Sunday, January 9, 2022

Should Blacks Apply for Mortgage Loans at the End of the Month?

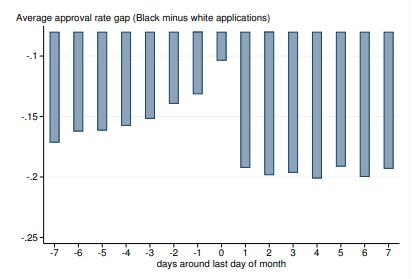

A new paper studies mortgage loan approval rates for white and blacks. “In the first seven days of the month, Black applicants have 20 percentage point lower approval rates than white applicants. The approval gap declines to just 10 percentage points on the last day the month,” as shown in the figure below. Why? The authors examine the hypothesis that this occurs because loan officers have monthly volume quotas, which gives “them less scope to apply subjective preferences” at the end of the month. They calculate “an upper bound for the costs of discrimination”: “if the Black approval gap on each day of the month was as small as it was on the last day, approximately 1.4 million more Black applicants would have been approved between 1994 and 2018,” corresponding to over $200 billion in total loan volume.

The figure reports approval rates, which we define as the fraction of loans that are originated out of the total number of applications (excluding withdrawn applications). We present the difference between the Black approval rate and the white approval rate on each day.

A new paper studies mortgage loan approval rates for white and blacks. “In the first seven days of the month, Black applicants have 20 percentage point lower approval rates than white applicants. The approval gap declines to just 10 percentage points on the last day the month,” as shown in the figure below. Why? The authors examine the hypothesis that this occurs because loan officers have monthly volume quotas, which gives “them less scope to apply subjective preferences” at the end of the month.

Posted by at 1:02 PM

Labels: Global Housing Watch

Alvin Rabushka: A link to his work

Posted by at 8:15 AM

Labels: Profiles of Economists

Saturday, January 8, 2022

Emerging-Market Central Bank Purchases Can be Effective but Carry Risks

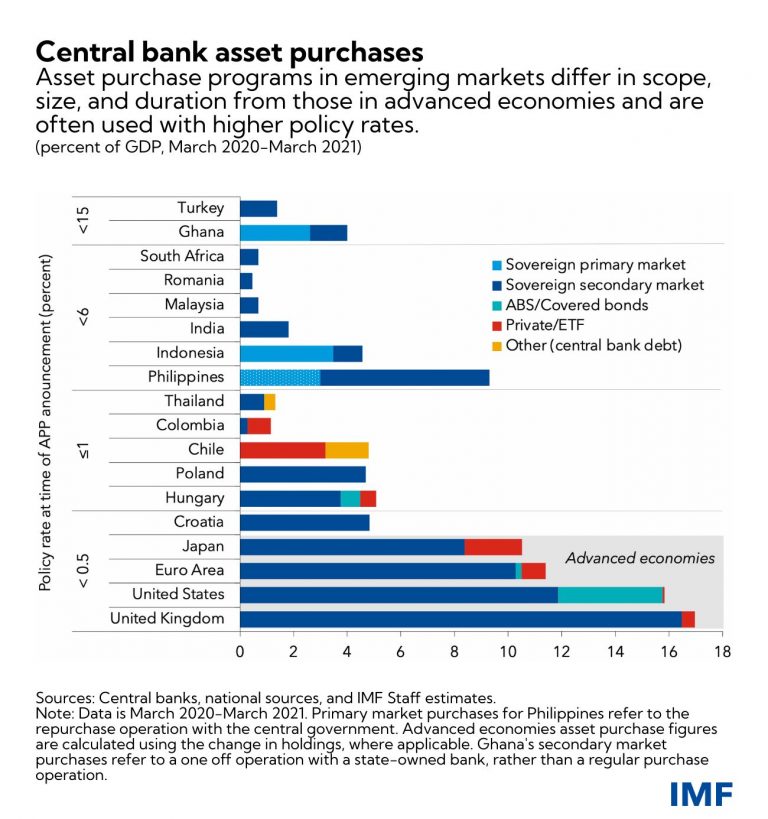

In a new IMF blog (2022), Tobias Adrian et al write about the effectiveness and risks of counter-cyclical monetary policy measures taken by central banks in emerging markets, specifically asset purchases.

‘Targeted asset purchases helped emerging markets manage financial distress during the COVID-19 crisis without noticeable capital outflow and exchange rate pressures but also pose significant risks, including the risk to central banks’ own balance sheets and governments pressuring central banks to act in a certain way’. It then goes on to discuss some principles for asset purchases and direct financing that may help central banks override this problem.

Click here to read the full blog.

In a new IMF blog (2022), Tobias Adrian et al write about the effectiveness and risks of counter-cyclical monetary policy measures taken by central banks in emerging markets, specifically asset purchases.

‘Targeted asset purchases helped emerging markets manage financial distress during the COVID-19 crisis without noticeable capital outflow and exchange rate pressures but also pose significant risks, including the risk to central banks’ own balance sheets and governments pressuring central banks to act in a certain way’.

Posted by at 9:29 AM

Labels: Macro Demystified

Friday, January 7, 2022

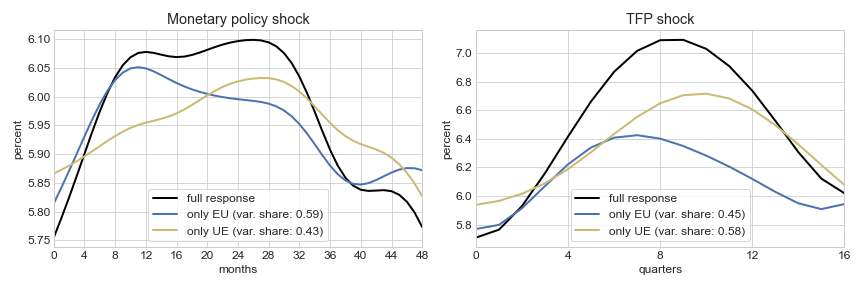

The unemployment-risk channel in business cycle fluctuations

Source: VoxEU CEPR

“Early signs of a recession can lead to a negative feedback loop, with workers’ concerns about unemployment dampening demand and thus deepening the recession. This column uses a heterogeneous agent model to quantify the importance of the ‘unemployment-risk’ channel for business cycle fluctuations in the US economy. It shows that the channel accounts for around one-third of observed unemployment fluctuations. As the demand amplification through precautionary savings is inefficient, this finding provides an additional rationale for stabilisation policies by policymakers. “

Figure: Estimated response of unemployment to monetary policy and total factor productivity (TFP) shocks

Click here to read the full article.

Source: VoxEU CEPR

“Early signs of a recession can lead to a negative feedback loop, with workers’ concerns about unemployment dampening demand and thus deepening the recession. This column uses a heterogeneous agent model to quantify the importance of the ‘unemployment-risk’ channel for business cycle fluctuations in the US economy. It shows that the channel accounts for around one-third of observed unemployment fluctuations. As the demand amplification through precautionary savings is inefficient, this finding provides an additional rationale for stabilisation policies by policymakers.

Posted by at 11:08 AM

Labels: Inclusive Growth, Macro Demystified

Housing View – January 7, 2022

On cross-country:

- How long can the global housing boom last? Three fundamental forces mean it could endure for some time yet – The Economist

On the US:

- ‘There may be a slight correction in pricing.’ Real estate attorneys and economists on what buyers need to know about the housing market in 2022 – Market Watch

- Home Values in Already Hot U.S. Market to Surge 14% This Year, Zillow Says. Tampa and Jacksonville in Florida and Raleigh in North Carolina are projected to be most in-demand. – Bloomberg

- Why Tampa will be 2022’s Hottest Market – Zillow

- Real estate market in 2022 will ‘remain very strong,’ expert says – Yahoo Finance

- AEI housing market indicators, December 2021 – American Enterprise Institute

- Home Ownership More Affordable Than Renting in Majority of U.S. Housing Markets – ATTOM

- What’s Going on With Housing Prices? A Deep Dive into the Discrepancy Between Home Price Indexes, Private Sector Rental Data, and Official CPI Rent Indexes – Apricitas

On China

- China Property Tax Trial Likely Delayed During Real Estate Slump – Bloomberg

On other countries:

- [Australia] As stimulus wanes, focus on productivity and house prices – Financial Review

- [Australia] Australia Housing Boom Fades as Melbourne, Sydney Pull Back – Bloomberg

- [Australia] Australia’s housing market faces headwinds as supply likely to outpace demand, analysts say – South China Morning Post

- [Ireland] The impact of COVID-19 on house prices in Northern Ireland: price persistence, yet divergent? – Journal of Property Research

- [New Zealand] New Zealand Average Home Price Exceeds NZ$1 Million for First Time – Bloomberg

- [Taiwan] Taiwan Central Bank Split on Using Rates to Rein in Housing Market – Bloomberg

On cross-country:

- How long can the global housing boom last? Three fundamental forces mean it could endure for some time yet – The Economist

On the US:

- ‘There may be a slight correction in pricing.’ Real estate attorneys and economists on what buyers need to know about the housing market in 2022 – Market Watch

- Home Values in Already Hot U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Subscribe to: Posts