Friday, October 11, 2019

Housing View – October 11, 2019

On cross-country:

- The State of Housing in the EU 2019 – Housing Europe

- Overvalued in the Long Room: London – Financial Times

- Global Residential Cities Index-Q2 2019 – Knight Frank

On the US:

- Drilling Down: The Impact of Oil Price Shocks on Housing Prices – Federal Reserve Bank of Dallas

- Increasing Access to Affordable Housing Opportunities in Silicon Valley – Federal Reserve Bank of San Francisco

- Why the U.S. Needs a New Vision for Affordable Housing – University of Pennsylvania

- Federal government has dramatically expanded exposure to risky mortgages – Washington Post

- Will the Supreme Court Strike Down Inclusionary Zoning? – Citylab

- Can Tiny Houses Change The Housing Debate? – Forbes

- A Primer on Housing Finance Reform – The Center for Growth and Opportunity

- When Mandating Affordable Housing Makes Housing Less Affordable – Reason

- Restrictive zoning is impeding DC’s goal to build more housing – Brookings

- Homeownership Without the White Picket Fence? Hispanic Homeownership in the US – Harvard Joint Center for Housing Studies

- Michael Bennet Tries to Break Through With Affordable Housing Plan – Time

On other countries:

- [Canada] The Propagation of Regional Shocks in Housing Markets: Evidence from Oil Price Shocks in Canada – Federal Reserve Bank of Dallas

- [Czech Republic] Czech Republic: Property price growth strong, for now – ING

- [United Kingdom] Now is the time for the government to increase the supply of homes – The Guardian

On cross-country:

- The State of Housing in the EU 2019 – Housing Europe

- Overvalued in the Long Room: London – Financial Times

- Global Residential Cities Index-Q2 2019 – Knight Frank

On the US:

- Drilling Down: The Impact of Oil Price Shocks on Housing Prices – Federal Reserve Bank of Dallas

- Increasing Access to Affordable Housing Opportunities in Silicon Valley – Federal Reserve Bank of San Francisco

- Why the U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, October 10, 2019

Reigniting Growth in Emerging Market and Low-Income Economies: What Role for Structural Reforms?

From the IMF’s latest WEO analytical chapter:

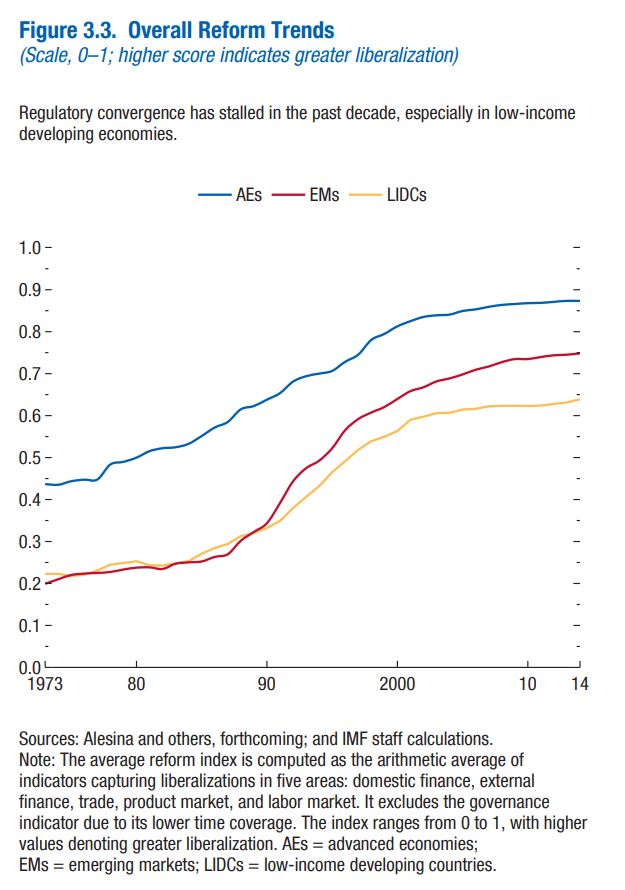

“The pace of structural reforms in emerging market and developing economies was strong during the 1990s, but it has slowed since the early 2000s. Using a newly constructed database on structural reforms, this chapter finds that a reform push in such areas as governance, domestic and external finance, trade, and labor and product markets could deliver sizable output gains in the medium term. A major and comprehensive reform package might double the speed of convergence of the average emerging market and developing economy to the living standards of advanced economies, raising annual GDP growth by about 1 percentage point for some time. At the same time, reforms take several years to deliver, and some of them—easing job protection regulation and liberalizing domestic finance—may entail greater short-term costs when carried out in bad times; these are best implemented under favorable economic conditions and early in authorities’ electoral mandate. Reform gains also tend to be larger when governance and access to credit—two binding constraints on growth—are strong, and where labor market informality is higher—because reforms help reduce it. These findings underscore the importance of carefully tailoring reforms to country circumstances to maximize their benefits.”

From the IMF’s latest WEO analytical chapter:

“The pace of structural reforms in emerging market and developing economies was strong during the 1990s, but it has slowed since the early 2000s. Using a newly constructed database on structural reforms, this chapter finds that a reform push in such areas as governance, domestic and external finance, trade, and labor and product markets could deliver sizable output gains in the medium term.

Posted by at 10:29 AM

Labels: Inclusive Growth

Tuesday, October 8, 2019

Housing market in Thailand

From the IMF’s latest report on Thailand:

“Credit and housing markets are also cooling down. Total credit growth—including credit from nonresidents—moderated from 5.8 percent in 2018 to 4.8 percent year-on-year in 2019:Q1, led by declines in corporate borrowing. While loans to households picked up in 2018 and remained buoyant through 2019:Q1—driven by auto loans and new mortgages housing loan demand softened following the tightening of loan-to-value (LTVs) in April 2019, and condo prices declined by 1¾ percent (y/y) also reflecting weaker foreign demand. The housing market is already going through a period of adjustment consistent with the broad-based cooling of the Thai economy.”

From the IMF’s latest report on Thailand:

“Credit and housing markets are also cooling down. Total credit growth—including credit from nonresidents—moderated from 5.8 percent in 2018 to 4.8 percent year-on-year in 2019:Q1, led by declines in corporate borrowing. While loans to households picked up in 2018 and remained buoyant through 2019:Q1—driven by auto loans and new mortgages housing loan demand softened following the tightening of loan-to-value (LTVs) in April 2019, and condo prices declined by 1¾ percent (y/y) also reflecting weaker foreign demand.

Posted by at 1:14 PM

Labels: Global Housing Watch

Monday, October 7, 2019

Capital City: Gentrification and the Real Estate State – Book Review

From LSE:

“The real estate industry is now worth $217 trillion, which is 36 times the value of all the gold in the world. What is more, it forms 60 per cent of global assets, and it is how one of the most powerful people on earth – US President Donald Trump – made his name. How, then, is the rise of the real estate industry transforming our cities and urban life? In Capital City, Samuel Stein argues that the emergence of the ‘real estate state’ has brought with it vicious gentrification, concomitant displacement of working-class people and remade our cities as temples of luxury development, rendering global cities increasingly inaccessible to all but an elite few. For Stein, ‘gentrification has become a household word and displacement an everyday fact of life’ (5).

Gentrification is, of course, a well-trodden path of academic inquiry. There is an extensive collection of books, articles and journal special editions spanning decades dedicated to the topic. Without treading on familiar ground, however, Stein approaches the issue at hand through the lens of urban planning. A central contention throughout is that, to understand gentrification, we must understand the rising political influence of real estate interests within local and national governments. Similarly, we are reminded of how these interests are actualised in a paradigm driven both by the growth imperative of capitalist development and the neoliberal state – that is, through urban planning and urban planners themselves. Early on in the book Stein, a trained planner himself, tells us that:

“This book is about planners in cities run by real estate. It describes how real estate came to rule, and what planners do under these circumstances. Planners provide a window into the practical dynamics of urban change” (6)

We can see, then, that Capital City is about understanding the dynamic that emerges between planners and real estate interests within the capitalist mode of production. It follows, therefore, that we must unpack the nature of urban planning itself. Stein’s genealogy of urban planning reveals that whilst the practice of planning is as old as human settlement, the profession of planning is a more recent phenomenon – and one with a rather oppressive history. ‘Proto-planners’, as Stein notes, advanced the ‘murderous westward expansion’ of the US (15), and planned and facilitated slavery through plantations and the systemic racial inequalities eminent from decades of ‘redlining’.”

Continue reading here.

From LSE:

“The real estate industry is now worth $217 trillion, which is 36 times the value of all the gold in the world. What is more, it forms 60 per cent of global assets, and it is how one of the most powerful people on earth – US President Donald Trump – made his name. How, then, is the rise of the real estate industry transforming our cities and urban life?

Posted by at 9:22 AM

Labels: Global Housing Watch

Changing business cycles: The role of women’s employment

From a VOX post by Stefania Albanesi:

“The US economy has been hampered over the last four decades by three trends: the productivity slowdown, the Great Moderation, and jobless recoveries. Economists seeking to explain these phenomena have generally looked to the impact that technological change has on labour demand. This column proposes an alternative explanation: the rise and stabilisation of women’s participation in the workforce, one of the most notable developments in the post-war US. Excluding gender differences in aggregate models of the US economy obscures our understanding of business cycle behaviour and economic performance.

The rise in women’s market work is one of the most notable economic developments in the post-war United States. Female participation rose from 37% in 1960 to a peak of 61% in 1997, and then flattened out, as shown in Figure 1. This phenomenon contributed substantially to the rise in aggregate hours per person in the US in the 1970s and 1980s. While a large literature has studied the determinants of the rise in women’s employment, the implications of this phenomenon for the aggregate performance of the US economy have been left largely unexplored. At the same time, several key properties of US business cycles changed over this period, and economists have yet to provide a comprehensive explanation of those changes. Three particularly puzzling phenomena stand out:

- the productivity slowdown in the 1970s (Jorgenson 1988) and the decline in the cyclical correlation between aggregate per capita hours and productivity (Gali and Gambetti 2009);

- the decline in the cyclicality of output and aggregate hours starting in the early 1980s, known as the Great Moderation (Stock and Watson 2002); and

- the sluggish growth in employment in the aftermath of recessions starting in the early 1990s, often referred to as jobless recoveries (Graetz and Michaels 2017).”

Continue reading here.

From a VOX post by Stefania Albanesi:

“The US economy has been hampered over the last four decades by three trends: the productivity slowdown, the Great Moderation, and jobless recoveries. Economists seeking to explain these phenomena have generally looked to the impact that technological change has on labour demand. This column proposes an alternative explanation: the rise and stabilisation of women’s participation in the workforce, one of the most notable developments in the post-war US.

Posted by at 9:20 AM

Labels: Inclusive Growth

Subscribe to: Posts