Tuesday, October 16, 2018

Housing and Macroeconomics

Global Housing Watch Newsletter: October 2018

*Below is a summary of a workshop prepared by Benjamin Larin (Leipzig University), Hans Torben Löfflad (Leipzig University), Konstantin Gantert (Leipzig University).

What drives house price fluctuations? How do fluctuations in house prices and credit affect the real economy? What explains the long-run dynamics of house prices? How do house prices and rents affect wealth inequality and individual welfare? These are some of the questions that were discussed at a recent event.

The European Association of Young Economists (EAYE), in collaboration with Leipzig University, organized the first EAYE Workshop on Housing and Macroeconomics. This newly established workshop will take place annually and will focus on a specific topic. The workshop is organized by young economists, and it is meant for young economists. This year’s keynote lectures were Moritz Kuhn (University of Bonn, CEPR, IZA) and Alberto Martín (ECB, CREI, Barcelona GSE). What follows is a summary of this year’s workshop.

Credit cycles, housing, and short-term fluctuations

How credit and the real side of the economy are linked, and how financial shocks translate to changes in GDP—this is one of the questions that was asked frequently at the workshop. One paper analyzed the effects of credit expansion on aggregate demand in Denmark. The authors find that additional demand due to credit expansion is mostly spend in the non-tradable sector. Employment increases, mostly at small firms, yet the average labor separation rate is found to be higher for those jobs. Another paper analyzed the supply side effects of housing on the macroeconomy. The authors found that housing supply elasticities have decreased over the course of the last two US housing boom-bust episodes, implying more volatile house prices.

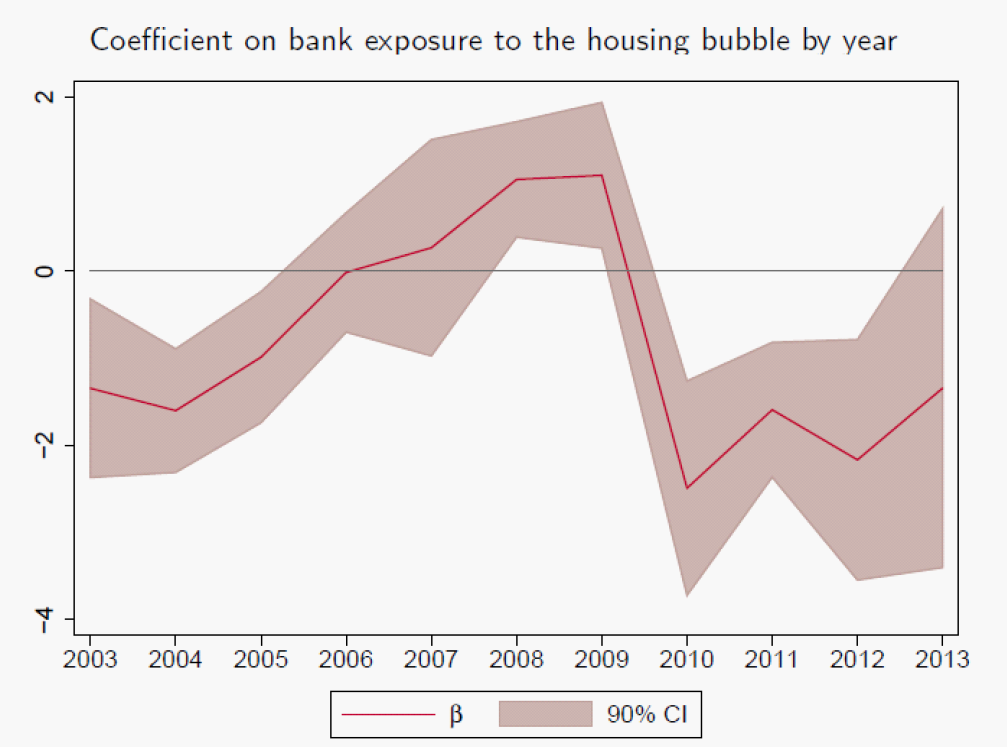

In the first keynote lecture, Alberto Martin presented a theory of macroeconomics of rational bubbles with an application to housing bubbles. He showed that a housing bubble leads to investment into the housing sector, first crowding out investment in non-housing firms (see figure 1). As bank capital increases over time, credit to non-housing firms increases as well. As the housing bubble bursts, this development reverses as credit lines freeze.

Figure 1.

Note: Coefficient of housing credit exposure of banks on credit growth to non-financial firms in the U.S. from 2003 to 2013. A value below 0 indicates a fall in credit to non-housing firms as the exposure to housing credit of a bank increases.

The real effects of housing credit on the macroeconomy are driven by changes in the credit side of the economy. A paper presented preliminary evidence that there is again a housing bubble in the U.S. and in other OECD economies. The housing bubbles in the U.S. seem to be geographically clustered, yet county specific factors cannot explain this. Bubbles do in general induce investment and growth through collateral feedback loops, yet they also create significant costs when they burst. When a bubble bursts feedback loops amplify the effects on the real economy. One channel is the excessively volatile risk premium that has to be paid. Another channel is the fluctuation in housing liquidity due to a change in the average time-to-sell margin. When everybody wants to sell their house, there is a supply side overhang and the liquidity of houses decreases strongly. This leads to a decrease in the value of houses.

Policy applications

As volatility of risk and house prices is high and its economic costs are large, the question arises whether policy can smooth this cycle and increase welfare. Two papers discussed different policy measures.

First, is macroprudential policy useful as an aggregate policy tool or should it take regional heterogeneity into account? A model-based analysis shows that taking the regional heterogeneity of house prices into account has potential benefits over classical monetary policy targeting inflation and one-size-fits-it-all macroprudential policy.

The second paper asked whether monetary policy effectiveness changes depending on the leverage cycle. The authors show that monetary policy is very effective when households deleverage, and credit constraints are binding, while it has only small effects when household leverage is increasing.

A third paper took a completely different angle on housing and studied the effect of the recent refugee inflow on rents in Germany. The authors find, very surprisingly, that local rents decrease as refugees move in. A possible explanation is the crowding out of the original population to different places in response to the inflow of refugees in their neighborhood.

Growth and wealth distribution

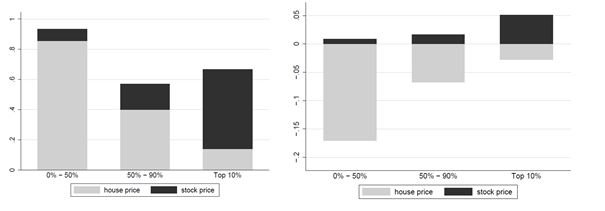

Some presentations at the workshop studied the relevance of the portfolio composition and house prices on the dynamics of wealth inequality. As the bottom 90 percent of the U.S. wealth distribution have a very large housing portfolio share, and hold only a small fraction of equity, it is paramount to wealth distribution how the two assets develop relatively to each other. Moritz Kuhn emphasized that the evolution of wealth inequality is the result of a race between housing and equity performance (see figure 2). When housing does relatively better, wealth inequality decreases. When equity does relatively better, wealth inequality increases.

Figure 2.

Note: The left figure indicates the wealth growth of different groups of the wealth distribution in the U.S. separated for housing and equity between 1998 and 2007. The right figure shows the impact on wealth growth from 2008 to 2016.

The significance of this statement has further been shown by a presentation on wealth inequality in Spain. There, wealth inequality did not increased significantly as rich households held a relatively high share of housing in their portfolio. Moritz Kuhn further emphasized the importance of data on the joint distribution of income and wealth for better understanding the dynamics of income and wealth inequality.

Takeaways from the workshop

Housing and Macroeconomics is an increasingly important topic. And as the many high-quality presentations have showed, young economists are aware of the importance of this topic. Housing has both short and long-run effects on the macroeconomy and the two dimensions might be connected. The financialization of housing drives both the business cycle and long-run wealth inequality. Therefore, housing is an important determinant for welfare and the economy in general.

Note: Photo on the left: Alberto Martin, center photo: participants at the workshop, right photo: Moritz Kuhn.

Global Housing Watch Newsletter: October 2018

*Below is a summary of a workshop prepared by Benjamin Larin (Leipzig University), Hans Torben Löfflad (Leipzig University), Konstantin Gantert (Leipzig University).

What drives house price fluctuations? How do fluctuations in house prices and credit affect the real economy?

Posted by at 5:00 AM

Labels: Global Housing Watch

Monday, October 15, 2018

Are published oil price forecasts efficient?

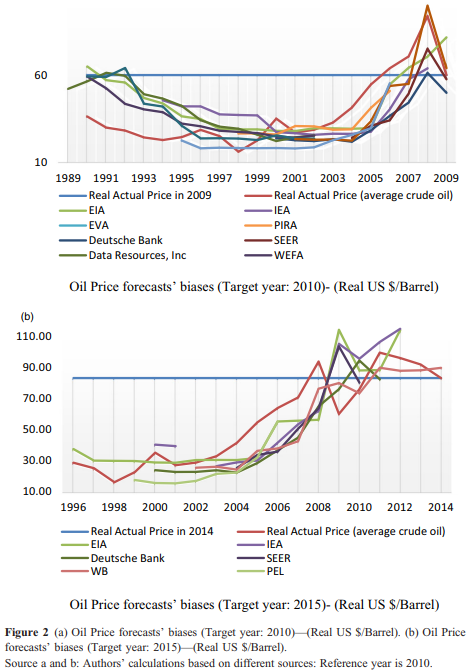

A new paper assesses “the accuracy and efficiency of crude oil price forecasts published by different organisations, think tanks and companies. Since the sequence of published forecasts appears as smooth, the weak efficiency criterion is clearly violated. Even combining forecasts, cannot increase efficiency due to high correlation among various forecasts. This pattern of oil price forecasts can be attributed to combining myopia (use current oil price levels as a basis) with Hotelling-type exponential growth. Another behavioural explanation in source of inefficiencies is that forecasters prefer to harmonise their forecasts with other forecasters in order to be not an outlier.”

A new paper assesses “the accuracy and efficiency of crude oil price forecasts published by different organisations, think tanks and companies. Since the sequence of published forecasts appears as smooth, the weak efficiency criterion is clearly violated. Even combining forecasts, cannot increase efficiency due to high correlation among various forecasts. This pattern of oil price forecasts can be attributed to combining myopia (use current oil price levels as a basis) with Hotelling-type exponential growth.

Posted by at 10:19 AM

Labels: Forecasting Forum

Friday, October 12, 2018

Housing View – October 12, 2018

On cross-country:

- Book: Housing Bubbles – SpringerLink

On the US:

- Mortgage Lending and Housing Markets – NBER

- Dark clouds gather over the US housing market – Financial Times

- 10 years later: How the housing market has changed since the crash – Washington Post

- The Housing Bust Widened the Wealth Gap. Here’s How. – Zillow

- Homeless in US: A deepening crisis on the streets of America – BBC

- Low mortgage rates and securitization: A distinct perspective on the U.S. housing boom – Brunel University of London

- Housing Sentiment Dips Slightly on Interest Rate Concerns – Fannie Mae

- 2018 Cost Burden Report: Despite improvements, affordability issues are immense – Apartment List

On other countries:

- [China] Angry Mobs Show All’s Not Well in China’s Property Sector – Bloomberg

- [Hong Kong] An Early Warning Sign for the World’s Priciest Homes Is Flashing Sell – Bloomberg

- [United Kingdom] What determines UK housing equity withdrawal in later life? – Regional Science and Urban Economics

Photo by Aliis Sinisalu

On cross-country:

- Book: Housing Bubbles – SpringerLink

On the US:

- Mortgage Lending and Housing Markets – NBER

- Dark clouds gather over the US housing market – Financial Times

- 10 years later: How the housing market has changed since the crash – Washington Post

- The Housing Bust Widened the Wealth Gap.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, October 11, 2018

Inequality in and across Cities

From a new article by Jessie Romero and Felipe F. Schwartzman at the Richmond Fed:

“Inequality in the United States has an important spatial component. More-skilled workers tend to live in larger cities where they earn higher wages. Less-skilled workers make lower wages and do not experience similar gains even when they live in those cities. This dynamic implies that larger cities are also more unequal. These relationships appear to have become more pronounced as inequality has increased. The evidence points to externalities among high-skilled workers as a significant contributor to those patterns.”

“A large body of research has identified several key facts about inequality across and within cities. First, larger cities have a greater concentration of high-skilled workers. In the Fifth District, for example, the share of the population over age twenty-five with a bachelor’s degree is 45 percent in the most urban areas, compared with 16 percent in the most rural areas. In the United States as a whole, the proportion ranges from 35 percent in the most urban areas to 17 percent in the most rural areas.”

“Second, nominal wages are higher in larger cities and in cities with a larger proportion of high-skilled workers. In the most urban areas of the Fifth District, average annual pay in 2016 was nearly $64,000; in the most rural areas, it was less than $35,000. Nationwide, workers in the most urban areas earned about $60,000 on average in 2016, while workers in the most rural areas earned about $36,000. (See Figure 2 above.) In recent research, Nathaniel Baum-Snow, Matthew Freedman, and Ronni Pavan find that nominal wages increase 0.065 percent for every percentage point increase in city size (based on data from 2005–07). They also find that the relationship between city size and wages has strengthened over time and that the wage gap between urban and rural areas has increased”

From a new article by Jessie Romero and Felipe F. Schwartzman at the Richmond Fed:

“Inequality in the United States has an important spatial component. More-skilled workers tend to live in larger cities where they earn higher wages. Less-skilled workers make lower wages and do not experience similar gains even when they live in those cities. This dynamic implies that larger cities are also more unequal. These relationships appear to have become more pronounced as inequality has increased.

Posted by at 5:59 PM

Labels: Inclusive Growth

Wednesday, October 10, 2018

Why Has the Stock Market Risen So Much Since the US Presidential Election?

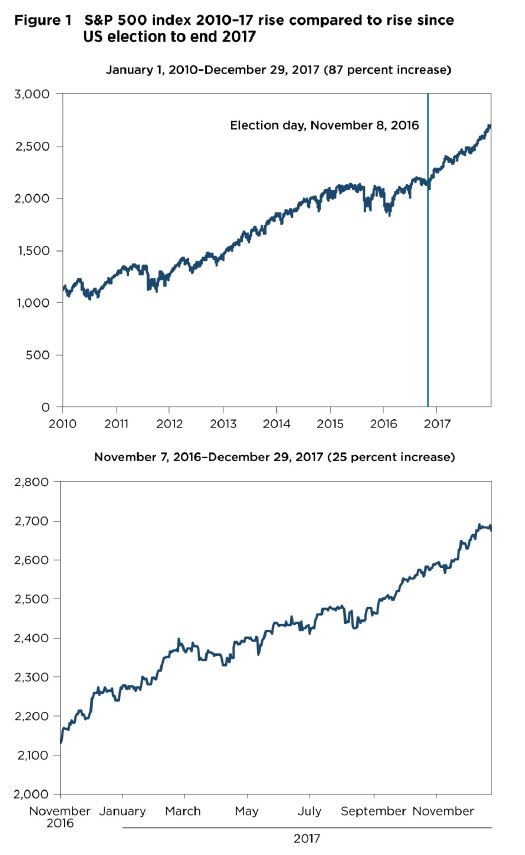

From a new paper by Olivier Blanchard, Christopher G. Collins, Mohammad R. Jahan-Parvar, Thomas Pellet, and Beth Anne Wilson:

“This paper looks at the evolution of U.S. stock prices from the time of the Presidential elections to the end of 2017. It concludes that a bit more than half of the increase in the aggregate U.S. stock prices from the presidential election to the end of 2017 can be attributed to higher actual and expected dividends. A general improvement in economic activity and a decrease in economic policy uncertainty around the world were the main factors behind the stock market increase. The prospect and the eventual passage of the corporate tax bill nevertheless played a role. And while part of the rise in stock returns came from a decrease in the equity risk premium, this decrease was relatively limited and returned the premium to the levels of the first half of the 2000s.”

From a new paper by Olivier Blanchard, Christopher G. Collins, Mohammad R. Jahan-Parvar, Thomas Pellet, and Beth Anne Wilson:

“This paper looks at the evolution of U.S. stock prices from the time of the Presidential elections to the end of 2017. It concludes that a bit more than half of the increase in the aggregate U.S. stock prices from the presidential election to the end of 2017 can be attributed to higher actual and expected dividends.

Posted by at 4:11 PM

Labels: Macro Demystified

Subscribe to: Posts