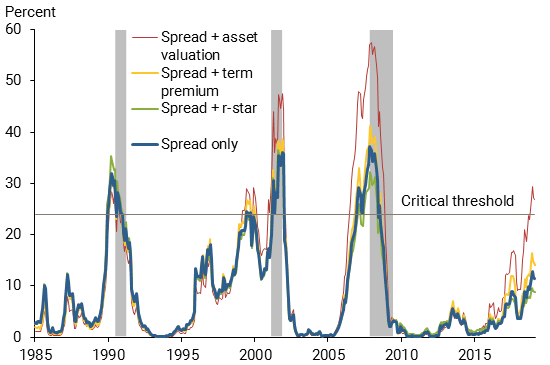

From the Federal Reserve Bank of San Francisco:

“Forecasting future economic developments is a tricky business, but the term spread has a strikingly accurate record for forecasting recessions. Periods with an inverted yield curve are reliably followed by economic slowdowns and almost always by a recession. While the current environment appears unique compared with recent economic history, statistical evidence suggests that the signal in the term spread is not diminished. These findings indicate concerns about the scenario of an inverting yield curve. Any forecasts that include such a scenario as the most likely outcome carry the risk that an economic slowdown might follow soon thereafter.”

Figure 1

The term spread and recessions

Note: Gray bars indicate NBER recession dates.

Figure 2

Estimated probabilities of recession based on term spread

Note: Gray bars indicate NBER recession dates.

From the Federal Reserve Bank of San Francisco:

“Forecasting future economic developments is a tricky business, but the term spread has a strikingly accurate record for forecasting recessions. Periods with an inverted yield curve are reliably followed by economic slowdowns and almost always by a recession. While the current environment appears unique compared with recent economic history, statistical evidence suggests that the signal in the term spread is not diminished.

Posted by at 9:46 AM

Labels: Macro Demystified

Saturday, March 10, 2018

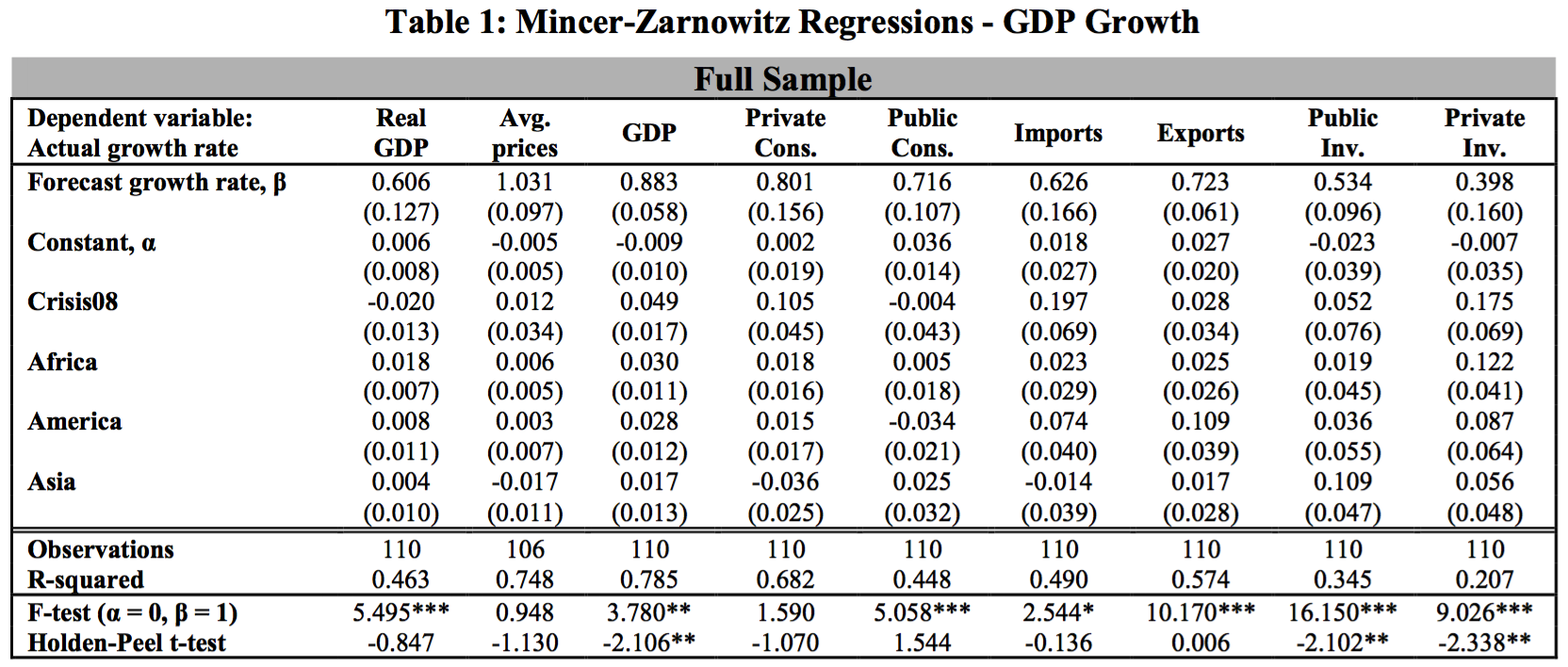

Forecasts in Times of Crises

From a new IMF working paper:

“Financial crises pose unique challenges for forecast accuracy. Using the IMF’s Monitoring of Fund Arrangement (MONA) database, we conduct the most comprehensive evaluation of IMF forecasts to date for countries in times of crises. We examine 29 macroeconomic variables in terms of bias, efficiency, and information content to find that IMF forecasts add substantial informational value as they consistently outperform naive forecast approaches. However, we also document that there is room for improvement: two thirds of the key macroeconomic variables that we examine are forecast inefficiently and 6 variables (growth of nominal GDP, public investment, private investment, the current account, net transfers, and government expenditures) exhibit significant forecast bias. Forecasts for low-income countries are the main drivers of forecast bias and inefficiency, reflecting perhaps larger shocks and lower data quality. When we decompose the forecast errors into their sources, we find that forecast errors for private consumption growth are the key contributor to GDP growth forecast errors. Similarly, forecast errors for non-interest expenditure growth and tax revenue growth are crucial determinants of the forecast errors in the growth of fiscal budgets. Forecast errors for balance of payments growth are significantly influenced by forecast errors in goods import growth. The results highlight which macroeconomic aggregates require further attention in future forecast models for countries in crises.”

From a new IMF working paper:

“Financial crises pose unique challenges for forecast accuracy. Using the IMF’s Monitoring of Fund Arrangement (MONA) database, we conduct the most comprehensive evaluation of IMF forecasts to date for countries in times of crises. We examine 29 macroeconomic variables in terms of bias, efficiency, and information content to find that IMF forecasts add substantial informational value as they consistently outperform naive forecast approaches. However,

Posted by at 10:57 PM

Labels: Forecasting Forum

Subscribe to: Posts