Thursday, December 23, 2021

Forecasting Facing Economic Shifts, Climate Change and Evolving Pandemics

New paper by Jennifer L. Castle , Jurgen A. Doornik and David F. Hendry

“By its emissions of greenhouse gases, economic activity is the source of climate change which affects pandemics that in turn can impact badly on economies. Across the three highly interacting disciplines in our title, time-series observations are measured at vastly different data frequencies: very low frequency at 1000-year intervals for paleoclimate, through annual, monthly to intra-daily for current climate; weekly and daily for pandemic data; annual, quarterly and monthly for economic data, and seconds or nano-seconds in finance. Nevertheless, there are important commonalities to economic, climate and pandemic time series. First, time series in all three disciplines are subject to non-stationarities from evolving stochastic trends and sudden distributional shifts, as well as data revisions and changes to data measurement systems. Next, all three have imperfect and incomplete knowledge of their data generating processes from changing human behaviour, so must search for reasonable empirical modeling approximations. Finally, all three need forecasts of likely future outcomes to plan and adapt as events unfold, albeit again over very different horizons. We consider how these features shape the formulation and selection of forecasting models to tackle their common data features yet distinct problems.”

New paper by Jennifer L. Castle , Jurgen A. Doornik and David F. Hendry

“By its emissions of greenhouse gases, economic activity is the source of climate change which affects pandemics that in turn can impact badly on economies. Across the three highly interacting disciplines in our title, time-series observations are measured at vastly different data frequencies: very low frequency at 1000-year intervals for paleoclimate, through annual, monthly to intra-daily for current climate;

Posted by at 8:16 AM

Labels: Forecasting Forum

Wednesday, December 22, 2021

Why low interest rates force us to revisit the scope and role of fiscal policy

In an article for the Peterson Institute for International Economics, economist Olivier Blanchard discusses 45 takeaways on the changing scope of fiscal policy and debt sustainability, in the light of consistently low interest rates. He also discusses three applications of the same- in the US, Japan, and Europe. Excerpts from the article:

- “A case of too little? The shift from output stabilization to debt reduction in the wake of the global financial crisis in Europe was too strong and too costly, reflecting an excessive weight on the costs of debt and an insufficient belief in the adverse effects of contractionary fiscal policy on demand and output.

- A case of just right? Faced with a strong case of secular stagnation, Japan has run large deficits for three decades and debt ratios have increased to very high levels, while the Bank of Japan remained at the effective lower bound. Was it the right strategy (if indeed it was a strategy)? The answer is a qualified yes, but, looking forward, the high debt ratios raise issues of debt sustainability. Alternative ways of boosting demand should be a high priority.

- A case of too much? To boost the US recovery from the initial COVID-19 shocks, the Biden administration embarked in 2021 on a major fiscal expansion. The strategy (again, if indeed it was a strategy) was for fiscal policy to increase demand and thus increase the neutral rate, and for monetary policy to delay the adjustment of the policy rate to the neutral rate, and in the process generate temporary inflation. Inflation has turned out to be much higher than expected. Was the fiscal expansion too strong? Was the strategy a mistake?”

Click here to read the full article.

In an article for the Peterson Institute for International Economics, economist Olivier Blanchard discusses 45 takeaways on the changing scope of fiscal policy and debt sustainability, in the light of consistently low interest rates. He also discusses three applications of the same- in the US, Japan, and Europe. Excerpts from the article:

- “A case of too little? The shift from output stabilization to debt reduction in the wake of the global financial crisis in Europe was too strong and too costly,

Posted by at 2:50 PM

Labels: Macro Demystified

Tuesday, December 21, 2021

The Latin American Pandemic

While the Covid-19 pandemic hit the world very hard, it is particularly well known that developing economies took the largest hit. In that, Latin America’s “long-standing fiscal and social deficits” have compounded the problem for policymakers, as discussed in a recent blog for VoxEU CEPR by Ilan Goldfajn (Chairman of the Board, Credit Suisse) and Eduardo Levy Yeyati (Dean, School of Government, Universidad Torcuato Di Tella).

“The pandemic also flagged two long-standing but often overlooked regional deficits: poor state capacity, and labour exclusion and informality. This explains the region’s worse performance during the pandemic: larger welfare costs and meager relative recovery. Not surprisingly, societies face growing indifference with political regimes (Latinobarómetro 2021), and social outbursts in several countries, such as Chile or Colombia, reveal dissatisfaction which will likely limit economic policy looking forward. On the one hand, many countries came from a period of increased civil unrest that reduced the government’s ability to restrict mobility. On the other hand, lack of political cohesion made it more difficult to implement restrictions, which inevitably led to lockdown fatigue and declining compliance. On top of that, a background of discontent and/or ongoing recessions clouded any perception of effective pandemic response.”

The article then moves on to discuss some areas that may possibly restrain constructive policy solutions, such as the limited size of the public sector given the already mounting primary deficit, populist policy temptations clashing with economically robust policies, etc.

Read the full blog here.

While the Covid-19 pandemic hit the world very hard, it is particularly well known that developing economies took the largest hit. In that, Latin America’s “long-standing fiscal and social deficits” have compounded the problem for policymakers, as discussed in a recent blog for VoxEU CEPR by Ilan Goldfajn (Chairman of the Board, Credit Suisse) and Eduardo Levy Yeyati (Dean, School of Government, Universidad Torcuato Di Tella).

“The pandemic also flagged two long-standing but often overlooked regional deficits: poor state capacity,

Posted by at 8:57 AM

Labels: Inclusive Growth, Macro Demystified

Monday, December 20, 2021

VIDEO: Discussing Global Recovery from the Pandemic with Gita Gopinath

The National Council of Applied Economic Research (NCAER) recently hosted Dr. Gita Gopinath, currently serving as the Chief Economist at the IMF for a discussion on the outlook for global growth in 2022. Among other things, the discussion touched upon topics like vaccination for protection against Covid-19, inflationary pressures in several countries, and the unique set of challenges before policymakers.

Watch the full video here.

The National Council of Applied Economic Research (NCAER) recently hosted Dr. Gita Gopinath, currently serving as the Chief Economist at the IMF for a discussion on the outlook for global growth in 2022. Among other things, the discussion touched upon topics like vaccination for protection against Covid-19, inflationary pressures in several countries, and the unique set of challenges before policymakers.

Watch the full video here.

Posted by at 9:12 AM

Labels: Inclusive Growth, Macro Demystified

Sunday, December 19, 2021

Where Can Residential Real Estate Investors Find the Most Potential ROI?

From First American:

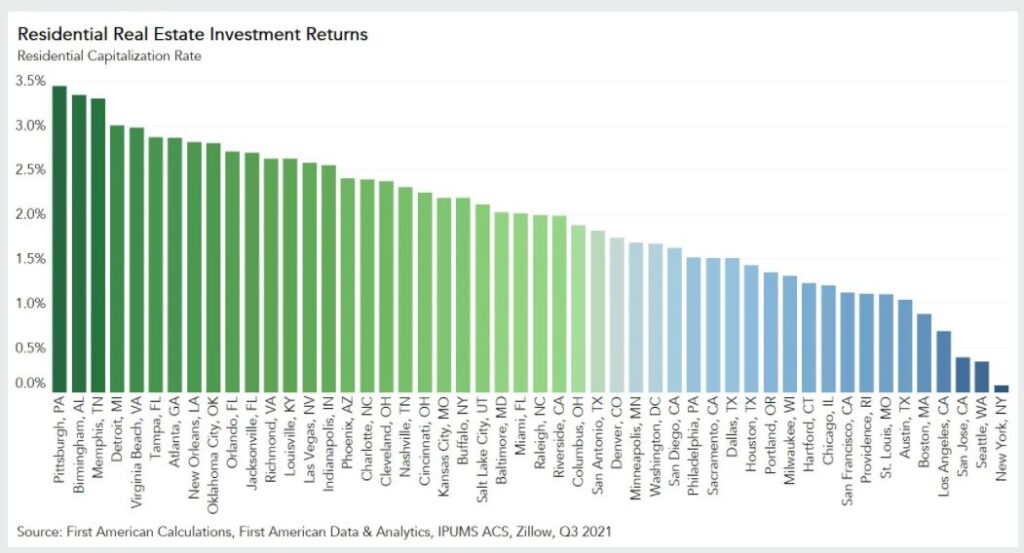

“Over the past year, increasing investor activity in residential real estate, particularly in single-family homes, has drawn a lot of attention. News of large institutional investors snapping up single-family homes underscored this summer’s historically hot housing market. Investors now own an estimated 2 percent of single-family rental housing units in the U.S., but investor activity varies significantly across markets. Adapting a metric commonly used for measuring the return on investment for commercial real estate can help identify the most attractive markets for residential real estate investors.

Housing’s Investment Return

Investors in commercial real estate often use a concept called the capitalization rate (cap rate) to calculate their potential rate of return on a real estate investment. The cap rate measures the net operating income of a property – its rental income less any operating costs, such as property taxes, insurance, and maintenance and repair costs – compared to the value of the property. Similar to the yield on a bond or the rate of return on an investment, the higher the cap rate, the more profitable the investment. While commonly calculated for commercial real estate transactions, it can be applied to residential real estate as well.

To calculate the typical market-level residential cap rate, take the median residential market rent and assume that the property will be vacant for three of the 12 months of the year (the typical vacancy assumption mortgage lenders use when underwriting a residential investment property), leaving an investor with nine months of collected rent. After accounting for property costs – property taxes, maintenance costs and annual homeowner’s insurance premium – we are left with estimated total rental income. Dividing the estimated total rental income by the median home sale price in each market yields a residential cap rate.

Which Markets Offer the Highest Return?

Breaking down the cap rate for the median single-family home in each of the top 50 U.S. markets reveals the residential housing markets that are potentially the most profitable from a real estate investment perspective. Of the top 50 U.S. markets, the five markets with the highest cap rates in the third quarter of 2021 were Pittsburgh (3.4 percent), Birmingham, Ala. (3.3 percent), Memphis, Tenn. (3.3 percent), Detroit (3 percent), and Virginia Beach, Va. (3 percent). The five markets with the lowest cap rates were New York (0.1 percent), San Jose, Calif. (0.3 percent), San Francisco (0.4 percent), Los Angeles (0.7 percent), and Boston (0.9 percent).”

Continue reading here.

From First American:

“Over the past year, increasing investor activity in residential real estate, particularly in single-family homes, has drawn a lot of attention. News of large institutional investors snapping up single-family homes underscored this summer’s historically hot housing market. Investors now own an estimated 2 percent of single-family rental housing units in the U.S., but investor activity varies significantly across markets. Adapting a metric commonly used for measuring the return on investment for commercial real estate can help identify the most attractive markets for residential real estate investors.

Posted by at 9:14 AM

Labels: Global Housing Watch

Subscribe to: Posts