Sunday, November 25, 2018

Grim Stock Signals Piling Up as Wall Street Mulls Recession Odds

A new Bloomberg post cites my study:

“Nine turbulent weeks and a correction in U.S. stocks have left analysts with a thorny question. What’s the market saying about the economy? And while few see incontrovertible signs investors are bracing for a recession, it’s a word that’s been coming up more as they seek a signal in the chaos.

From the ascent of defensive industries to the sudden craze for companies that resist volatility, stocks are acting in ways that have presaged slowing growth in the past. That makes sense: gains in the economy and corporate earnings are forecast to ease in 2019 from this year’s torrid pace.

Befitting that, most of the charts that follow reflect observations by analysts who don’t see a recession as the most obvious conclusion. Many view the sell-off as healthy after a 10-year run of gains. But with a trade war flaring and the Federal Reserve set to boost interest rates again, the number of stock researchers who are at least willing to mention the possibility is rising.”

“Economists haven’t always done a great job predicting contractions. A 2014 study by the International Monetary Fund’s Prakash Loungani found that not one of 49 recessions suffered around the world in 2009 had been predicted by the consensus of economists a year earlier. Loungani previously reported that only two of the 60 recessions of the 1990s had been anticipated a year in advance.”

“[…] the economic indicators that often precede recession — yield curve inversion and rising unemployment — are not flashing warning signs. The yield curve is flat but not inverted and the unemployment rate keeps falling, as opposed to rising when a recession approaches.”

A new Bloomberg post cites my study:

“Nine turbulent weeks and a correction in U.S. stocks have left analysts with a thorny question. What’s the market saying about the economy? And while few see incontrovertible signs investors are bracing for a recession, it’s a word that’s been coming up more as they seek a signal in the chaos.

From the ascent of defensive industries to the sudden craze for companies that resist volatility,

Posted by at 1:19 PM

Labels: Forecasting Forum

A New Canadian Macroeconomic Database

From a new post by Dave Giles:

“Anyone who’s undertaken empirical macroeconomic research relating to Canada will know that there are some serious data challenges that have to be surmounted.

In particular, getting access to long-term, continuous, time series isn’t as easy as you might expect.

Statistics Canada has been criticized frequently over the years by researchers who find that crucial economic series are suddenly “discontinued”, or are re-defined in ways that make it extremely difficult to splice the pieces together into one meaningful time-series.

In recognition of these issues, a number of efforts have been made to provide Canadian economic data in forms that researchers need. These include, for instance, Boivin et al. (2010), Bedock and Stevanovic (2107), and Stephen Gordon’s on-going “Project Link“.

Thanks to Olivier Fortin-Gagnon, Maxime Leroux, Dalibor Stevanovic, &and Stéphane Suprenant we now have an impressive addition to the available long-term Canadian time-series data. Their 2018 working paper, “A Large Canadian Database for Macroeconomic Analysis“, discusses their new database and illustrates its usefulness in a variety of ways.”

From a new post by Dave Giles:

“Anyone who’s undertaken empirical macroeconomic research relating to Canada will know that there are some serious data challenges that have to be surmounted.

In particular, getting access to long-term, continuous, time series isn’t as easy as you might expect.

Statistics Canada has been criticized frequently over the years by researchers who find that crucial economic series are suddenly “discontinued”,

Posted by at 1:08 PM

Labels: Macro Demystified

How does monetary policy affect income and wealth inequality?

From a new paper by Yannis Dafermos and Christos Papatheodorou:

“The recent empirical literature on the distributional effects of monetary policy on inequality has focused on the various channels through which a change in the policy interest rate or the central bank asset purchases affect income and wealth inequality. Although most studies show that expansionary (contractionary) conventional policy tends to reduce (increase) income inequality (see Coibion et al., 2017; Mumtaz and Theophilopoulou, 2017; Furceri et al., 2018; Guerello, 2018; Ampudia et al., 2018), there is no consensus on whether these effects are economically significant. In addition, there is no consensus about (i) the size and the direction of the effects of conventional monetary policy on wealth inequality and (ii) the distributional impact of quantitative easing (see e.g. Saiki and Frost, 2014; Domaski et al., 2016; Montecino and Epstein, 2017; Mumtaz and Thephilopoulou, 2017; O’Farrell and Rawdanowicz, 2016; Ampudia et al., 2018; Casiraghi et al., 2018; Guerello, 2018; Koedijk, 2018). This comes as no surprise: the magnitude of the distribution channels of monetary policy depends on a number of factors which influence the impact of these channels across countries and time periods. For example, it has been shown that the effect of monetary policy on inequality depends on the initial wealth distribution and the composition of household financial assets (O’Farrell and Rawdanowicz, 2017; Guerello, 2018), the initial wage share (Furceri et al., 2018) and the marginal propensity to consume (Ampudia et al., 2018).

Despite these recent developments in the empirical literature, there is currently no theoretical model that incorporates the key distribution channels of monetary policy simultaneously and is capable of analysing in a systematic way the exact conditions under which monetary policy has economically significant effects on inequality. This paper develops such a model by combining the agent-based (AB) and the stock-flow consistent (SFC) approaches to macroeconomic modelling. The SFC approach is characterised by the explicit incorporation of accounting principles into dynamic macro modelling and the emphasis that it places on the dynamic interplay between monetary stocks and flows (see Godley and Lavoie, 2007a). The AB approach is suitable for exploring how macroeconomic phenomena emerge out of the interactions between heterogeneous agents. It has been recently argued that the combination of agent-based and stockflow consistent approaches is a fruitful avenue for the reconstruction of macroeconomics, moving beyond the conventional representative agents framework (see e.g. van der Hoog and Dawid, 2015; Caiani et al., 2016).”

From a new paper by Yannis Dafermos and Christos Papatheodorou:

“The recent empirical literature on the distributional effects of monetary policy on inequality has focused on the various channels through which a change in the policy interest rate or the central bank asset purchases affect income and wealth inequality. Although most studies show that expansionary (contractionary) conventional policy tends to reduce (increase) income inequality (see Coibion et al., 2017; Mumtaz and Theophilopoulou,

Posted by at 1:04 PM

Labels: Inclusive Growth

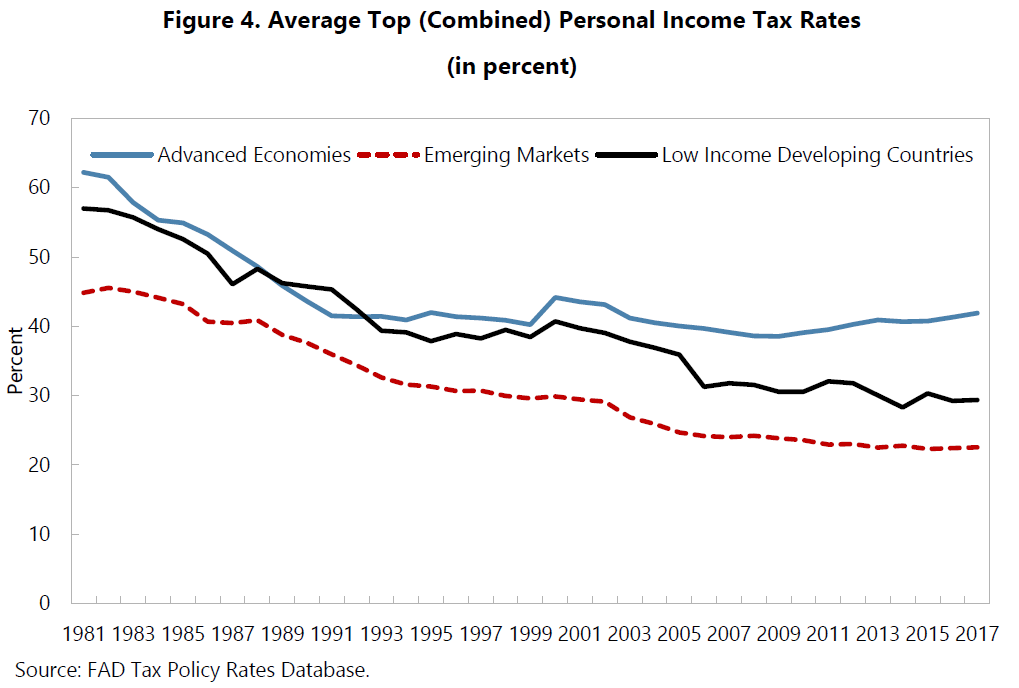

Personal Income Tax Progressivity: Trends and Implications

From a new IMF working paper:

“This paper has approached progressivity from different angles. Bringing together our findings, we can conclude strongly that progressivity has decreased over the last few decades, a finding that is robust to the choice of measure. We also conclude, but with less certainty, that the reduction in progressivity appears not to have given growth a boost.

While this paper focused on personal income taxes, developments in capital income taxation are also likely to have contributed to reducing overall progressivity: Capital income is distributed more unequally than labor income, has risen over the past few decades as a share of total income (IMF, 2017b), and is often taxed at a lower rate than labor income. The corporate income tax, in particular, plays an important role in determining progressivity. First, there can be a direct effect to the extent that it is partly borne by owners of corporations. Second, it indirectly supports the enforcement of the taxation of labor income: Corporate taxation mitigates arbitrage in response to taxation of entrepreneurial income, because distinguishing labor income from capital income can be difficult (or impossible) when individuals can freely choose the form through which they declare their income (IMF, 2014). When the personal income tax base can be shifted to some alternative tax base that is taxed at a lower rate (such as corporate income), optimal tax theory implies that the optimal tax rate on personal income rises with the tax rate on the alternative base. In recent decades, international tax competition—resulting from capital mobility—has led to a steady downward trend in corporate income tax rates (Table 2). This trend reduces overall tax progressivity and may also put downward pressure on personal income tax rates—even though labor itself is less mobile and could be taxed more easily in a globalized world.

There are many unresolved questions and areas for further research. For example, progressivity measures taking the entire tax and benefit system, and ideally even public spending, into account would enhance the understanding of overall progressivity tremendously. The challenges in finding such a measure, especially one that is still independent of pre-tax and spending distributions are enormous.

Despite the absence of a fully comprehensive measure of progressivity, and some reasonable doubts about the impact of progressivity on growth, it appears safe to say that progressivity-enhancing measures could be taken without major risks to growth. This would be especially relevant in countries that are marked by great inequality.”

From a new IMF working paper:

“This paper has approached progressivity from different angles. Bringing together our findings, we can conclude strongly that progressivity has decreased over the last few decades, a finding that is robust to the choice of measure. We also conclude, but with less certainty, that the reduction in progressivity appears not to have given growth a boost.

While this paper focused on personal income taxes,

Posted by at 12:57 PM

Labels: Inclusive Growth

Saturday, November 24, 2018

Is Inflation Domestic or Global? Evidence from Emerging Markets

From a new IMF working paper:

“Following a period of disinflation during the 1990s and early 2000s, inflation in emerging markets has remained remarkably low. The volatility and persistence of inflation also fell considerably and remained low despite large swings in commodity prices, the global financial crisis, and periods of strong and sustained US dollar appreciation. A key question is whether this improved inflation performance is sustainable or rather reflects global disinflationary forces that could prove temporary. In this paper, we use a New-Keynesian Phillips curve framework and data for 19 large emerging market economies over 2004-18 to assess the contribution of domestic and global factors to domestic inflation dynamics. Our results suggest that longer-term inflation expectations, linked to domestic factors, were the main determinant of inflation. External factors played a considerably smaller role. The results underscore that although emerging markets are increasingly integrated into the global economy, policymakers remain largely in control of domestic inflation developments.”

From a new IMF working paper:

“Following a period of disinflation during the 1990s and early 2000s, inflation in emerging markets has remained remarkably low. The volatility and persistence of inflation also fell considerably and remained low despite large swings in commodity prices, the global financial crisis, and periods of strong and sustained US dollar appreciation. A key question is whether this improved inflation performance is sustainable or rather reflects global disinflationary forces that could prove temporary.

Posted by at 7:44 PM

Labels: Inclusive Growth

Subscribe to: Posts