Tuesday, December 25, 2018

Paper Tigers

From a new post by Adam M. Grossman:

“Economist Prakash Loungani has spent the better part of two decades researching the issue. In a 2001 study, Loungani evaluated experts’ ability to forecast recessions. His conclusion was blunt: “The record of failure to predict recessions is virtually unblemished.” In a follow-up study, looking at the 2008 financial crisis, Loungani’s findings were nearly identical. Economists uniformly failed to predict that global recession.

Perhaps Loungani’s study wasn’t comprehensive enough. What about all-star forecasters? Here the evidence is inevitably more anecdotal, but no more encouraging. Consider Abby Joseph Cohen, the recently-retired Goldman Sachs strategist. Her forecasts during the 1990s earned her the nickname “the Prophet of Wall Street.” But she later missed the two biggest meltdowns of her career: In 2000, when the dot-com bubble burst, Cohen predicted the market would rise. And she, along with virtually everybody else, missed the 2008 collapse.

A more recent example: Ray Dalio, the billionaire founder of hedge fund Bridgewater Associates, proclaimed in January of this year: “If you’re holding cash, you’re going to feel pretty stupid.” The year’s not over yet. But so far, cash has done materially better than the stock market, which is in negative territory.

The reality is that forecasting has always been difficult—and not just in the world of economics. Decca Records told the Beatles they have “no future in show business.” Walt Disney was once fired for “lacking imagination.” The list of incorrect predictions is long.

If forecasts are so error-prone, why do sensible organizations like Vanguard continue issuing them? In part, I believe it’s in response to investor demand: People want to know what’s going to happen and they believe experts can tell them. It’s just human nature. But now that you’ve seen the data, here’s my recommendation: Tune out anyone who approaches you with a crystal ball. Instead, situate yourself so the market’s short-term ups and downs don’t impact your ability to meet your financial goals—or to sleep at night.”

From a new post by Adam M. Grossman:

“Economist Prakash Loungani has spent the better part of two decades researching the issue. In a 2001 study, Loungani evaluated experts’ ability to forecast recessions. His conclusion was blunt: “The record of failure to predict recessions is virtually unblemished.” In a follow-up study, looking at the 2008 financial crisis, Loungani’s findings were nearly identical. Economists uniformly failed to predict that global recession.

Posted by at 8:27 PM

Labels: Forecasting Forum

Services sector export in Europe

From a new paper on the service exports in Europe:

“In this paper, we consider the changes that occurred in the service exports of thirty-eight European countries in the period of 2005–2016. We have found that the existing world trend related to the growth of service exports is also present in Europe. However, the trend of the service exports’ share growth in the general volume of export is not common for all European countries. We found that higher growth rates are observed in European countries with lower levels of GDP per capita. We also discovered the presence of a strong positive correlation between growth in service exports and GDP growth, as well as between growth in service exports and GDP per capita. We also found that there is a linear correlation between the growth of service exports and the growth of GDP per capita, as well as between the growth in service exports and GDP growth. The data obtained allowed us to conclude that European countries, categorized as “Innovation Leaders” in accordance with the European Innovation Scoreboard, are not the leading countries in Europe with regard to the rates of service export growth. We also discovered that service exports in Europe are less sensitive to adverse macroeconomic effects than goods exports.”

From a new paper on the service exports in Europe:

“In this paper, we consider the changes that occurred in the service exports of thirty-eight European countries in the period of 2005–2016. We have found that the existing world trend related to the growth of service exports is also present in Europe. However, the trend of the service exports’ share growth in the general volume of export is not common for all European countries.

Posted by at 8:20 PM

Labels: Inclusive Growth

Wired for Work: Exploring the Nexus of Technology & Jobs

From a new paper by Sabina Dewan

“As technological advancements proceed at an unprecedented scale and speed upending traditional employment models, researchers across the globe are working frenetically to understand how the world of work is changing and what the future holds. This paper explores the most important questions that scholars, policymakers and practitioners are grappling with in understanding the nexus of technology and jobs. It outlines what we know and where gaps remain. Understanding the potential reach of technological change along with emerging preferences and modes of organization can help us balance priorities across a broad range of actors. There is a need for urgent action to direct the impact that technology has on jobs. This means deliberate choices about work design on the part of employers, exploring new and innovative ways of organizing workers and creating a new set of government policies and regulations to manage the proliferation and effect of technology on jobs.”

From a new paper by Sabina Dewan

“As technological advancements proceed at an unprecedented scale and speed upending traditional employment models, researchers across the globe are working frenetically to understand how the world of work is changing and what the future holds. This paper explores the most important questions that scholars, policymakers and practitioners are grappling with in understanding the nexus of technology and jobs. It outlines what we know and where gaps remain.

Posted by at 8:15 PM

Labels: Inclusive Growth

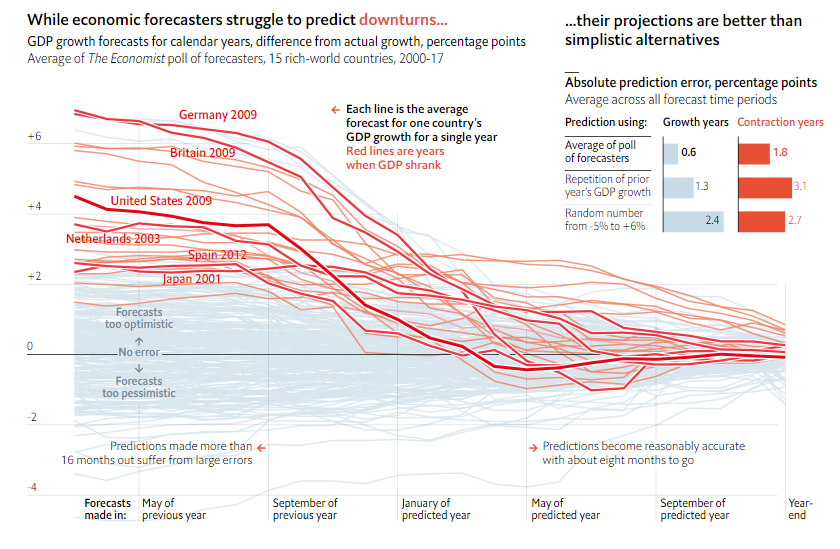

GDP predictions are reliable only in the short term

A new article from The Economist cites my paper:

“[…] economic forecasters project GDP growth of about 2% in 2020.”

“How much confidence should one have in these predictions? For the past 20 years The Economist has kept a database of projections by banks and consultancies for annual GDP growth. It now contains 100,000 forecasts across 15 rich countries. In general, they fared well over brief time periods, but got worse the further analysts peered into the future—a trend unsurprising in direction but humbling in magnitude. If a recession lurks beyond 2019, economists are unlikely to foresee it this far in advance.”

“The biggest errors occurred ahead of GDP contractions. The average projection 22 months before the end of a downturn year missed by 3.7 points, four times more than in other years. In part, this is because growth figures are “skewed”: economies usually expand slowly and steadily, but sometimes contract sharply. As a result, forecasters seeking to predict the most likely outcome expect growth. However, they adjust too slowly even once bad news arrives, says Prakash Loungani of the IMF. That suggests they are prone to “anchoring”—over-weighting previous expectations—or to “herding” (keeping their predictions near the consensus).”

“If forecasters displayed such biases consistently, an aggregator could beat the crowd by granting more weight to those with good records. But top performers rarely repeat their feats. When it comes to GDP, the best guide is the adage that prediction is difficult—especially about the future.”

A new article from The Economist cites my paper:

“[…] economic forecasters project GDP growth of about 2% in 2020.”

“How much confidence should one have in these predictions? For the past 20 years The Economist has kept a database of projections by banks and consultancies for annual GDP growth. It now contains 100,000 forecasts across 15 rich countries. In general, they fared well over brief time periods,

Posted by at 8:12 PM

Labels: Forecasting Forum

Friday, December 21, 2018

Housing View – December 21, 2018

On cross-country:

- How consumer behaviour sways the housing market- and the economy – ING

On the US:

- What’s Up With Construction Costs? – BuildZoom

- The Goldilocks problem of housing supply: Too little, too much, or just right? – Brookings

- Gentrification and Fair Housing: Does Gentrification Further Integration? – Furman Center for Real Estate and Urban Policy

- Where Have All The Renters Gone? – Harvard Joint Center for Housing Studies

- Risky Home Loans Are Making a Comeback. Are They Right for You? – New York Times

- California Needs a Housing Revolution – Bloomberg

- Here’s Housing’s Real Threat to the Economy – Bloomberg

On other countries:

- [Australia] Sydney’s house prices face a falling tide – Financial Times

- [Botswana] The housing market’s potential to boost Botswana’s economic growth – Bank of Botswana

- [Mexico] Mexico’s housing market is strengthening – Global Property Guide

- [Netherlands] Short-term rentals and the housing market: Quasi-experimental evidence from Airbnb in Los Angeles – VoxEU

- [Singapore] Can Singapore’s social housing keep up with changing times? – BBC

Photo by Aliis Sinisalu

On cross-country:

- How consumer behaviour sways the housing market- and the economy – ING

On the US:

- What’s Up With Construction Costs? – BuildZoom

- The Goldilocks problem of housing supply: Too little, too much, or just right? – Brookings

- Gentrification and Fair Housing: Does Gentrification Further Integration? – Furman Center for Real Estate and Urban Policy

- Where Have All The Renters Gone?

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts