Monday, January 3, 2022

Correlates of declining income inequality in emerging and developing nations

In an upcoming publication for World Development titled, ‘The correlates of declining income inequality among emerging and developing economies during the 2000s’ (2022), author Edward Anderson of the University of East Anglia discusses patterns that were frequently observed in countries that experienced declining levels of income inequality.

Among the most significant results of the paper, one states that “the tendency toward declining inequality in the 2000s was stronger in countries with higher initial levels of inequality and larger increases in relative agricultural productivity, country-specific primary commodity prices, and remittance inflows.” (Furceri and Loungani, 2018) “The results suggest that the challenge now facing many emerging and developing countries is how to sustain the reductions in inequality achieved since the early 2000s, given the decline in commodity prices since 2015, and the social and economic repercussions of the COVID-19 pandemic”, the paper adds.

Click here to read the full paper.

In an upcoming publication for World Development titled, ‘The correlates of declining income inequality among emerging and developing economies during the 2000s’ (2022), author Edward Anderson of the University of East Anglia discusses patterns that were frequently observed in countries that experienced declining levels of income inequality.

Among the most significant results of the paper, one states that “the tendency toward declining inequality in the 2000s was stronger in countries with higher initial levels of inequality and larger increases in relative agricultural productivity,

Posted by at 12:16 PM

Labels: Inclusive Growth

Sunday, January 2, 2022

The new consensus of economists is further to the left

They say economists rarely agree on one thing.

However, now this statement may not hold true as before. Based on a survey of members of the American Economic Association, a paper by Doris Geide-Stevenson and Alvaro La Parra Perez of the Weber State University compares the academic positions of economists over four decades.

“The main result is an increased consensus on many economic propositions, specifically the appropriate role of fiscal policy in macroeconomics and issues surrounding income distribution. Economists now embrace the role of fiscal policy in a way not obvious in previous surveys and are largely supportive of government policies that mitigate income inequality. Another area of consensus is concern with climate change and the use of appropriate policy tools to address climate change.”

Click here to download the paper and here to be a part of the discussion on it.

They say economists rarely agree on one thing.

However, now this statement may not hold true as before. Based on a survey of members of the American Economic Association, a paper by Doris Geide-Stevenson and Alvaro La Parra Perez of the Weber State University compares the academic positions of economists over four decades.

“The main result is an increased consensus on many economic propositions, specifically the appropriate role of fiscal policy in macroeconomics and issues surrounding income distribution.

Posted by at 10:33 AM

Labels: Inclusive Growth, Macro Demystified

Saturday, January 1, 2022

Okun’s Law in Liechtenstein

A 2021 report published by the Financial Market Authority Liechtenstein discusses the weak relationship between national output and unemployment in the country, given by Okun’s law in economic theory. The report deliberates upon this phenomenon as follows:

“One explanation for the missing link between employment and the business cycle is a shortage of skilled labor. In addition to labor market regulations, the decoupling of the business cycle and employment can be explained by hiring costs associated with search frictions that tend to have increased over the last decades (Ball, Leigh, and Loungani, 2017). The Swiss Employment Barometer indicates that skilled labor is especially difficult to find in sectors such as metal or machinery industries, which are relatively large in Liechtenstein. Against this background, it is plausible that the decoupling between employment and business cycle dynamics progressed in a stronger manner and earlier in Liechtenstein compared to other advanced economies.”

Click here to read the full report.

A 2021 report published by the Financial Market Authority Liechtenstein discusses the weak relationship between national output and unemployment in the country, given by Okun’s law in economic theory. The report deliberates upon this phenomenon as follows:

“One explanation for the missing link between employment and the business cycle is a shortage of skilled labor. In addition to labor market regulations, the decoupling of the business cycle and employment can be explained by hiring costs associated with search frictions that tend to have increased over the last decades (Ball,

Posted by at 9:27 AM

Labels: Macro Demystified

Friday, December 31, 2021

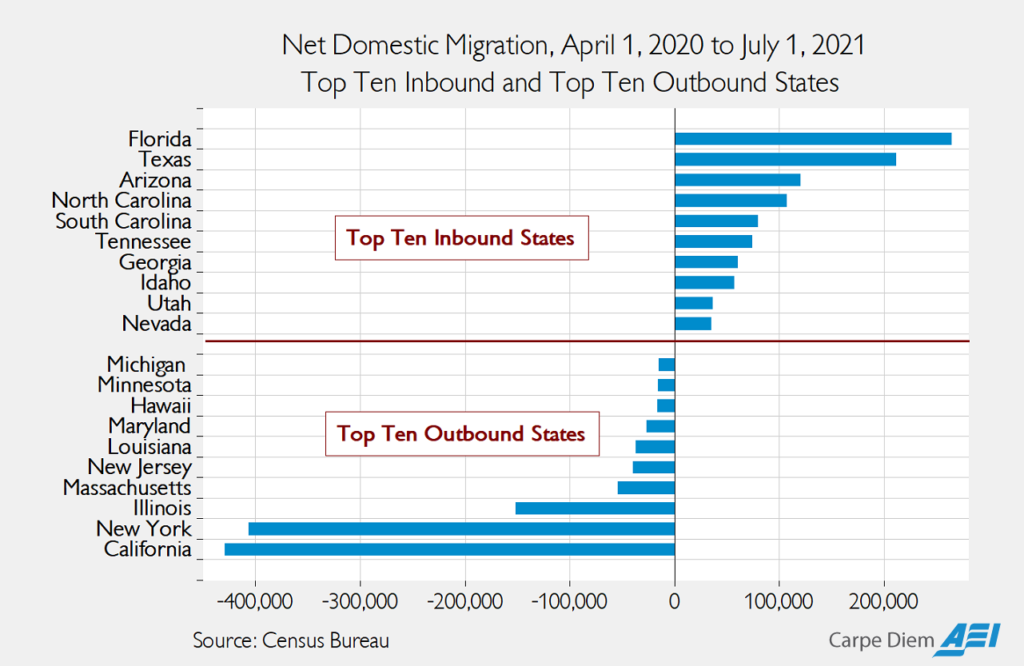

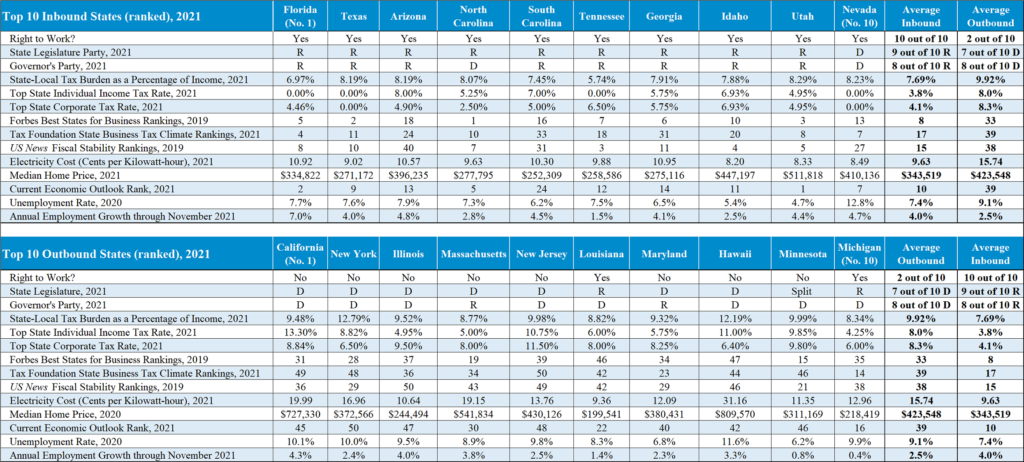

Moving on up? Understanding migration to red states in 2021

In a column for the public policy think tank, American Enterprise Institute, the top ten inbound and top ten outbound US states for the year 2021 have been compared using new data on net domestic migration data from the US Census Bureau.

Click here to read the full report.

In a column for the public policy think tank, American Enterprise Institute, the top ten inbound and top ten outbound US states for the year 2021 have been compared using new data on net domestic migration data from the US Census Bureau.

Source: American Enterprise Institute

Source: American Enterprise Institute

Click here to read the full report.

Posted by at 1:08 PM

Labels: Inclusive Growth

Thursday, December 30, 2021

Measuring US Core Inflation: The Stress Test of COVID-19

Laurence M. Ball of the Johns Hopkins University, and Daniel Leigh, Prachi Mishra, and Antonio Spilimbergo of the International Monetary Fund write about the core inflation rate in the US in a paper for the National Bureau of Economic Research (NBER).

Abstract:

“Large price changes in industries affected by the COVID-19 pandemic have caused erratic fluctuations in the U.S. headline inflation rate. This paper compares alternative approaches to filtering out the transitory effects of these industry price changes and measuring the underlying or core level of inflation over 2020-2021. The Federal Reserve’s preferred measure of core, the inflation rate excluding food and energy prices, has performed poorly: over most of 2020-21, it is almost as volatile as headline inflation. Measures of core that exclude a fixed set of additional industries, such as the Atlanta Fed’s sticky-price inflation rate, have been less volatile, but the least volatile have been measures that filter out large price changes in any industry, such as the Cleveland Fed’s median inflation rate and the Dallas Fed’s trimmed mean inflation rate. These core measures have followed smooth paths, drifting down when the economy was weak in 2020 and then rising as the economy has rebounded.”

Click here to read the full paper.

Laurence M. Ball of the Johns Hopkins University, and Daniel Leigh, Prachi Mishra, and Antonio Spilimbergo of the International Monetary Fund write about the core inflation rate in the US in a paper for the National Bureau of Economic Research (NBER).

Abstract:

“Large price changes in industries affected by the COVID-19 pandemic have caused erratic fluctuations in the U.S. headline inflation rate. This paper compares alternative approaches to filtering out the transitory effects of these industry price changes and measuring the underlying or core level of inflation over 2020-2021.

Posted by at 9:41 AM

Labels: Macro Demystified

Subscribe to: Posts