Friday, May 13, 2022

Housing Market in New Zealand

From the IMF’s latest report on New Zealand:

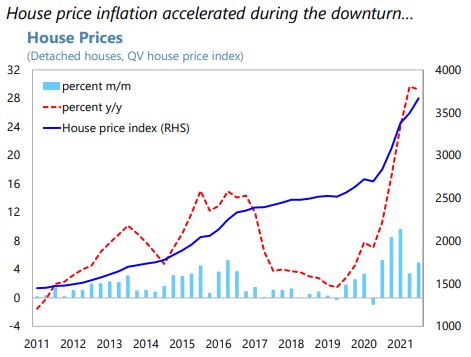

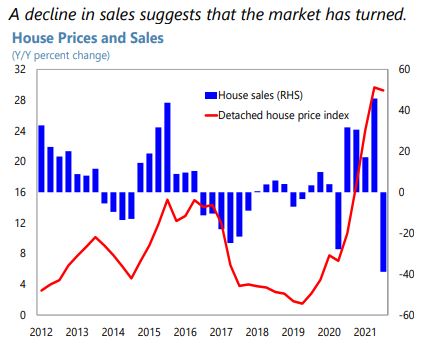

“House prices have peaked and are expected to correct. The market is turning given that important drivers over previous years, such as low mortgage rates and easy credit availability, are now reversing (…). The recent trend of falling sales volumes and mortgage lending is expected to continue, supporting a house price correction, although the period and intensity are difficult to estimate.

Rising mortgage rates and recent policy actions are curbing demand. In response to actual and expected withdrawal of monetary stimulus, standard mortgage rates rose by between 40 and 150 bps in 2021H2. The removal of property investors’ tax deductibility of mortgage interest and the extension of the minimum holding period to exempt capital gains on investment properties from income tax have contributed to a decline in investor demand. The RBNZ re-introduced loan-to-value ratio (LVR) limits on mortgages in March 2021 and tightened them in May and November. The December 2021 amendments to the Credit Contracts and Consumer Finance Act (CCCFA), designed to protect borrowers and strengthen the consumer credit regulatory regime, had the unintended effect of tightening credit conditions further. These developments contributed to a significant decline in mortgage lending (-31 percent y/y in March 2022), with new loans to investors and highly leveraged buyers (LVR exceeding 80 percent) declining more rapidly (-44 percent and -56 percent y/y, respectively). The RBNZ intends to implement additional MPMs for potential future use to broaden its toolkit. A framework to introduce DTI ceilings will be released by end-2022 for implementation by mid-2023. The RBNZ is also looking at the possible use of a floor on test interest rates to assess borrowers’ ability to meet debt service obligations.

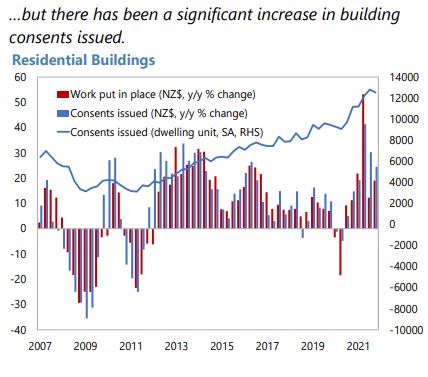

Efforts are ongoing to improve housing supply. A NZ$3.8 billion (around 1.1 percent of GDP) allocation was made to the Housing Acceleration Fund to increase housing supply and improve affordability. Amendments to the Resource Management Act (RMA) in October 2021 allow for higher-density housing construction without requiring resource consent, making it easier to build new homes. However, these measures will take time to bear fruit: a cost-benefit appraisal by the Treasury estimated that about 75,000 additional dwellings would be built in the next 5-8 years, with more than 200,000 additional dwellings available in 20 years. The government is also in the process of reforming the RMA, which should streamline planning processes. There are plans to boost effective land supply by incentivizing local authorities to approve new housing projects faster.

Staff Views

Tackling housing imbalances requires a comprehensive approach, and recent initiatives will help address these imbalances. Achieving long-term housing sustainability and affordability depends critically on freeing up land supply, improving planning and zoning, and fostering infrastructure investments to enable fast-track housing developments and lower construction costs. There is a need for continued spending on land, infrastructure, and housing, including financial incentives that enable and incentivize local councils and iwi (Māori tribal organizations) to provide infrastructure for new developments. Increasing the stock of social housing also remains important in the near term, while supply constraints are addressed over time.

A moderation of prices is widely expected, and macroprudential policy should be adjusted commensurate with the evolution of financial stability risks. The use of macroprudential measures to address the financial stability impact of surging house prices has been appropriate. LVR restrictions have been effective in making lending for housing more cautious. Restrictions could be relaxed in case of a stronger-than-expected downturn in the housing market. Financial stability risks from a sharp downturn in the housing market are limited given high bank capitalization, but pockets of vulnerability, particularly among recent borrowers, may exist. More broadly, in case of a sharp downturn, potentially reinforced by a faster rise in interest rates, there could be a significant impact on consumption through wealth and confidence effects. A more extensive MPM toolkit, including the ability to readily implement DTI ceilings and loan serviceability test interest rate requirements when warranted, would be useful in addressing future risks.

Authorities’ Views

The authorities stressed that, while the housing cycle had likely turned, improving affordability remained a key priority. While prices are expected to decline in 2022, this only partially reverses the very large increases of recent years and will therefore not make a significant impact on affordability. A comprehensive approach covering the demand and supply sides of housing is underway, with more initiatives planed under the wider review of the RMA and laid out in the National Policy Statement on Urban Development. The Housing Acceleration Fund will provide funding at the local level for infrastructure development, and the first tranche of projects is likely to be approved soon. The authorities emphasized their commitment to invest in social housing. They agreed that the CCCFA amendments may have impacted credit conditions, though the effect is hard to quantify. They noted that clarifications have already been issued, with further changes being considered in consultation with the industry.”

From the IMF’s latest report on New Zealand:

“House prices have peaked and are expected to correct. The market is turning given that important drivers over previous years, such as low mortgage rates and easy credit availability, are now reversing (…). The recent trend of falling sales volumes and mortgage lending is expected to continue, supporting a house price correction, although the period and intensity are difficult to estimate.

Rising mortgage rates and recent policy actions are curbing demand.

Posted by at 6:49 PM

Labels: Global Housing Watch

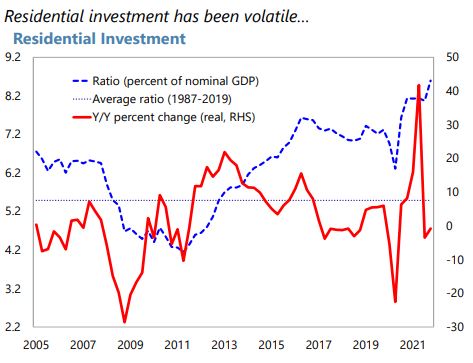

New Zealand: Addressing the Housing Cycle

From the IMF’s latest report on New Zealand:

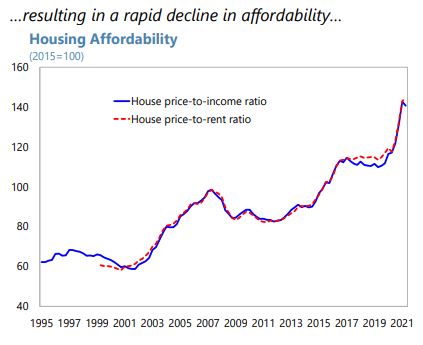

“Despite the COVID-19 pandemic, housing prices have surged in New Zealand in 2020 and much of 2021, more so than in other countries, raising affordability concerns. This was driven by demand-side factors such as record low mortgage rates, easy credit availability, COVID-related pent-up demand, and lagged effect of population growth interacting with inelastic supply. The housing market is now turning given that many of these factors are reversing, in part due to recent policy actions, but the extent of moderation remains uncertain. Rising mortgage rates are set to further dent affordability and make borrowers vulnerable to mortgage repricing risks, but financial stability risks from the housing market would likely be manageable as banks are well capitalized. Policy should focus on increasing supply and ensuring affordability, including through the provision of public social housing. Macroprudential policy should be adjusted commensurate with the evolution of the housing cycle and financial stability risks, while the planned expansion of the macroprudential toolkit may prove useful for future use.”

From the IMF’s latest report on New Zealand:

“Despite the COVID-19 pandemic, housing prices have surged in New Zealand in 2020 and much of 2021, more so than in other countries, raising affordability concerns. This was driven by demand-side factors such as record low mortgage rates, easy credit availability, COVID-related pent-up demand, and lagged effect of population growth interacting with inelastic supply. The housing market is now turning given that many of these factors are reversing,

Posted by at 6:33 PM

Labels: Global Housing Watch

Housing View – May 13, 2022

On cross-country:

- Which housing markets are most exposed to the coming interest-rate storm? The pain of rising mortgage repayments will be harder to bear in some places than in others – The Economist

- Wages Can’t Keep Up With Spike in Housing Prices. Across the globe, the 10 cities that experienced the largest drops in affordability in 2021 were all in the U.S., new research shows – New York Times

- Grantham: “Day of reckoning” coming for global housing markets – Macro Business

- When were U.S. home prices at their worst? – Marginal Revolution

On the US:

- US homebuyers stretch finances to beat rising rates in hot market. Shoppers settle for less space and take second jobs in response to declining affordability – FT

- How Hurricanes Sweep Up Housing Markets: Evidence from Florida – SSRN

- The Housing Market Is Passing an Inflection Point This Spring, on the Way to More Balanced Conditions – Zillow

- For Tens of Millions of Americans, the Good Times Are Right Now. Their houses are piggy banks, their retirement accounts are up and their bosses are eager to please. When the boom ends, everything will change. – New York Times

- Long Covid in Real Estate Weighs on Core Inflation. Shelter rents are still rising and will offset falls in prices elsewhere; any uptick in headline inflation is likely to trigger another bout of market volatility. – Bloomberg

- Building Materials Prices Move Higher, Up 19% Year-over-Year – NAHB

- Multifamily Rent Growth Slow to Decelerate – Yardi Matrix

- Fed Policy Helped Distressed Homeowners But Wasn’t a Cure-All – UCLA

- Does Affordable Housing Lead to Electoral Backlash? – Princeton University

- Mortgages drive increase in US household debt to nearly $16tn. Credit card balances stand $71bn higher than a year ago but New York Fed says borrowers are in ‘very good shape’ – FT

On China

- Chinese property developer Sunac defaults as lockdowns hit house sales. Beijing’s pandemic restrictions have worsened a liquidity crisis in real estate – FT

On other countries:

- [Australia] Seven downsides to Australia’s dangerous property obsession. Home ownership creates unbalanced growth and deceptive prosperity while contributing to structural problems – The Guardian

- [Australia] Is housing our greatest policy fail? – Financial Review

- [Australia] Australia’s Housing Market Faces Its Biggest Test in 30 Years. Property prices expected to fall, building slow on rate rises. Declining home values a challenge for winner of May 21 ballot – Bloomberg

- [Belgium] The impact of changes in dwelling characteristics and housing preferences on house price indices – Central Bank of Belgium

- [Canada] Trudeau to outlaw foreign home buyers in Canada as affordability fears heat up. Housing experts say it’s not the right fix: “This is kind of scapegoating.” – Politico

- [Canada] How Do Mortgage Rate Resets Affect Consumer Spending and Debt Repayment? Evidence from Canadian Consumers – Dallas Fed

- [New Zealand] New Zealand May Eliminate Housing Shortage Within Years: Westpac – Bloomberg

- [New Zealand] As property market cools, New Zealand’s recent home buyers tighten belts – Reuters

- [Singapore] Singapore’s Hot Housing Market. Despite government’s various efforts to restrain the price of housing, costs have risen considerably since the beginning of the COVID-19 pandemic – The Diplomat

- [Spain] Mallorca, where mountains tower and house prices climb. With the easing of Covid rules, wealthy overseas buyers are back on the Balearic island, pricing out locals – FT

- [Turkey] Cheap home loans raise Turkey’s inflation roof – Reuters

- [Turkey] Turkey’s Erdogan announces measures to address soaring housing prices – Reuters

- [Turkey] Turkey’s new measures fall short of addressing surging house prices, builders say – Reuters

- [United Kingdom] UK house prices rise but cost of living crisis will cool market, says Halifax. April marks longest run of monthly increases since 2016 as average cost of home reaches record of £286,079 – The Guardian

- [United Kingdom] Bank of England Sees U.K. House Price Growth Slowing Down – Bloomberg

- [United Kingdom] U.K. Housing Market Outlook Dims With Jump in Borrowing Costs. Fixed-rate mortgages provide a short-term cushion for buyers. End of the era of cheap money will stretch affordability – Bloomberg

- [United Kingdom] Cash buyers drive sales and prices in UK housing boom. Interest rate rises and cost of living squeeze likely to strengthen the role of mortgage-free buyers – FT

- [United Kingdom] ‘The risks are pretty big’: how long can UK house prices defy gravity? Pent-up lockdown demand and stamp duty holidays kept prices high, but rising mortgage rates and living costs may tip balance – The Guardian

- [United Kingdom] How Hongkongers became the biggest foreign homeowners in London and where they are buying – including boroughs along the Thames such as Barking and Dagenham, Tower Hamlets and Greenwich – South China Morning Post

- [United Kingdom] London’s housing market is making us buyers do irrational things. Lack of supply leads house-hunters to write heart-rending sob stories and offer outrageous amounts above the asking price – FT

On cross-country:

- Which housing markets are most exposed to the coming interest-rate storm? The pain of rising mortgage repayments will be harder to bear in some places than in others – The Economist

- Wages Can’t Keep Up With Spike in Housing Prices. Across the globe, the 10 cities that experienced the largest drops in affordability in 2021 were all in the U.S., new research shows – New York Times

- Grantham: “Day of reckoning” coming for global housing markets – Macro Business

- When were U.S.

Posted by at 5:00 AM

Labels: Global Housing Watch

Thursday, May 12, 2022

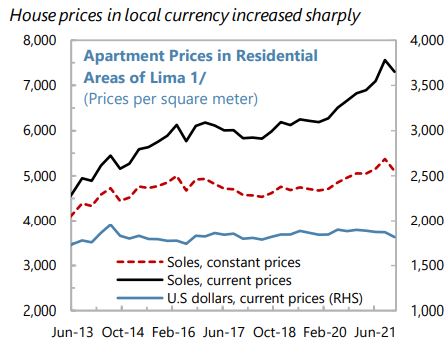

House Prices in Peru

Posted by at 10:38 AM

Labels: Global Housing Watch

Wednesday, May 11, 2022

Should We Insure Workers or Jobs During Recessions?

From a paper by Giulia Giupponi, Camille Landais, and Alice Lapeyre in the Journal of Economic Perspectives:

“What is the most efficient way to respond to recessions in the labor market? To this question, policymakers on the two sides of the pond gave diametrically opposed answers during the COVID-19 crisis. In the United States, the focus was on insuring workers by increasing the generosity of unemployment insurance. In Europe, instead, policies were concentrated on saving jobs, with the expansion of short-time work programs to subsidize labor hoarding. Who got it right? In this article, we show that far from being substitutes, unemployment insurance and short-time work exhibit strong complementarities. They provide insurance to different types of workers and against different types of shocks. Short-time work can be effective at reducing socially costly layoffs against large temporary shocks, but it is less effective against more persistent shocks that require reallocation across firms and sectors. We conclude that short-time work is an important addition to the labor market policy-toolkit during recessions, to be used alongside unemployment insurance.”

From a paper by Giulia Giupponi, Camille Landais, and Alice Lapeyre in the Journal of Economic Perspectives:

“What is the most efficient way to respond to recessions in the labor market? To this question, policymakers on the two sides of the pond gave diametrically opposed answers during the COVID-19 crisis. In the United States, the focus was on insuring workers by increasing the generosity of unemployment insurance. In Europe, instead, policies were concentrated on saving jobs,

Posted by at 11:35 AM

Labels: Macro Demystified

Subscribe to: Posts