Sunday, February 3, 2019

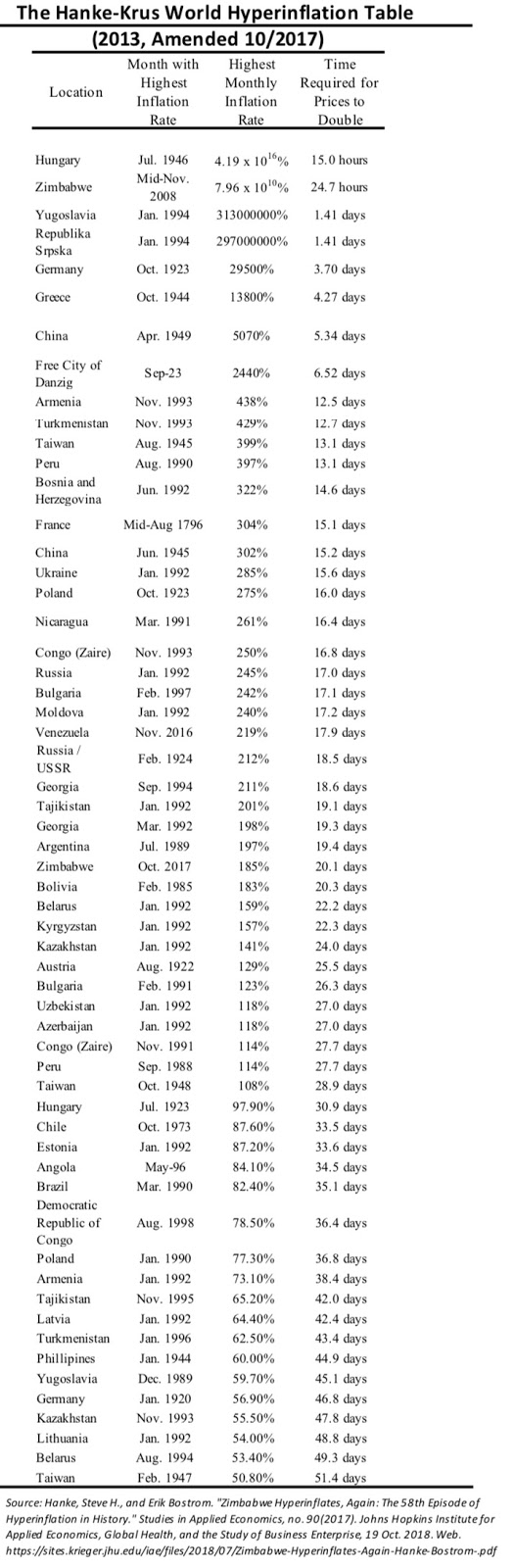

58 Episodes of Hyperinflation (Venezuela is #23)

From Conversable Economist:

“Steve Hanke has devoted considerable effort to building up data on hyperinflations during the last century or so. He offers a quick overview of this work in Forbes (January 20, 2019). Below is his list of hyperinflations. When it comes to Venezuela, he writes:

Now, let’s turn to the world’s only current hyperinflation: Venezuela. It ranks as the 23rd most severe. Today, the annual rate of inflation is 120,810%/yr. While this rate is modest by hyperinflation standards, the duration of Venezuela’s hyperinflation episode, as of today, is long: 27 months. Only four episodes of hyperinflation have been more long-lived.

Here’s the table of all 58 hyperinflations:”

From Conversable Economist:

“Steve Hanke has devoted considerable effort to building up data on hyperinflations during the last century or so. He offers a quick overview of this work in Forbes (January 20, 2019). Below is his list of hyperinflations. When it comes to Venezuela, he writes:

Now, let’s turn to the world’s only current hyperinflation: Venezuela. It ranks as the 23rd most severe.

Posted by at 8:16 AM

Labels: Macro Demystified

Building an adequate U.S. labor and social protection system for the 21st century

From a working paper by Sandra Polaski:

“This paper reviews the erosion of labor and social protections for U.S. workers and households over recent decades. It discusses the causes and the relative weight of different elements of the erosion in order to bring clarity to the discussion of needed reforms. It proposes a framework of policy objectives and principles to guide choices for reform among policy alternatives in the specific U.S. context. The paper also explores the relative merits of some alternative proposals to address these challenges. The prospects for political and legislative action to create a viable modern social and labor protection system are discussed. The paper concludes that updating and strengthening existing elements of the U.S. system provides a firm foundation for creating an adequate U.S. labor and social protection floor for the 21st century, if critical additional rights and programs are built on and integrated into this foundation.”

From a working paper by Sandra Polaski:

“This paper reviews the erosion of labor and social protections for U.S. workers and households over recent decades. It discusses the causes and the relative weight of different elements of the erosion in order to bring clarity to the discussion of needed reforms. It proposes a framework of policy objectives and principles to guide choices for reform among policy alternatives in the specific U.S.

Posted by at 8:13 AM

Labels: Inclusive Growth

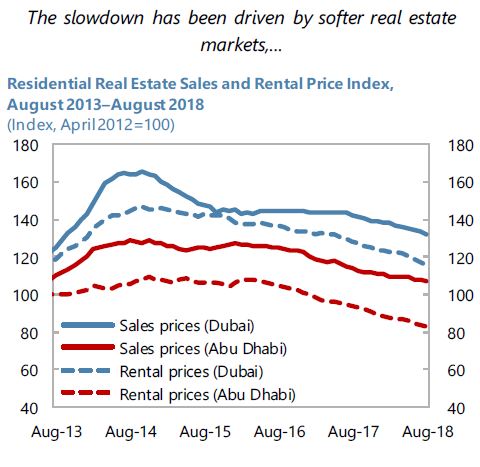

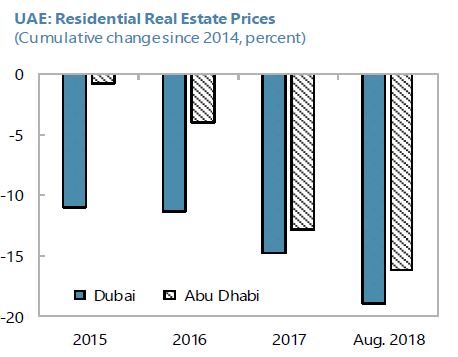

Housing Market in the United Arab Emirates

From the IMF’s latest report on UAE:

“A sharp deepening in the real estate downturn and weakening asset quality could constrain bank lending, which in turn could hold back the recovery.”

“Given the risk of spillovers from declining real estate prices, staff urged the CBU to resist calls for relaxing prudential limits on real estate lending. The authorities are preparing to develop a new bank resolution regime; in the meantime, staff encouraged the CBU to discuss contingency plans for banks in case of an abrupt tightening of financial conditions or other adverse shocks.”

From the IMF’s latest report on UAE:

“A sharp deepening in the real estate downturn and weakening asset quality could constrain bank lending, which in turn could hold back the recovery.”

“Given the risk of spillovers from declining real estate prices, staff urged the CBU to resist calls for relaxing prudential limits on real estate lending. The authorities are preparing to develop a new bank resolution regime; in the meantime,

Posted by at 8:09 AM

Labels: Global Housing Watch

Friday, February 1, 2019

Housing View – February 1, 2019

On cross-country:

- Global Home Price Growth under Pressure – Fitch Ratings

- House Prices to Fall in Several APAC Markets in 2019 – Fitch Ratings

On the US:

- The Dream Revisited – Columbia University Press

- Supply Skepticism: Housing Supply and Affordability – NYU Furman Center

- In Lieu of Gifts, Please Make a Down Payment on Our New Home – Citylab

- Could High-Speed Rail Ease California’s Housing Crisis? See Japan. – Citylab

- More Housing Would Mean Cheaper Housing – Wall Street Journal

- California housing crisis podcast: Where’s the home building for the middle class? – Los Angeles Times

- AEI Housing Market Indicators release on October 2018 data – American Enterprise Institute

- Mortgage Risk Premiums during the Housing Bubble – The Journal of Real Estate Finance and Economics

- Big drop in US homebuilders’ shares could spell trouble – Financial Times

- Americans stopped buying homes in 2018, mortgage lenders are getting crushed, and an economic storm could be brewing – Business Insider

- Two Lawsuits Show What a Hot Mess California Housing Politics Is Right Now – Reason

On other countries:

- [China] Chinese Exiting U.S. Real Estate as Beijing Directs Money Back to Shore Up Economy – Wall Street Journal

- [India] Too slow for the urban march: Litigations and real estate market in Mumbai, India – Brookings

- [Lebanon] Lebanese Central Bank to Reinstate Subsidized Housing Loans – Bloomberg

- [New Zealand] New Zealand Vowed 100,000 New Homes to Ease Crunch. So Far It Has Built 47. – New York Times

- [Singapore] Singapore Is Seeing an Unprecedented Mortgage Slowdown – Bloomberg

- [United Kingdom] What goes up must come down: modelling the mortgage cycle – Bank of England

- [United Kingdom] London property transactions drop to decade low – Financial Times

- [United Kingdom] Call for rethink on UK planning rules for housing – Financial Times

Photo by Aliis Sinisalu

On cross-country:

- Global Home Price Growth under Pressure – Fitch Ratings

- House Prices to Fall in Several APAC Markets in 2019 – Fitch Ratings

On the US:

- The Dream Revisited – Columbia University Press

- Supply Skepticism: Housing Supply and Affordability – NYU Furman Center

- In Lieu of Gifts, Please Make a Down Payment on Our New Home – Citylab

- Could High-Speed Rail Ease California’s Housing Crisis?

Posted by at 5:00 AM

Labels: Global Housing Watch

Tuesday, January 29, 2019

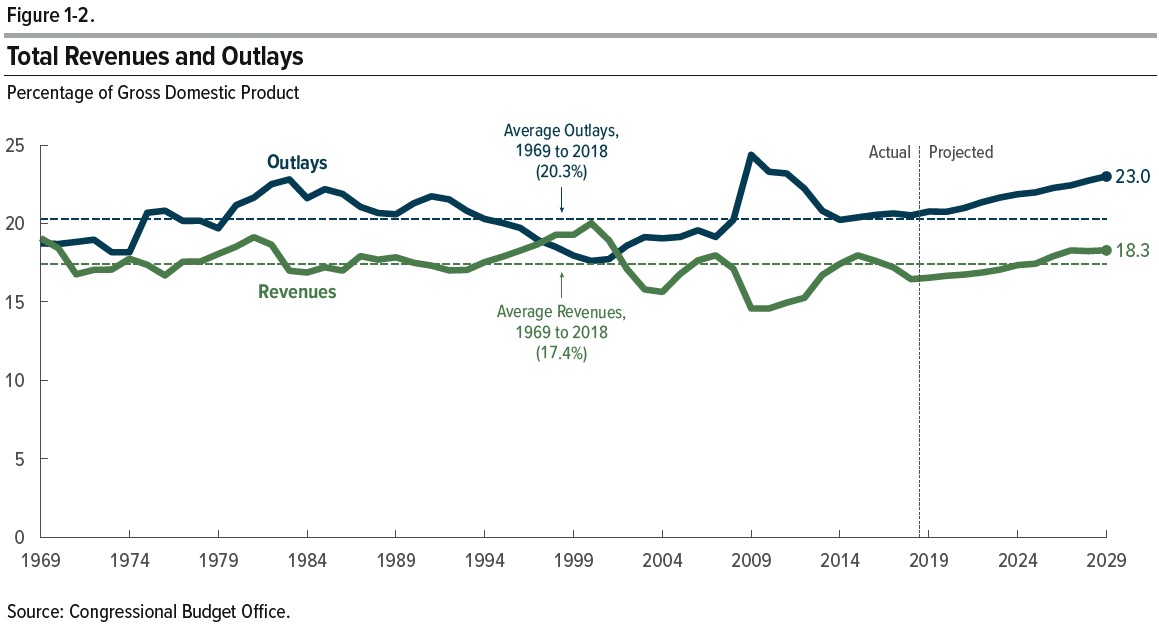

Budget Deficits and Debt: Background and Tradeoffs

From Conversable Economist:

“Twice a year the Congressional Budget Office publishes a “just the facts” overview of the federal budget picture and the US economy. The latest version is “The Budget andEconomic Outlook:2019 to 2029 (January 2019). Here, I’ll focus on the US budget deficit and debt.

Here’s the pattern of US federal government spending and revenues in the last 50 years. Average outlays during that time were 20.7% of GDP. Average revenues were 17.4% of GDP. Contrary to the widespread belief that US government spending and taxes have over time surged ever higher, to me the more obvious pattern here over the half-century is one of stability. Sure, government spending is higher and taxes are lower than the historical averages during the Great Recession. But during boom times like the late 1990s, taxes are above their historical average while spending is below. When President Trump took office early in 2017, US government spending and taxes were–whether for better or worse–almost bang on their long-run averages.

But under the surface, two changes are going on–one medium-term and one longer-term. The medium-term change is that the usual pattern over time has been that when the US economy is proceeding strongly, with sustained growth and a relatively low unemployment rate, the budget deficits are usually lower, or in the late 1990s even turned into surpluses. But at present, the trajectory is a relatively healthy economy but with larger-than-usual budget deficits.

This CBO figures shows that if one looks back at years when the unemployment rate was below 6%, the average budget deficit has been 1.5% of GDP. But although the current unemployment rate has been substantially below 6% for several years, the projected budget deficits for the next decade are projected at 4.4% of GDP.

Continue reading here.

From Conversable Economist:

“Twice a year the Congressional Budget Office publishes a “just the facts” overview of the federal budget picture and the US economy. The latest version is “The Budget andEconomic Outlook:2019 to 2029 (January 2019). Here, I’ll focus on the US budget deficit and debt.

Here’s the pattern of US federal government spending and revenues in the last 50 years. Average outlays during that time were 20.7% of GDP.

Posted by at 9:34 AM

Labels: Macro Demystified

Subscribe to: Posts