Monday, July 30, 2018

Twin Deficits in Developing Economies

From a new IMF working paper by Davide Furceri and Aleksandra Zdzienicka:

“We provide new evidence of the existence of the “twin deficits” in developing economies. Using unanticipated government spending shocks for an unbalanced panel of 114 developing economies from 1990 to 2015, we find that a one percent of GDP unanticipated improvement in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP. This effect is substantially larger than usually found in the literature using standard measures of fiscal policy changes such as the CAB. This finding has important policy implications as for a given target of external adjustment less fiscal consolidation is required than normally assumed.

Beyond this average effect lies some heterogeneity, both across states of the business cycle and across countries. The effect tends to be larger: (i) during recessions; (ii) in countries that are more open to trade; (iii) that have less flexible exchange rate regimes; and (iv) with lower initial public debt-to-GDP ratios. This heterogeneity has far-reaching implications for policymakers in deciding the magnitude of the fiscal adjustment needed to address external imbalances.”

From a new IMF working paper by Davide Furceri and Aleksandra Zdzienicka:

“We provide new evidence of the existence of the “twin deficits” in developing economies. Using unanticipated government spending shocks for an unbalanced panel of 114 developing economies from 1990 to 2015, we find that a one percent of GDP unanticipated improvement in the government budget balance improves, on average, the current account balance by 0.8 percentage point of GDP.

Posted by at 10:16 AM

Labels: Macro Demystified

Sunday, July 29, 2018

Difficulties of Making Predictions: Global Power Politics Edition

A new post by Timothy Taylor says that “Making predictions is hard, especially about the future. It’s a comment that seems to have been attributed to everyone from Nostradamus to Niels Bohr to Yogi Berra. But it’s deeply true. Most of us have a tendency to make statements about the future with a high level of self-belief, avoid later reconsidering how wrong we were, and then make more statements. […] The questions of how to predict for what you don’t expect, and how to plan for what you don’t expect, are admittedly difficult. The ability to pivot smoothly to face the new challenge may be one of the most underrated skills in politics and management. ”

Continue reading here.

A new post by Timothy Taylor says that “Making predictions is hard, especially about the future. It’s a comment that seems to have been attributed to everyone from Nostradamus to Niels Bohr to Yogi Berra. But it’s deeply true. Most of us have a tendency to make statements about the future with a high level of self-belief, avoid later reconsidering how wrong we were, and then make more statements. […] The questions of how to predict for what you don’t expect,

Posted by at 3:45 PM

Labels: Forecasting Forum

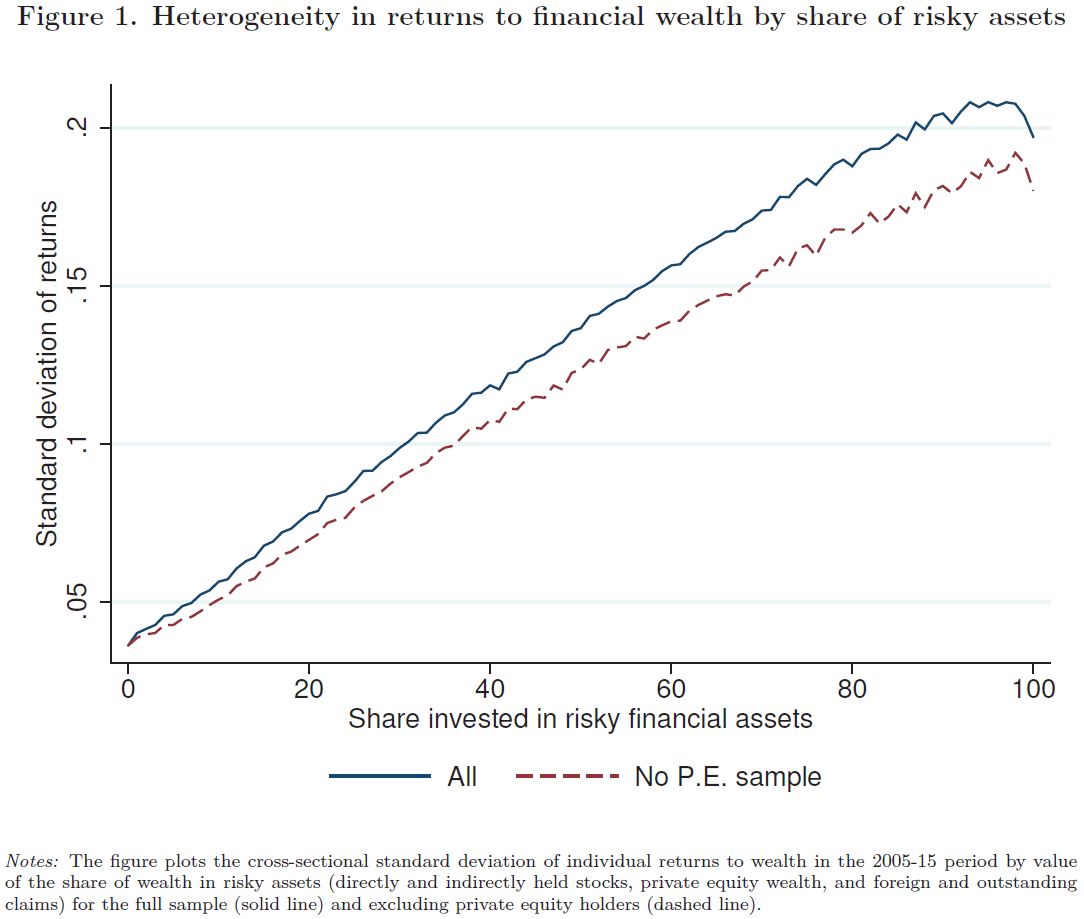

Heterogeneity and Persistence in Returns to Wealth

From a new IMF working paper:

“We provide a systematic analysis of the properties of individual returns to wealth using twelve years of

population data from Norway’s administrative tax records. We document a number of novel results.

First, during our sample period individuals earn markedly different average returns on their financial

assets (a standard deviation of 14%) and on their net worth (a standard deviation of 8%). Second,

heterogeneity in returns does not arise merely from differences in the allocation of wealth between safe

and risky assets: returns are heterogeneous even within asset classes. Third, returns are positively

correlated with wealth: moving from the 10th to the 90th percentile of the financial wealth distribution

increases the return by 3 percentage points – and by 17 percentage points when the same exercise is

performed for the return to net worth. Fourth, wealth returns exhibit substantial persistence over time.

We argue that while this persistence partly reflects stable differences in risk exposure and assets scale,

it also reflects persistent heterogeneity in sophistication and financial information, as well as

entrepreneurial talent. Finally, wealth returns are (mildly) correlated across generations. We discuss the

implications of these findings for several strands of the wealth inequality debate.”

From a new IMF working paper:

“We provide a systematic analysis of the properties of individual returns to wealth using twelve years of

population data from Norway’s administrative tax records. We document a number of novel results.

First, during our sample period individuals earn markedly different average returns on their financial

assets (a standard deviation of 14%) and on their net worth (a standard deviation of 8%).

Posted by at 3:41 PM

Labels: Inclusive Growth

Friday, July 27, 2018

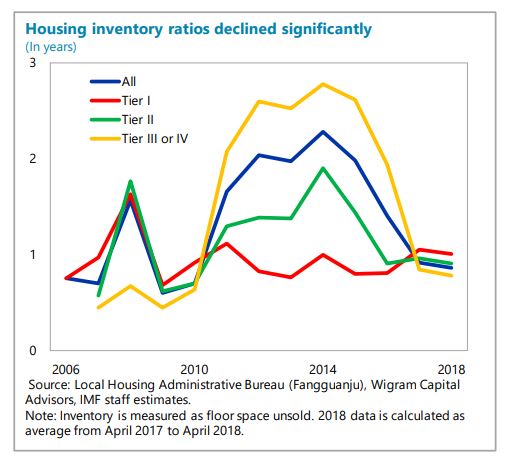

Housing Market in China

The IMF’s latest report on China says that:

- “Housing inventories in smaller cities declined considerably, due in part to social housing programs. House price growth moderated following the tightening measures since late 2016.”

- “A more sustainable housing market. The government’s “long-term mechanism for housing” appropriately focuses on addressing fundamental supply-demand imbalances. Ensuring long-run sustainability of the housing market requires increasing land supply for residential housing, promoting rental markets, and reducing the reliance of local governments on land sales. De-emphasizing growth targets would allow housing investment to be driven by long-run fundamentals, rather than the need to manage economic cycles. Staff’s projection indicates that residential investment, a key growth engine over the last decade, will decline as a share of GDP over the medium term as household income and consumption growth moderates.”

The IMF’s latest report on China says that:

- “Housing inventories in smaller cities declined considerably, due in part to social housing programs. House price growth moderated following the tightening measures since late 2016.”

- “A more sustainable housing market. The government’s “long-term mechanism for housing” appropriately focuses on addressing fundamental supply-demand imbalances. Ensuring long-run sustainability of the housing market requires increasing land supply for residential housing,

Posted by at 3:50 PM

Labels: Global Housing Watch

Housing View – July 27, 2018

On the US:

- Gen X rebounds as the only generation to recover the wealth lost after the housing crash – Pew Research Center

- ‘Severe’ housing shortage hits US home sales, lifts prices – Financial Times

- Airbnb pulled out every trick to stop NYC from curbing rentals – CNET

- The Millionaire’s Mortgage – Slate

- How Washington could actually make housing more affordable – CNN

- When Black Lawmakers Get Elected, Zoning Decisions Change – CityLab

On other countries:

- [China] Stabilizing China’s Housing Market – VoxChina

- [United Kingdom] Millennials must fight for their right to housing – Financial Times

- [United Kingdom] London house prices are falling, and remain as unaffordable as ever – Quartz

Photo by Aliis Sinisalu

On the US:

- Gen X rebounds as the only generation to recover the wealth lost after the housing crash – Pew Research Center

- ‘Severe’ housing shortage hits US home sales, lifts prices – Financial Times

- Airbnb pulled out every trick to stop NYC from curbing rentals – CNET

- The Millionaire’s Mortgage – Slate

- How Washington could actually make housing more affordable – CNN

- When Black Lawmakers Get Elected,

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts