Wednesday, July 10, 2019

Wealth Inequality and Private Savings in Germany

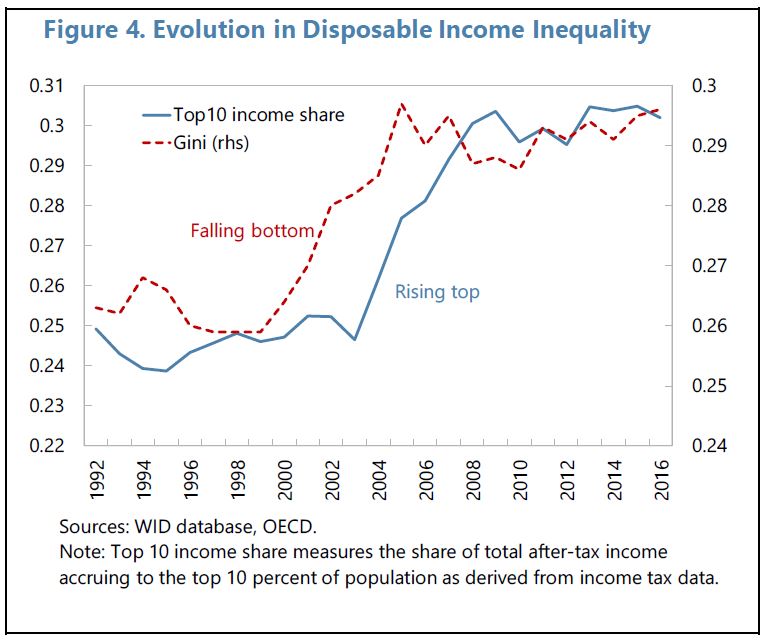

From latest IMF report on Germany:

“Does the large current account surplus in Germany reflect export-driven income gains that are evenly shared among the population? The evidence strongly suggests this is not the case and underscores the important role of German business wealth concentration in this context. As high corporate savings and underlying profits largely reflect capital income accruing to wealthy households and increasingly retained in closely-held firms, the buildup of external imbalance has been accompanied by widening top income inequality, rising private savings and compressed consumption rates.”

From latest IMF report on Germany:

“Does the large current account surplus in Germany reflect export-driven income gains that are evenly shared among the population? The evidence strongly suggests this is not the case and underscores the important role of German business wealth concentration in this context. As high corporate savings and underlying profits largely reflect capital income accruing to wealthy households and increasingly retained in closely-held firms, the buildup of external imbalance has been accompanied by widening top income inequality,

Posted by at 12:02 PM

Labels: Inclusive Growth

Monday, July 8, 2019

Grenada : Climate Change Policy Assessment

From the IMF’s latest report on Grenada:

“Grenada has made significant strides to counter climate change but meeting the daunting remaining challenges will require domestic policy actions and sustained international support. Climate change is an existential threat to Grenada. Increasing frequency and intensity of coastal storms threatens infrastructure and livelihoods, as do increased risk of coastal flooding and drought. Notably, Hurricane Ivan in 2004 caused damages of over 200 percent of GDP. Grenada has recognized this by placing climate resilience at the center of its policy making and forging strategic alliances with key global climate finance providers. However, the challenges facing the country remain daunting and will require large increases in international support, both financial and technical, to assist the Grenadian authorities turn their impressive resilience plans into action.

This Climate Change Policy Assessment (CCPA) takes stock of Grenada’s plans to manage its climate response, from the perspective of their macroeconomic and fiscal implications. The CCPA is a joint initiative by the IMF and World Bank to assist small states to understand and manage the expected economic impact of climate change, while safeguarding long-run fiscal and external sustainability. It explores the possible impact of climate change and natural disasters on the macroeconomy and the cost of Grenada’s planned response. It suggests macroeconomically relevant reforms that could strengthen the likelihood of success of the national strategy and identifies policy gaps and resource needs.

General preparedness for climate change. Grenada has made significant strides in preparedness. Its Nationally Determined Contribution (NDC) sets out an ambitious agenda for mitigation. The Climate Change Policy and National Adaptation Plan (NAP) provide costed detailed plans for adaptation and resilience building. The establishment of the Ministry of Climate Resilience in 2017 has further promoted mainstreaming of climate adaptation. However, implementation capacity remains a huge impediment to meeting NAP goals, particularly given Grenada’s tight fiscal constraints. Post-disaster activities and responsibilities are well-articulated but require formalization and more progress is required on financing. A Disaster Resilience Strategy (DRS) drawing on the recommendations of the CCPA and summarizing and synthesizing actions from other plans and strategies would help Grenada improve its readiness to cope with future disasters.

Mitigation. Grenada plans to progress on its mitigation pledge for the Paris Agreement in the near term by expanding the share of renewable energy in the power generation mix and by adopting energy efficiency measures including in the transport sector. However, progress has been slow and a finalized legal and regulatory framework is needed to provide incentives for this to occur. In addition, Grenada could consider using upstream fuel excise-based carbon taxation to reinforce price incentives towards energy efficiency paying due attention to distributional impacts, administrative efficiency and competitiveness. Feebates (tax-subsidy schemes integrated into existing excises) could further reinforce mitigation incentives.

Adaptation. Grenada’s adaptation strategy—the NAP—covers all infrastructure sectors, land, agroforestry, agriculture, fishing, food security, water, mangrove, marine, coral, health, and zone management. An estimated one-third of capital expenditures in 2019 budget already goes to resilience-building projects. However, progress is hindered by capacity constraints, in particular in investment project execution. Progress is being made on supporting policies and regulations but implementation and enforcement need to be strengthened, notably with regard to building codes and draining maintenance.

Financing. Grenada faces huge financing challenges to meet its ambitious climate change policy. The authorities have estimated financing needs at about US$500 million, equivalent to over 40 percent of 2018 GDP. Even if most mitigation investment can be financed by the private sector, the required adaptation investment of at least US$340 million out of the $500 million estimated by the authorities is difficult to reconcile with fiscal constraints and other priority needs, including general infrastructure maintenance and development. Proposed reforms to the Fiscal Responsibility Law (FRL) may open some space for increased revenue and loan-financed investment in resilient infrastructure but maintaining a safe debt level means that this will be limited. Maximizing use of available grant financing is therefore crucial for Grenada to ensure long term fiscal sustainability while meeting climate adaptation goals. Grenada has made some progress in beginning to access global climate financing and needs to build on this to maintain progress. However, as the availability of these funds for Grenada may be limited they will need to be supplemented by domestic revenue mobilization, available concessional loans and increased private sector participation remain key to any resource mobilization strategy.

Risk management. Grenada has well identified disaster and climate risks but does not yet have a comprehensive risk and contingent liability assessment. The authorities have put in place a number of elements of a comprehensive natural disaster risk layering strategy, including establishing contingency funds, participating in regional parametric insurance schemes and including a hurricane clause in debt restructuring agreements. However, indemnity and catastrophe insurance is underused in both the public and private sectors and Grenada has not established contingent lines of finance. Fiscal buffers also fall short of desirable levels. Grenada could enhance its risk management by putting place a National Natural Disaster Risk Financing Strategy as a key element of the broader DRS. This would guide future policy making on risk transfer and retention, including trade-offs between options and provide a framework for seeking increased international support.

National processes. The establishment of Ministry of Climate Resilience has helped to further strengthen the mainstreaming of climate-related projects. Climate resilience has been built into the public sector investment program framework as a key screening element, but in practice the weight given to climate resilience project prioritization and selection process is not yet clear. Weak project management capacity is a considerable drag on Grenada’s public investment management system. Grenada should establish an asset registry which would be the foundation for well managed asset insurance and disaster loss assessment.

Priority needs. To meet its mitigation plan, Grenada will need to rely heavily on private investment. Investment needs for adaptation require using as much grant and concessional financing (including contingent financing for natural disasters) as possible to maintain debt sustainability, while also creating space for private sector participation and increasing, where possible, domestic resource mobilization. Expansion of insurance coverage should also play a role but cannot substitute for investments in resilient infrastructure. Capacity building will also be crucial including for public investment management and to help complete the DRS, move toward carbon taxation, and enhance implementation of sectoral adaptation plans.

From the IMF’s latest report on Grenada:

“Grenada has made significant strides to counter climate change but meeting the daunting remaining challenges will require domestic policy actions and sustained international support. Climate change is an existential threat to Grenada. Increasing frequency and intensity of coastal storms threatens infrastructure and livelihoods, as do increased risk of coastal flooding and drought. Notably, Hurricane Ivan in 2004 caused damages of over 200 percent of GDP.

Posted by at 10:36 AM

Labels: Energy & Climate Change

Sunday, July 7, 2019

Capital Account Liberalization and Inequality

A new paper by Xiang Li and Dan Su highlights the possible relationship between capital account liberalization and inequality:

“This study adds empirical evidence to the literature linking external financial liberalization and income inequality. Its contributions are as follows. First, we provide evidence of the effect of opening the capital account on the income shares of different income groups. The dependent variable of previous studies is usually the nationwide Gini index. The use of income share data in this study cannot only show the effects on the overall distributional effect but also explain specifically which group benefits or loses the most. Second, we distinguish the direction and categories of capital account liberalization by using an updated measure from Fernández et al. (2016). The impacts of various dimensions of capital account liberalization can help narrow the discussion on specific opening policies . Third, we employ the difference-in-difference (DID) approach combined with propensity score matching (PSM) to estimate the impact of opening the capital account on income inequality in a 20-year window. In this way, we mitigate the endogeneity concern of conventional panel fixed effects models because the DID method tries to construct an experiment by selecting two groups of similar countries and then randomly liberalizing the capital account of the treated group while keeping that of the control group closed. In this way, we interpret the findings of this study one step closer to causality”

A new paper by Xiang Li and Dan Su highlights the possible relationship between capital account liberalization and inequality:

“This study adds empirical evidence to the literature linking external financial liberalization and income inequality. Its contributions are as follows. First, we provide evidence of the effect of opening the capital account on the income shares of different income groups. The dependent variable of previous studies is usually the nationwide Gini index.

Posted by at 8:55 PM

Labels: Inclusive Growth

Friday, July 5, 2019

Housing View – July 5, 2019

On cross-country:

- For now, residential-property prices are likely to keep rising – The Economist

- Rate cuts cannot curb property boom and bust – Financial Times

- Not just San Francisco: City housing markets all over the world are far too expensive – MarketWatch

- Why financialisation is not causing the housing crisis – Centre for Cities

On the US:

- Waiting for Affordable Housing in New York City – NBER

- Fewer Renters Believe They Are Likely to Ever Own a Home – Wall Street Journal

- Do land use restrictions increase restaurant quality and diversity? – American Enterprise Institute

- A City’s Bold Housing Plan – New York Times

- Changing supply elasticities and regional housing booms – Norges Bank

- I am Jane. Do I pay more in the housing market? – IDEAS

- AEI Housing Market Indicators release on March 2019 data – American Enterprise Institute

- The Government Created Housing Segregation. Here’s How the Government Can End It. – The American Prospect

- Housing: Elizabeth Warren v. John Cochrane – Econospeak

- Oregon Legislature Votes To Essentially Ban Single-Family Zoning – NPR

- The next housing bubble could come from this technology – Los Angeles Times

- The US Housing Finance System: A Flawed Giant – Harvard Joint Center for Housing Studies

- Housing affordability and quality create stress for Heartland families – Brookings Institute

- The Great Price Deceleration – John Burns

On other countries:

- [Brazil] Brazil’s house prices continue to fall – Global Property Guide

- [Egypt] Egypt’s house prices falling sharply – Global Property Guide

- [Macao] Macau’s amazing, incredible, soaring property prices – Global Property Guide

- [Netherlands] Brexit fuels Amsterdam property price boom – Financial Times

- [Singapore] Singapore to Keep Property Curbs for Now as Sell-Off Risk Remote – Bloomberg

- [United Kingdom] Speech by Communities Secretary Rt Hon James Brokenshire MP at the Chartered Institute of Housing conference – GOV

On cross-country:

- For now, residential-property prices are likely to keep rising – The Economist

- Rate cuts cannot curb property boom and bust – Financial Times

- Not just San Francisco: City housing markets all over the world are far too expensive – MarketWatch

- Why financialisation is not causing the housing crisis – Centre for Cities

On the US:

- Waiting for Affordable Housing in New York City – NBER

- Fewer Renters Believe They Are Likely to Ever Own a Home – Wall Street Journal

- Do land use restrictions increase restaurant quality and diversity?

Posted by at 9:29 AM

Labels: Global Housing Watch

Monday, July 1, 2019

Robots and Firms—A fresh perspective

From a new Vox piece on robots and firms:

“Frey and Osborne (2017) predict that almost 47% of total US employment could be automated in the nearest future. Focusing on the period from 1993 to 2007 and covering 17 different countries, Graetz and Michaels (2018) find that the growing intensity of robot use accounted for 15% of aggregate economy-wide productivity growth, contributed to significant growth in wages, and had virtually no aggregate employment effects. At the same time, Acemoglu and Restrepo (2017) investigate the US labour market between 1990 and 2007 and show that one additional robot per thousand workers reduces the employment to population ratio by about 0.2 percentage points and wages by 0.37 percent within commuting zones. Dauth et al. (2018) study Germany between 1994 and 2014 and find no effects on total employment, but identify a substantial shift in the composition of jobs away from manufacturing and towards business service”

From a new Vox piece on robots and firms:

“Frey and Osborne (2017) predict that almost 47% of total US employment could be automated in the nearest future. Focusing on the period from 1993 to 2007 and covering 17 different countries, Graetz and Michaels (2018) find that the growing intensity of robot use accounted for 15% of aggregate economy-wide productivity growth, contributed to significant growth in wages, and had virtually no aggregate employment effects.

Posted by at 10:27 PM

Labels: Inclusive Growth

Subscribe to: Posts