Friday, February 15, 2019

Housing View – February 15, 2019

On cross-country:

- Urban Futures – 2019 – Knight Frank

- Global affordable housing gap reaches $740 billion – Guardian

On the US:

- America Isn’t Building Enough New Housing – Bloomberg

- Housing Indicators to Watch in 2019 – Federal Reserve Bank of St. Louis

- Renting the American Dream: Why homeownership shouldn’t be a prerequisite for middle-class financial security – Brookings

- When Wall Street Is Your Landlord – The Atlantic

On other countries:

- [Ireland] Ireland’s rising house prices lead to tough choices – Financial Times

- [Malta] The Evolution of the Housing Stock in Malta – Central Bank of Malta

- [Netherlands] Knot Sounds Alarm Over the Impact of Dutch House-Price Swings – Bloomberg

- [United Kingdom] New stamp duty land tax surcharge for non-UK resident homebuyers to be introduced – UK

- [United Kingdom] A lack of affordable homes is forcing young Britons to live with their parents – World Economic Forum

On cross-country:

- Urban Futures – 2019 – Knight Frank

- Global affordable housing gap reaches $740 billion – Guardian

On the US:

- America Isn’t Building Enough New Housing – Bloomberg

- Housing Indicators to Watch in 2019 – Federal Reserve Bank of St. Louis

- Renting the American Dream: Why homeownership shouldn’t be a prerequisite for middle-class financial security – Brookings

- When Wall Street Is Your Landlord – The Atlantic

Posted by at 7:20 AM

Labels: Global Housing Watch

Wednesday, February 13, 2019

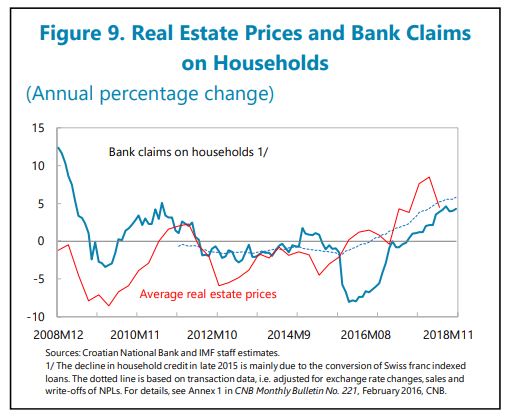

Housing Market in Croatia

From the IMF’s latest report on Croatia:

“The real estate market is also picking up, albeit from a low base and the recovery is rather segmented. Should both household borrowings and real estate prices further accelerate, additional macro prudential measures may need to be considered, including a comprehensive debt-service-to-income ratio capturing all debts, not just debts related to housing loans. Since May 2018, new loans are no longer reported to the credit register run by the Croatian Banking Association due to concerns of some banks about the implementation of the General Data Protection Regulation (GDPR). Staff recommended to shortly resolve these legal issues.”

“Macroprudential policies can contain possible pressure points. If real estate prices accelerate or high growth of cash loans persists, authorities could consider the introduction of additional measures to prevent excessive household borrowing (e.g., more comprehensive use of debt-service-to-income limits). Enhancements to the efficiency of bankruptcy procedures (e.g., by facilitating out-of-court settlements) would help further private sector deleveraging. Despite recent changes in the bankruptcy legislation, a comprehensive review to ensure that the insolvency framework aligns with best practices merits strong consideration.”

From the IMF’s latest report on Croatia:

“The real estate market is also picking up, albeit from a low base and the recovery is rather segmented. Should both household borrowings and real estate prices further accelerate, additional macro prudential measures may need to be considered, including a comprehensive debt-service-to-income ratio capturing all debts, not just debts related to housing loans. Since May 2018, new loans are no longer reported to the credit register run by the Croatian Banking Association due to concerns of some banks about the implementation of the General Data Protection Regulation (GDPR).

Posted by at 9:40 AM

Labels: Global Housing Watch

Tuesday, February 12, 2019

Housing Market in the Netherlands

From the latest IMF report on the Netherlands:

“The housing market is dominated by social housing (with a wait time exceeding a decade in some cases) and owner-occupied houses with significant shortages. The absence of a robust private rental market leaves young households, in particular, with little alternative to purchasing owner-occupied housing with high leverage and thin financial buffers. Rent controls, regulations, and inadequate means-testing result in long waiting lists for social housing. Elevated demand for owner-occupied houses was encouraged by generous mortgage interest deductibility (MID) in the past, which also boosted house prices. As macro-prudential policies were tightened recently, households’ debt has stabilized at about 250 percent of net disposable income, but it remains the second highest among OECD countries. Overborrowing on mortgages has contributed to the accumulation of household debt. When housing prices declined sharply after the global financial crisis (GFC), many mortgages were underwater and private consumption contracted sharply as households attempted to rebuild their net worth. Nevertheless, household overborrowing on mortgages is not a significant source of systemic risk in the financial sector even though it is a threat to the macro-economy

To reduce household debt and improve housing affordability, it is necessary to increase housing supply, tighten macro-prudential policies, and further reduce the debt bias in the tax system. Liberalizing rent controls for higher-income households and improving means-testing for social housing would help optimize allocation and improve housing supply. In addition, private investment should be encouraged by relaxing restrictions on zoning plans and simplifying administrative procedures for building permits. Lowering the maximum loan-to-value (LTV) ratio to no more than 90 percent (from 100 percent currently) and capping the debt service to income (DSTI) ratio to limit its procyclicality should be considered. The authorities plan to accelerate the phasing down of MID by 3 percentage points per year starting from 2020 until the basic rate of 37.05 percent is reached is a welcome step. Further phasing down of MID, to bring it at a neutral level compared with taxation of investment in other type of assets, would not only generate additional revenues but also help address the current debt bias of households.

The authorities emphasized that the focus is currently on increasing housing supply, while giving due consideration to possible tighter macro-prudential policies. To increase supply, the authorities are taking actions to improve coordination among the main stakeholders, including the relevant ministries, subnational governments, and private investors to reduce building preparation time, stimulate the transformation of suitable areas like outdated industrial areas for housing, and increase the amount of new construction plans. The authorities noted that the coalition agreement does address previous IMF recommendations to lower the MID but does not follow the previous IMF and Financial Stability Committee (FSC) recommendation to further lower LTV limits beyond the 100 percent ratio. The authorities noted that a lower LTV limit would make it more difficult, especially for younger households, to buy a house, while the middle-range rental market is already tight. The Dutch Central Bank and the Financial Market Authority noted that the current DSTI framework has procyclical elements. Increasing risk weights on mortgages in banks’ balance sheets and activating the countercyclical buffer could be considered if household debt continues to rise due to further tightening of the housing market.”

From the latest IMF report on the Netherlands:

“The housing market is dominated by social housing (with a wait time exceeding a decade in some cases) and owner-occupied houses with significant shortages. The absence of a robust private rental market leaves young households, in particular, with little alternative to purchasing owner-occupied housing with high leverage and thin financial buffers. Rent controls, regulations, and inadequate means-testing result in long waiting lists for social housing.

Posted by at 2:27 PM

Labels: Global Housing Watch

Friday, February 8, 2019

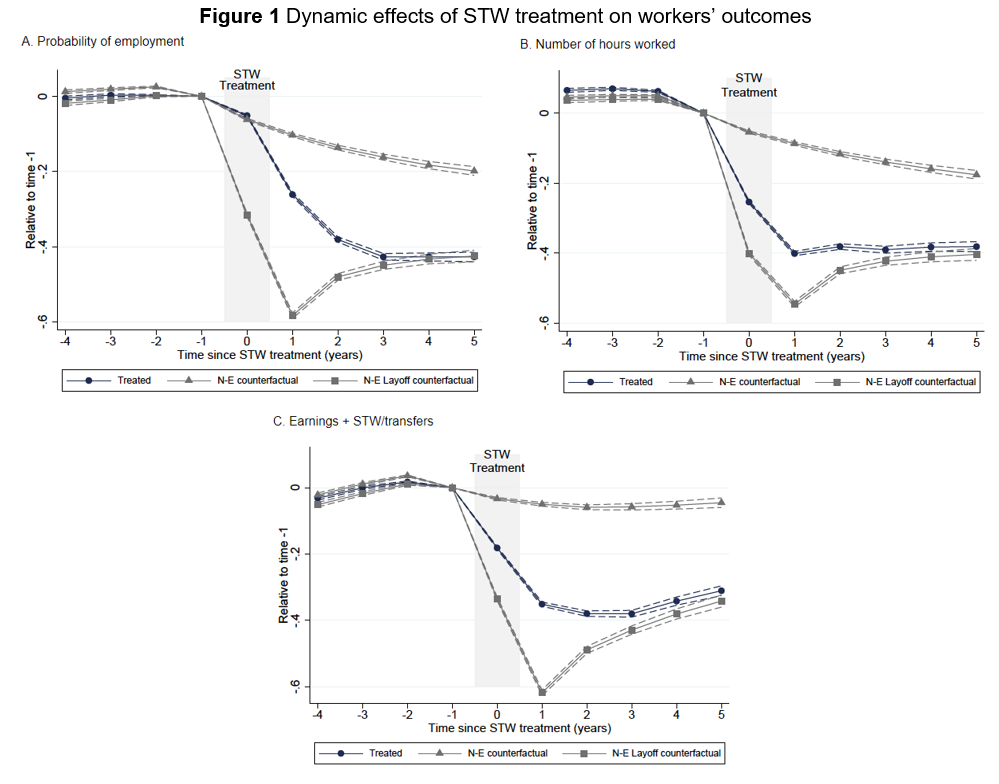

Subsidising labour hoarding in recessions: New evidence from Italy’s Cassa Integrazione

From a new VOXEU post:

“Figure 1 shows the evolution of various worker outcomes – the employment probability, the number of hours worked, and total earnings and transfers – around the time of STW treatment and compares workers who receive STW treatment (in blue) with two groups of similar workers who do not receive treatment. The workers in the grey square series are of particular interest – they are workers, similar to our treated group, but in firms who cannot access STW programmes, and who are laid-off. The figure shows that two years after STW treatment, there are no significant differences in the employment probability, earnings, and total income of workers who were treated by STW and workers who were laid-off. In other words, STW does not seem to provide any significant insurance to workers in the medium or long run.

How can we explain the very temporary nature of the impact of STW? The first answer lies in the selection of firms into these programmes. In the Italian context, firms that were at the bottom of the productivity distribution before the recession are three times more likely than higher-productivity firms to take up STW during the recession and employment effects for them are significantly smaller. These results are confirmed in the French context by Cahuc et al. (2018). This clearly suggests that STW predominantly targets firms that have permanently lower productivity and helps explain why keeping workers in these firms does not entail significant long-term benefits. More importantly, it suggests that, by preventing workers from moving from low- to high-productivity firms during recessions, STW may have significant negative reallocation effects in the labour market. Leveraging the rich spatial variation available in Italy across more than 600 local labour markets, we can estimate how an increase in the fraction of workers treated by STW in a local labour market affects employment outcomes of non-treated firms. Our results provide evidence of the presence of equilibrium effects of STW within labour markets. STW significantly decreases the employment growth and inflow rates of non-treated firms, and has a significant (although small) negative impact on TFP growth in the labour market.

Another reason that may explain the absence of long-term employment effects of STW in the Italian context is the nature of the Italian recession, which was long and protracted. It is likely that when a shock is more temporary, the effects of STW will be larger and will last longer, as the desire for labour hoarding is much greater for temporary shocks, especially when the cost of replacing or training workers is high.”

From a new VOXEU post:

“Figure 1 shows the evolution of various worker outcomes – the employment probability, the number of hours worked, and total earnings and transfers – around the time of STW treatment and compares workers who receive STW treatment (in blue) with two groups of similar workers who do not receive treatment. The workers in the grey square series are of particular interest – they are workers,

Posted by at 11:10 AM

Labels: Inclusive Growth

Fiscal Policy and Development : Human, Social, and Physical Investments for the SDGs

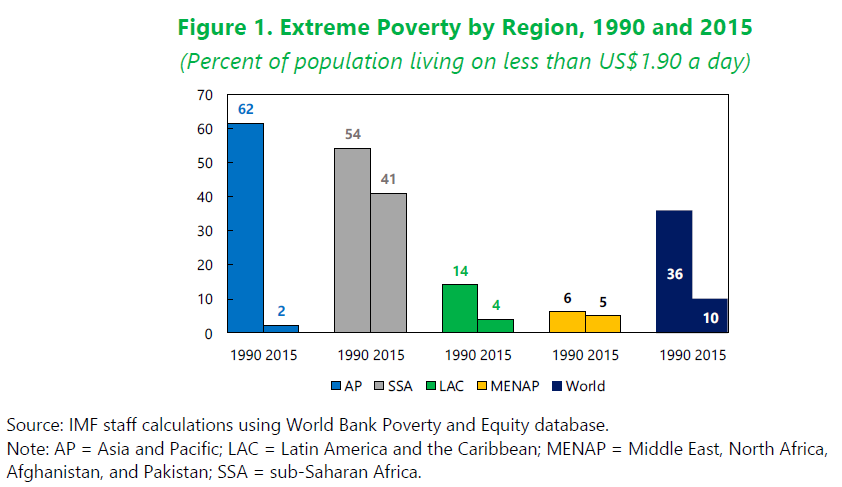

From a new IMF Staff Discussion Note on Sustainable Development Goals:

“In September 2015, world leaders gathered at the United Nations endorsed the 17 Sustainable Development Goals (SDGs) as a road map to more inclusive growth and development that respects the limits of nature. In this Staff Discussion Note we focus on investment in human, social, and physical capital, which are at the core of sustainable and inclusive growth and represent an important share of national budgets—specifically, education, health, roads, electricity, and water and sanitation.

The goal of this paper is to estimate the additional annual spending required for meaningful progress on the SDGs in these areas. Our estimates refer to additional spending in 2030, relative to a baseline of current spending to GDP in these sectors. Toward this end, we apply an innovative costing methodology to a sample of 155 countries: 49 low-income developing countries, 72 emerging market economies, and 34 advanced economies. And we refine the analysis with five country studies: Benin, Guatemala, Indonesia, Rwanda, and Vietnam.

Our main finding is that delivering on the SDG agenda will require additional spending in 2030 of US$0.5 trillion for low-income developing countries and US$2.1 trillion for emerging market economies.

There is a sharp contrast between the two groups. For emerging market economies, the average additional spending required represents about 4 percentage points of GDP. This is a considerable challenge, but in most cases these economies can rely on their own resources to achieve these SDGs. How it can be done is illustrated by the country study for Indonesia.

The challenge is much greater for low-income developing countries. Here, the average additional spending represents 15 percentage points of GDP. Some countries in this group—such as Vietnam—have additional spending needs similar to those of Indonesia and other emerging market economies. But others, including Rwanda and Benin, will require additional spending of more than 15 percentage points of GDP in 2030.

Countries themselves own the responsibility for achieving the SDGs, especially through reforms to foster sustainable and inclusive growth that will in turn generate the tax revenue needed. Efforts should focus on strengthening macroeconomic management, combating corruption and improving governance, strengthening transparency and accountability, and fostering enabling business environments.

Raising more domestic revenue is an essential component of this strategy. Increasing the tax-to-GDP ratio by 5 percentage points of GDP in the next decade is an ambitious but reasonable target in many countries.

Addressing spending inefficiencies is also critical—countries need to spend not only more, but better. We estimate that countries could save about as much through efficiency efforts as through tax reforms.

But in addition to domestic resources, the scale of the additional spending needs in low-income developing countries requires support from all stakeholders—including the private sector, donors, philanthropists, and international financial institutions. Delivering on official development assistance targets can help in closing development gaps in many LIDCs. A national reform agenda that maps the SDGs to national circumstances should articulate the complementary role of the various development partners.”

From a new IMF Staff Discussion Note on Sustainable Development Goals:

“In September 2015, world leaders gathered at the United Nations endorsed the 17 Sustainable Development Goals (SDGs) as a road map to more inclusive growth and development that respects the limits of nature. In this Staff Discussion Note we focus on investment in human, social, and physical capital, which are at the core of sustainable and inclusive growth and represent an important share of national budgets—specifically,

Posted by at 10:50 AM

Labels: Inclusive Growth

Subscribe to: Posts