Friday, April 6, 2018

Impact of Monetary Policy on Luxembourg

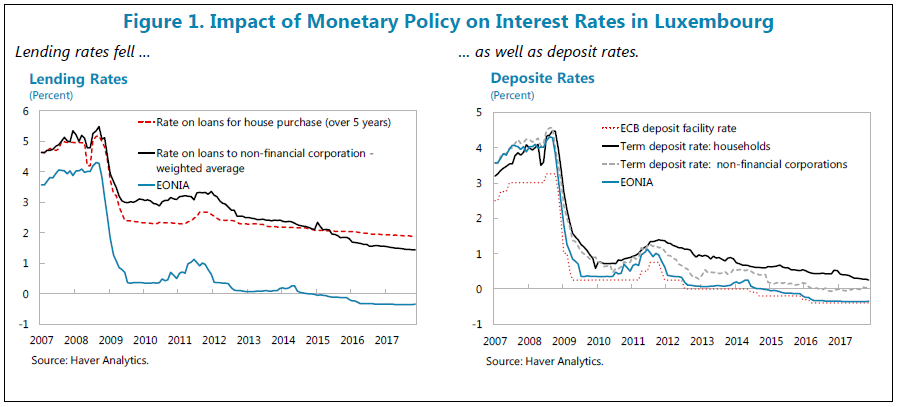

A new IMF report says that “Accommodative monetary policy has contributed to the performance of the Luxembourg economy through some expansion of aggregate demand and through its impact on the financial system. Banks have remained profitable and interest margins stable, while fee and commission income from fund and other activity has been healthy. The investment fund industry has benefited from various factors such as portfolio rebalancing, search for yield, and other market developments leading to strong inflows into various classes of investment funds, and through strong valuation effects. Scenario analysis suggest that the fund industry could be adversely impacted by sharp interest rate increases and that, because of interconnections, the banking system would also be affected. Margins of some banks could also decline when interest rate normalize. Against this backdrop, it is important to implement all 2017 FSAP recommendations that will contribute to making the financial system more resilient to shocks, including those arising from faster-than-expected monetary policy normalization.”

Continue reading here.

A new IMF report says that “Accommodative monetary policy has contributed to the performance of the Luxembourg economy through some expansion of aggregate demand and through its impact on the financial system. Banks have remained profitable and interest margins stable, while fee and commission income from fund and other activity has been healthy. The investment fund industry has benefited from various factors such as portfolio rebalancing, search for yield, and other market developments leading to strong inflows into various classes of investment funds,

Posted by at 1:13 PM

Labels: Inclusive Growth

Housing View – April 6, 2018

On cross-country:

- European Mortgage Markets Quarterly Review – European Covered Bond Council

- Singapore’s private-public housing mix could offer solutions for Toronto and Vancouver – The Globe and Mail

- Financial cycles in euro area economies: a cross-country perspective – Deutsche Bundesbank

On the US:

- Quantities and Prices during the Housing Bust – Federal Reserve Bank of New York

- Characteristics of Domestic Cross-Metropolitan Migrants – BuildZoom

- San Diego’s Mexican property market at risk from Trump tariffs – Financial Times

- House Price Markups and Mortgage Defaults – Federal Housing Finance Agency

- Case-Shiller – A surprise in the bottom 3 cities – Real Estate Decoded

- The Unfulfilled Promise of Fair Housing – The Atlantic

- Housing Wealth, Health and Deaths of Despair – IESE Business School

- Nearly two-thirds of renters say they can’t afford to buy a home – Wall Street Journal

On other countries:

- [Botswana] Housing delivery to the low income in Botswana – Emerald Insight

- [China] Housing conditions and life satisfaction in urban China – Cities

- [China] Accounting for China’s real estate boom – Financial Times

- [China] Macro-economic index effect on house prices in China – Universiti Teknologi Malaysia

- [China] Has Monetary Policy Caused Housing Price to Rise or Fall in China? – The Singapore Economic Review

- [China] Exploring the relationship between urban land supply and housing stock: Evidence from 35 cities in China – Habitat International

- [France] Taxing Vacant Dwellings: Can fiscal policy reduce vacancy? – RePec

- [Hong Kong] The impact of government housing policy and development controls on the dynamics of Hong Kong’s residential property market – The Hong Kong Polytechnic University

- [Italy] Average Time to Sell a Property and Credit Conditions: Evidence from the Italian Housing Market Survey – LUISS Guido Carli

- [Vietnam] Vietnam’s rapid growth fuels Ho Chi Minh property boom – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- European Mortgage Markets Quarterly Review – European Covered Bond Council

- Singapore’s private-public housing mix could offer solutions for Toronto and Vancouver – The Globe and Mail

- Financial cycles in euro area economies: a cross-country perspective – Deutsche Bundesbank

On the US:

- Quantities and Prices during the Housing Bust – Federal Reserve Bank of New York

- Characteristics of Domestic Cross-Metropolitan Migrants – BuildZoom

- San Diego’s Mexican property market at risk from Trump tariffs – Financial Times

- House Price Markups and Mortgage Defaults – Federal Housing Finance Agency

- Case-Shiller – A surprise in the bottom 3 cities – Real Estate Decoded

- The Unfulfilled Promise of Fair Housing – The Atlantic

- Housing Wealth,

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, April 5, 2018

House Prices in Mongolia

The IMF’s latest report on Mongolia says that “(…) housing prices stabilized after years of deflation, in line with stronger economic activity and household lending.”

The IMF’s latest report on Mongolia says that “(…) housing prices stabilized after years of deflation, in line with stronger economic activity and household lending.”

Posted by at 10:40 AM

Labels: Global Housing Watch

Wednesday, April 4, 2018

Housing Market in Luxembourg: Assessment and Policy Recommendations

From the IMF’s latest report on Luxembourg:

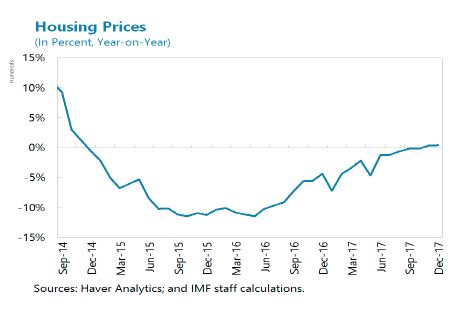

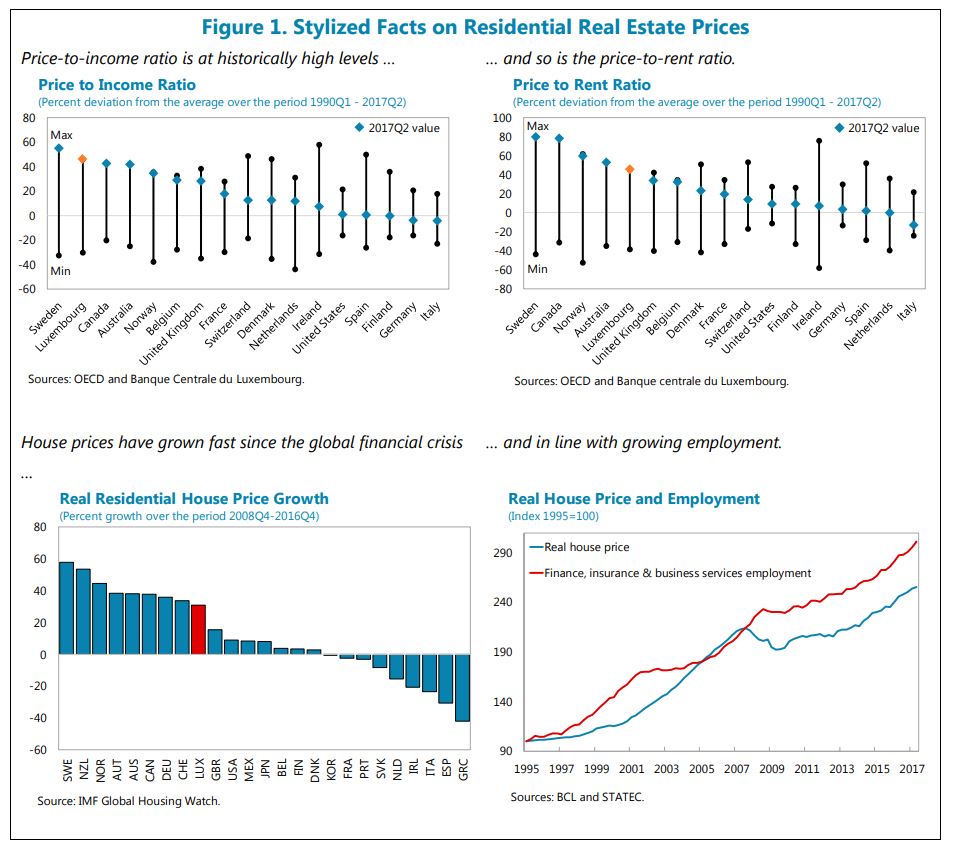

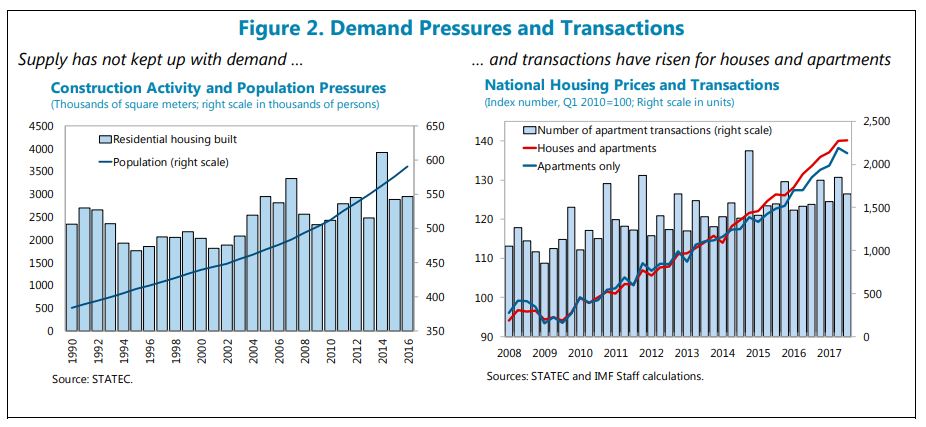

“Demand for housing has exceeded supply for many years. While house prices are in line with fundamentals, they have risen faster than disposable income for years, largely because of structural supply constraints in the context of strong demand, in part reflecting net demographic growth. The dynamics of house prices is also somewhat affected by cyclical factors such as the cost of construction and to some extent the low interest rate environment. Rigid zoning and administrative rules together with land hoarding prevent sufficient construction, while tax incentives and subsidies fuel demand. Reduced affordability has driven up household indebtedness, in particular among younger households.

Risks in the real estate market should continue to be closely monitored, and further actions taken as needed. Recent measures have appropriately built capital buffers in the banking system while discouraging riskier lending. However, household debt is relatively high and limits to debt-service-to-income ratios should be set if house prices continue to outpace disposable incomes. Going forward, the normalization of interest rates could add to the debt service of some households (who borrowed at variable rates) while banks’ margins on their stock of fixed rate mortgages would shrink.

Containing house price pressures and alleviating bottlenecks of housing require a strong effort to expand the stock of housing:

- Excessive red tape in bringing additional land to construction should be pruned, and incentives strengthened. The initiatives of Baulücken for new construction are a step in the right direction;

- Local zoning decisions should be better coordinated with a national spatial development plan and cooperation among municipalities should be encouraged;

- Existing tools to mobilize vacant land and unoccupied dwellings could be strengthened. This includes implementing taxation on vacant lots. In this respect, the initiative of Baulandvertrag goes in the right direction;

- In the PDAT and the municipal implementation, assigning “mixed construction” land in priority to residential real estate would widen the share of land eligible for housing development;

- Tax biases at the municipality level against residential real estate should be reduced further. The reform of the distribution of municipal business taxes among municipalities is a step in the right direction as it reduces incentives favoring commercial over residential real estate zoning decisions. Going forward, policies should increase the share of the ICC redistributed in the equalization fund;

- Increasing property taxes and revising cadastral values would help municipalities increase own resources.

The share of social and affordable housing in total housing could be increased:

- To encourage social housing in the rental segment, public developers in the social sector (FSH, SNCHM, and municipalities) should be gradually steered only towards the development and management of social rentals. This would help clarify management roles and separate more clearly the rental activity from the construction-for-sale business.”

From the IMF’s latest report on Luxembourg:

“Demand for housing has exceeded supply for many years. While house prices are in line with fundamentals, they have risen faster than disposable income for years, largely because of structural supply constraints in the context of strong demand, in part reflecting net demographic growth. The dynamics of house prices is also somewhat affected by cyclical factors such as the cost of construction and to some extent the low interest rate environment.

Posted by at 4:33 PM

Labels: Global Housing Watch

Tuesday, April 3, 2018

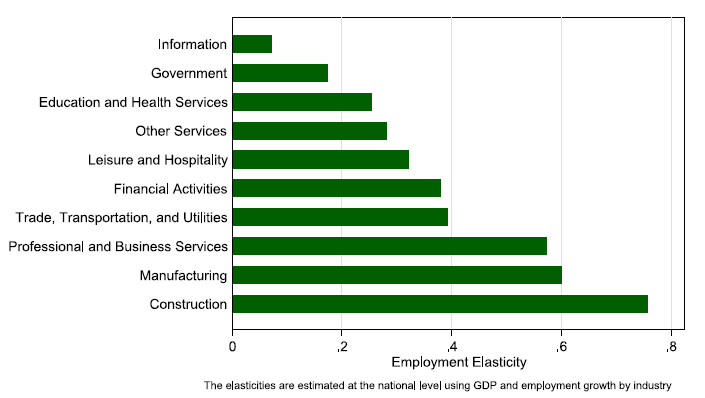

What Lies beneath? A Sub-National Look at Okun’s Law in the United States

In my new paper with Nathalie Gonzalez Prieto and Saurabh Mishra, “We find that Okun’s Law holds quite well for most U.S. states but the Okun coefficient—the responsiveness of unemployment to output—varies substantially across states. We are able to explain a significant part of this cross-state heterogeneity on the basis of the state’s industrial structure. Our results have implications for the design of state and federal policies and may also be able to explain why Okun’s Lawat the national level has remained quite stable over time despite an enormous shift in the structure of the U.S. economy from manufacturing to services.”

Fig. 3 National-level employment elasticities

Continue reading here.

In my new paper with Nathalie Gonzalez Prieto and Saurabh Mishra, “We find that Okun’s Law holds quite well for most U.S. states but the Okun coefficient—the responsiveness of unemployment to output—varies substantially across states. We are able to explain a significant part of this cross-state heterogeneity on the basis of the state’s industrial structure. Our results have implications for the design of state and federal policies and may also be able to explain why Okun’s Lawat the national level has remained quite stable over time despite an enormous shift in the structure of the U.S.

Posted by at 10:40 AM

Labels: Inclusive Growth

Subscribe to: Posts