Showing posts with label Macro Demystified. Show all posts

Saturday, January 22, 2022

Does Financial “Bonanza” Cause Premature Deindustrialization?

A recent working paper by A. Botta et al (2022) of the Levy Economics Institute analyzes factors that may have hindered productive development for over four decades prior to the COVID-19 pandemic.

Abstract: We investigate the role of (non-FDI) net capital inflows as a potential source of premature deindustrialization. We consider a sample of 36 developed and developing countries from 1980 to 2017, with major emphasis on the case of emerging and developing economies (EDE) in the context of increasing financial integration. We show that periods of abundant capital inflows may have caused the significant contraction of manufacturing share to employment and GDP, as well as the decrease of the economic complexity index. We also show that phenomena of “perverse” structural change are significantly more relevant in EDE countries than advanced ones. Based on such evidence, we conclude with some policy suggestions highlighting capital controls and external macroprudential measures taming international capital mobility as useful tools for promoting long-run productive development on top of strengthening (short-term) financial and macroeconomic stability.

A recent working paper by A. Botta et al (2022) of the Levy Economics Institute analyzes factors that may have hindered productive development for over four decades prior to the COVID-19 pandemic.

Abstract: We investigate the role of (non-FDI) net capital inflows as a potential source of premature deindustrialization. We consider a sample of 36 developed and developing countries from 1980 to 2017,

Posted by at 7:36 AM

Labels: Macro Demystified

Thursday, January 20, 2022

EconoFact at Five

From EconBrowser:

“[On] January 20th, EconoFact celebrates its 5 year anniversary, providing non-partisan, incisive analyses on timely and important economic and social policy issues. It does so by bringing to the public debate the expertise of leading economists and social scientists via memos and podcasts.

Topics:

With contributions from a network of economists and social scientists. (full disclosure: I’m one of the contributors.)

The entire topics list A-Z is here.”

From EconBrowser:

“[On] January 20th, EconoFact celebrates its 5 year anniversary, providing non-partisan, incisive analyses on timely and important economic and social policy issues. It does so by bringing to the public debate the expertise of leading economists and social scientists via memos and podcasts.

Topics:

With contributions from a network of economists and social scientists.

Posted by at 7:38 AM

Labels: Macro Demystified

Wednesday, January 19, 2022

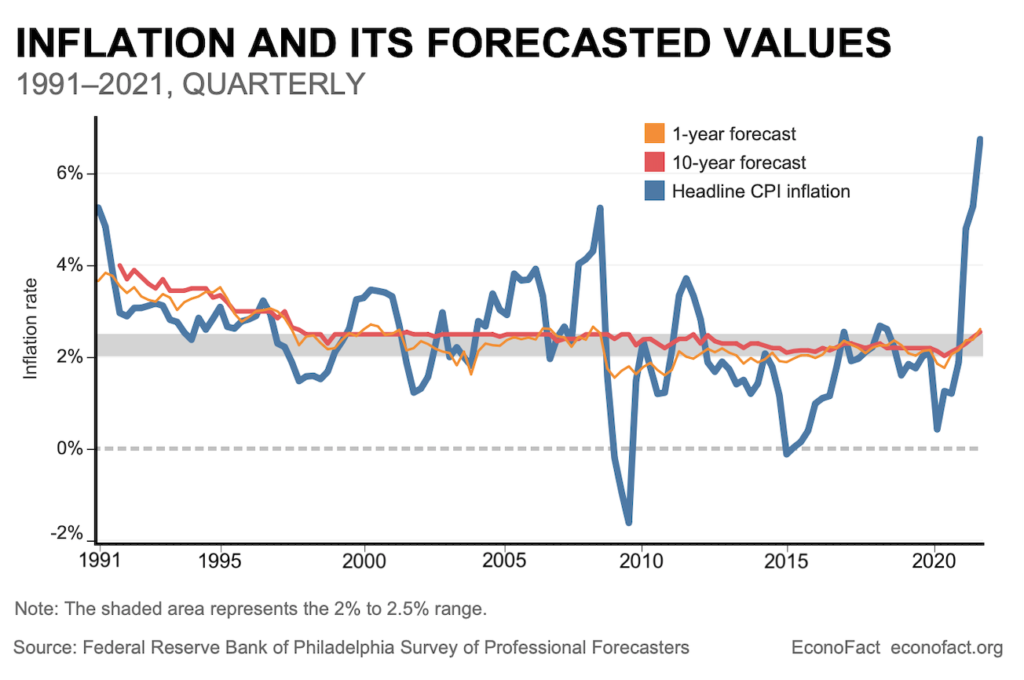

Thinking Can Make It So: The Important Role of Inflation Expectations

From ECONOFACT:

“The Issue:

Consumer prices rose 7 percent between December 2020 and December 2021, the third month in a row that this year-to-year inflation rate exceeded 6 percent. This December figure is the largest 12-month increase in 40 years. A central concern now is whether inflation will be transitory or, instead, we are entering a persistently high-inflation period, like what occurred in the 1970s. The proximate causes of current inflation include supply chain disruptions, labor shortages and pent-up consumer spending. But another important source of ongoing high inflation is an expectation of high inflation among households and businesses. How does the expectation of high inflation become self-fulfilling, and what proxies do we have to reflect this inherently unobservable but very important economic variable?

The Facts:

One source of inflation is when spending by people and companies strains the economy’s capacity for providing goods and services. Strains on the economy’s productive capacity can arise because of an increase in demand, constrictions to supply, or some combination of these two factors. Currently in the United States and other developed countries it is the combination of high demand and constrained supply that is feeding inflationary pressures. Demand in the United States was supported through the first year-and-a-half of the pandemic by government support programs. Cash payments to individuals and families under the CARES act of March 2020, the CARES Supplemental Appropriations Act of December 2020 and the American Rescue Plan of March 2021 contributed to sharp increases in personal disposable income. Spending may also have been boosted by low interest rates, which have increased the value of stocks, houses and other assets. Supply has been constrained because of a 2 percentage point drop in the share of the population participating in the labor force (either working or looking for a job).”

Continue reading here.

From ECONOFACT:

“The Issue:

Consumer prices rose 7 percent between December 2020 and December 2021, the third month in a row that this year-to-year inflation rate exceeded 6 percent. This December figure is the largest 12-month increase in 40 years. A central concern now is whether inflation will be transitory or, instead, we are entering a persistently high-inflation period, like what occurred in the 1970s.

Posted by at 6:24 PM

Labels: Macro Demystified

Monday, January 17, 2022

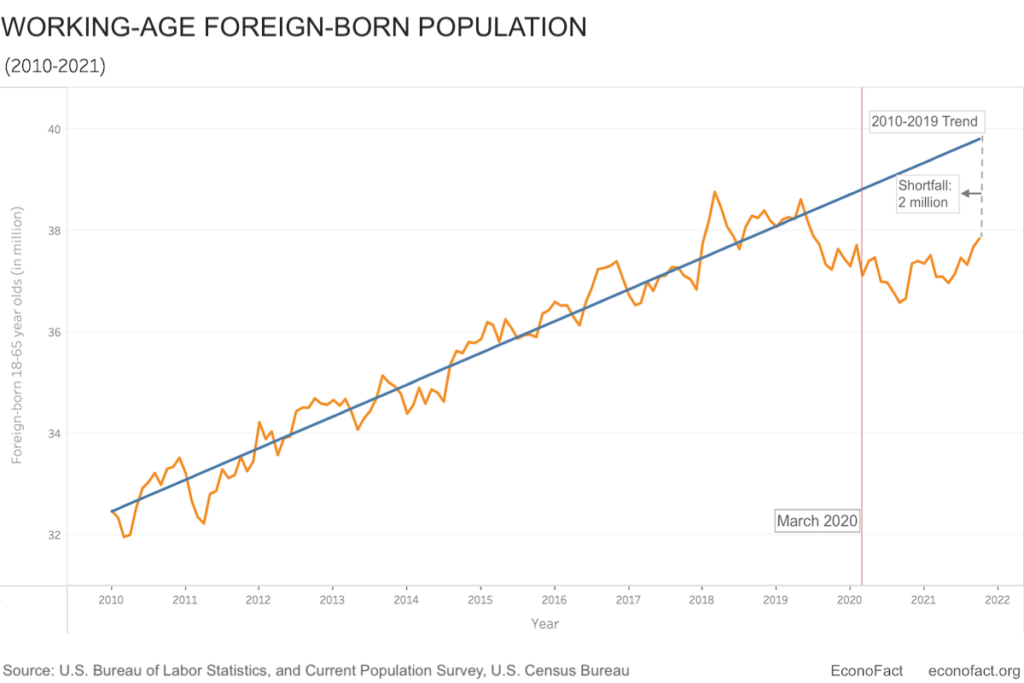

Labor Shortages and the Immigration Shortfall

The COVID-19 pandemic brought with it numerous travel and immigration-related restrictions throughout the globe. For the USA, this translated into a shortfall of nearly 2 million working-age immigrants compared to how many there would have been if the pre-2020 immigration trend had continued unchanged.

Metadata within this shows that out of these 2 million immigrants nearly one million would have been college graduates, implying a loss to the US labor market in terms of skilled workers, entrepreneurs, and a huge loss to American Universities which annually attract several foreign students. The drop in numbers of highly-skilled immigrants is significant due to its “long-run effects on productivity, innovation, and entrepreneurship”. The blog sheds light on these and several such issues.

Click here to read the full blog.

The COVID-19 pandemic brought with it numerous travel and immigration-related restrictions throughout the globe. For the USA, this translated into a shortfall of nearly 2 million working-age immigrants compared to how many there would have been if the pre-2020 immigration trend had continued unchanged.

Source: Labor Shortages and the Immigration Shortfall (2022). Econofact.org

Metadata within this shows that out of these 2 million immigrants nearly one million would have been college graduates,

Posted by at 10:33 AM

Labels: Inclusive Growth, Macro Demystified

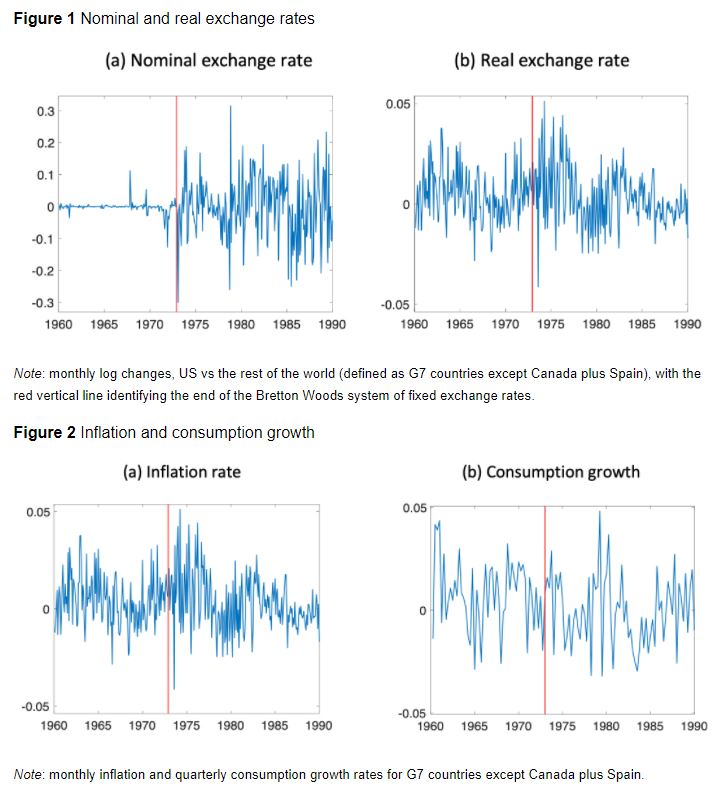

The Mussa puzzle and the optimal exchange rate policy

From a VoxEU post by Oleg Itskhoki and Dmitry Mukhin:

“The Mussa puzzle refers to the existence of a large and sudden jump in the volatility of the real exchange rate after the adoption of a floating exchange rate regime in 1973. It is a central piece of evidence in favour of monetary non-neutrality. In contrast to conventional wisdom, this column argues that the puzzle cannot be explained with sticky prices, and instead provides strong evidence in favour of monetary transmission via the financial market. This has important consequences for the design of optimal monetary and exchange rate policy.

What is the most convincing evidence that monetary shocks affect real outcomes? When Nakamura and Steinsson (2018) surveyed prominent macroeconomists, “the three most common answers were: the evidence presented in Friedman and Schwartz (1963) regarding the role of monetary policy in the severity of the Great Depression; the Volcker disinflation of the early 1980s and accompanying twin recession; and the sharp break in the volatility of the US real exchange rate accompanying the breakdown of the Bretton Woods System of fixed exchange rates in 1973”. This third fact, famously documented by Mussa (1986), is especially appealing as it relies on a simple and clear identification of the causal real effect from a shift in monetary policy: a large and discontinuous change in the nominal exchange rate process makes it hard to attribute the increased volatility of the real exchange rate to any other factors (see Figure 1)

What is missing from this narrative, however, is that there was no simultaneous change in the properties of other macro variables – neither nominal like inflation, nor real like consumption and output (Baxter and Stockman 1989, Flood and Rose 1995, and Figure 2). One could interpret this as an extreme form of neutrality, where a major shift in the monetary regime, which increases the volatility of the nominal exchange rate by an order of magnitude, does not affect the equilibrium properties of any macro variables, apart from the real exchange rate. In fact, this is a considerably more puzzling part of the larger set of ‘Mussa facts’ summarised in Figures 1 and 2. In a recent paper, we argue that this evidence points to a particular unconventional transmission mechanism of monetary policy and has important normative implications for both open and closed economies (Itskhoki and Mukhin 2021b).”

Continue reading here.

From a VoxEU post by Oleg Itskhoki and Dmitry Mukhin:

“The Mussa puzzle refers to the existence of a large and sudden jump in the volatility of the real exchange rate after the adoption of a floating exchange rate regime in 1973. It is a central piece of evidence in favour of monetary non-neutrality. In contrast to conventional wisdom, this column argues that the puzzle cannot be explained with sticky prices,

Posted by at 9:51 AM

Labels: Macro Demystified

Subscribe to: Posts